However, latest results from our surveys indicate that ever more households want to bank digitally. So, given the compelling data from our surveys, what has happened to the number of branches in Australia in recent years? As branches are expensive, have outlets been closed in response to the digital migration?

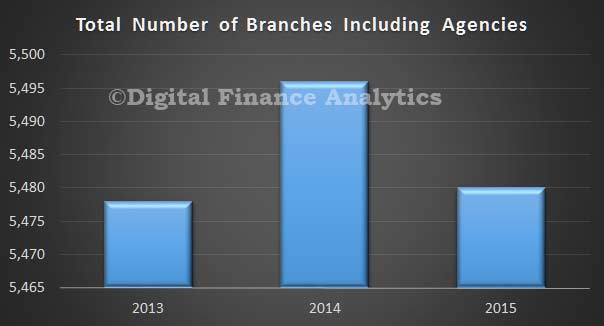

Analysis from the APRA Point of Presence databases shows that the total number of branch outlets has grown slightly between 2013 and 2015. There were 5,478 outlets in 2013, 5,496 in 2014 and 5,480 in 2015. Overall almost no change.

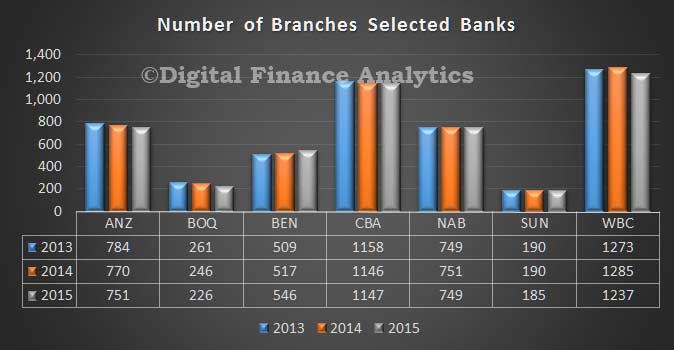

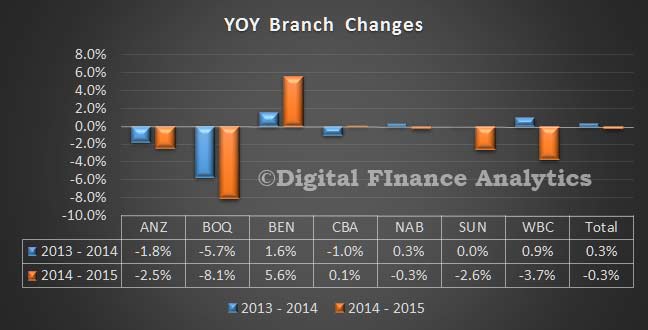

Analysis of the count of branches by selected banks, which includes agency outlets, shows that most have reduced their footprints slightly, other than Bendigo/Adelaide Bank, who grew their footprint by 5.6% in 204-15.

On the other hand, Bank of Queensland has reduced the number of franchise branches and recorded a drop of 8.1% in 2014-15.

We conclude that so far banks are not responding to the digital revolution by closing branches, although some have reconfigured existing ones into smaller and more efficient units.

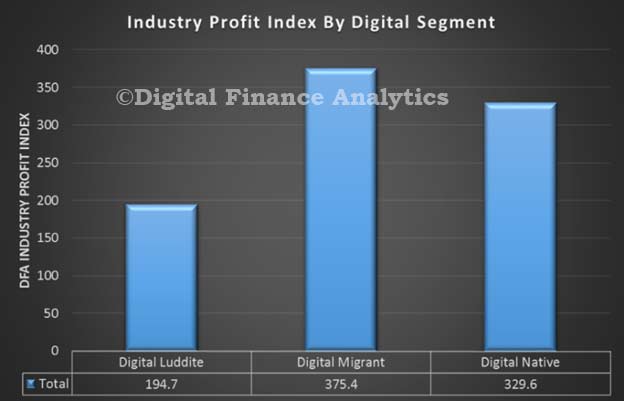

We segment households into three groups. Digital Luddites are the last bastions of traditional banking and centre on branch and ATM access, value face to face conversations, and the bank brand. They are migrating from PC’s to smart devices to access online bank services (if they use them).

In contrast, Digital Natives expect 24×7 access, mobile banking, near-field payments and online applications. They expect their bank to be in the social media environment, and would value video-conferencing with the bank advisor. Branch access, bank brand and face to face conversations are not important to this group.

Digital migrants are somewhere in between, however, more are demanding more from online services.

We think that existing players need to be thinking about how they will deploy appropriate services through digital channels, as their customers are rapidly migrating there.

We see this migration to digital is more advanced among higher income households. So players which are slow to catch the wave will be left with potentially less valuable customers longer term.

Here is a glimpse of our latest profitability index which shows how much less valuable Digital Luddites are compared with digitally aligned households. There is a real risk of stranded costs in the branch network.

Players need to adapt more quickly to the digital world. We are past an omni-channel (let them choose a channel) strategy. Digital migration needs to become central strategy because the winners will be those with the technical capability, customer sense and flexibility to reinvent banking in the digital age.

The bank branch has limited life expectancy. Banks should be planning accordingly.

The Australian banking industry is a classic economic ‘oligopoly’ with the so-called ‘Four Pillars’ or ‘Big Four’ (National Australia Bank (NAB), Commonwealth Bank of Australia (CBA), ANZ and Westpac) dominating not only the banking sector but the whole financial sector and arguably the economy.

The big four banks account for over 25% of the market capitalisation of the ASX 200, and are valued at over $360 billion. In total, the four banks reported assets in 2015 of some $3.5 trillion or about 10 times the size of BHP and RIO combined, and profits for their latest financial year of over $30 billion between them.

In an oligopoly, the dominant players operate a very similar business model. This is true of the Big Four, which operate within a structure known as ‘universal banking’. Not only do each of these behemoths run a traditional retail and business bank, they also have wealth management (mainly retail superannuation fund management) and insurance subsidiaries. To complete the picture, each of the four runs a wholly owned bank in New Zealand, again dominating the banking system in that country. The banks operate throughout Australasia, often with competing branches (and valuable jobs) in each small town – Australia is ‘over banked’.

The risks of having one of the most concentrated banking systems in the world were outlined in 2012 by the International Monetary Fund (IMF), it warned that Australia’s banks had:

“broadly similar business models and reliance on offshore funding leave them exposed to common shocks and disruptions to funding markets. Against a still worrying global environment, these risks will need to be closely monitored, particularly if the domestic economy slows sharply.”

Among the four banks, there is constant jockeying for prominence and any one time one bank climbs to the top of the pile. At the moment, the clear winner is CBA, largest by capitalisation, latest annual profits and staff employed with the lowest Cost to Income Ratio (CIR). Another winner is Westpac, the smallest by assets and employees but with an enviable CIR and Net Interest Margin (NIM) leading to excellent profit results. Meanwhile, NAB trails the others by profitability and with a low NIM and high CIR, will be likely do so for some time. Nonetheless, NAB is by any standards a very profitable company, if a bit overshadowed by the other banks this year.

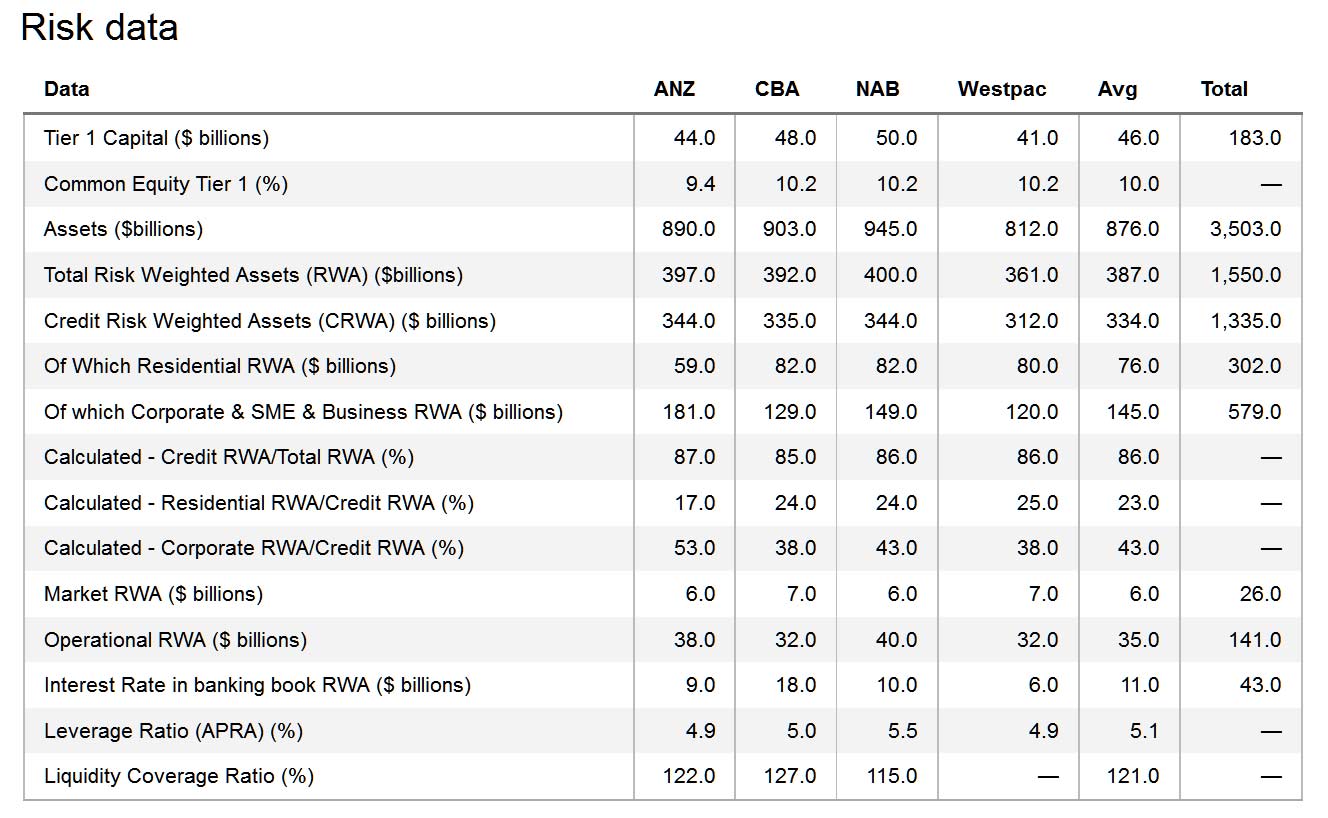

It should be noted that not all banks report their financial results at the same time in a completely consistent fashion. However each quarter the banks are required to report their risk numbers to the Australian Prudential Regulation Authority (APRA), the banking regulator. These so-called APS 330 reports give a picture (albeit slightly murky) of where banks are taking risks and the size of those risks.

These numbers show that the banks hold roughly similar amounts of assets, so-called Risk Weighted Assets (RWA) and associated capital. Although Westpac, being slightly smaller, has about 10% less of each. This data shows Big Four banks are still predominantly lending institutions with about 86% of their Risk Weighted Assets (RWAs) related to credit.

While ANZ has a higher proportion of corporate and business lending than the others, about 23% of its credit (RWAs) relates to retail, mainly residential mortgage, lending. With a few notable exceptions, such as CBAs exposure to interest rate risks and NAB’s operational risks, the risk numbers are similar across the banks.

From an analysis of prior APS 330 reports (not shown), it appears that, although the RWAs for residential mortgages have increased slightly for all banks (mainly because lending has increased), the banking sector has not factored in much additional capital to cover the potential for the busting of a housing bubble.

The large Australian banks will in the next year face headwinds from a number of directions. First, any busting or even deflation of Australia’s real or imagined housing bubble will undoubtedly give the banks serious headaches.

Likewise, the end of the mining boom is already beginning to take its toll on mining companies, even the largest. If the gloom spreads, loans to the sector might be under pressure. Last, but far from least, banking scandals will definitely come to the fore this year especially market manipulation and product misselling.

Disruption from technology

Following the retreats of both NAB and ANZ from their respective overseas forays, it looks like the four banks are going to resemble each other even more as they are all embarking on strategies that target the same Australasian retail, mortgage and business markets. But there is at least one significant point of difference between the banks that might give a clue to potential shifts in future.

In banking, as in other industries, technology is critical. After an outsourcing deal that went sour, in 2008 the CBA board was forced (some say was brave enough) to embark on a complete refresh of its ageing IT systems, often called a Core Systems Replacement (CSR).

After some significant project blowouts, CBA eventually got the CSR to work and their annual profit numbers are beginning to reflect that success. Meanwhile, NAB is in the middle of its almost decade long CSR project (called Nextgen) and is constantly changing its management, which does not bode well for its completion in the near future. On the other hand, the new Chief Information Officer (CIO) of Westpac has denied that the firm needs a CSR, and has embarked on a much needed face-lift to the bank’s ageing systems.

After a number of attempts to change its core systems, the new management of ANZ have just announced that they are hiring an ex-Google executive to become its head of ‘digital banking’ – but to do what is still not certain.

Given the oft repeated fact that some 70% of IT projects fail, it looks like one or more of the banks are in for some big headaches over the next decade.

For this snapshot, the information is collected from the latest annual reports (2014-2015), except for CBA which reported its semi-annual numbers in February 2016. The risk figures are taken from the 2016 December quarter APS 330 reports of the banks to APRA, which are available at the banks’ websites.

Author: Pat McConnell, Honorary Fellow, Macquarie University Applied Finance Centre, Macquarie University

The Basel Committee on Banking Supervision’s second set of proposals to update the standardised approach to credit risk, published in December 2015, represents a change of approach that will improve risk sensitivity. But the regime proposes to retain flexibility for national regulatory implementation and bank risk weighting. This means that comparing capital ratios across banks and countries will continue to be elusive, says Fitch Ratings.

If the proposals are implemented, there will be two separate risk weighting approaches. One will use external credit ratings and the other will rely on standardised assessments. Capital adequacy ratios will vary, depending on which methodology is used, and this will make it difficult to preserve consistency and simplify comparison of output ratios.

The use of credit ratings for assessing bank and corporate credit exposures, scrapped under Basel’s original proposals, has been reinstated. We think this is an improvement because credit ratings serve as important credit risk benchmarks and have been effective in assessing relative credit risk. They can also be effective in fostering consistency. The external credit rating based approach (ECRA) maps credit ratings to a number of risk weight buckets and is currently used by the majority of the Basel Committee’s 27 national members.

Some countries however, notably the US, prohibit the use of credit ratings for regulatory purposes. Basel proposes that banks in these countries use a new standardised credit risk assessment (SCRA) approach. Under the SCRA, bank and corporate exposures will be split into categories and risk weighted according to the specific characteristics of the counterparty.

Risk weights calculated for bank exposures using either the ECRA or SCRA could vary because banks have to undertake mandatory due diligence when using credit ratings. This could lead to a bank assigning a risk weighting at least one bucket higher (but not lower) than the “base” risk weight. The SCRA proposal also imposes a higher risk weight floor for bank exposures and applies larger haircuts to highly rated non-sovereign bonds than the ECRA. If implemented, this means US banks will see risk weights more than double on exposures to their US peers and will need to post or receive higher collateral on repurchase transactions over corporate securities, for example.

Basel is also proposing an overhaul of capital allocation to real estate lending, with more granular risk weights. Capital requirements for property development loans, buy-to-let (BTL) mortgages and more speculative real estate finance will be hiked to reflect greater risk. All mortgages will be capitalised at original loan to values (LTV) to inhibit cyclical changes to risk weights. But during times of rising property prices, lenders might encourage borrowers to refinance their loans, to reduce their own capital requirements. If the proposals are adopted, we think some banks, notably those heavily involved in high LTV BTL lending, will have adjust their business models.

The proposals discourage banks from lending in foreign currency and holding equity investments by increasing risk weightings. By requiring banks to recognise capital charges on unconditionally cancellable commitments, such as credit card and personal overdraft facilities, the most affected banks may reduce credit card limits or pass higher costs of capital to consumers.

At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

(1) The interest rate on the main refinancing operations of the Eurosystem will be decreased by 5 basis points to 0.00%, starting from the operation to be settled on 16 March 2016.

(2) The interest rate on the marginal lending facility will be decreased by 5 basis points to 0.25%, with effect from 16 March 2016.

(3) The interest rate on the deposit facility will be decreased by 10 basis points to -0.40%, with effect from 16 March 2016.

(4) The monthly purchases under the asset purchase programme will be expanded to €80 billion starting in April.

(5) Investment grade euro-denominated bonds issued by non-bank corporations established in the euro area will be included in the list of assets that are eligible for regular purchases.

(6) A new series of four targeted longer-term refinancing operations (TLTRO II), each with a maturity of four years, will be launched, starting in June 2016. Borrowing conditions in these operations can be as low as the interest rate on the deposit facility.

The outlook for global growth has deteriorated since the December Monetary Policy Statement, due to weaker growth in China and other emerging markets, and slower growth in Europe. This is despite extraordinary monetary accommodation, and further declines in interest rates in several countries. Financial market volatility has increased, reflected in higher credit spreads. Commodity prices remain low.

Domestically, the dairy sector faces difficult challenges, but domestic growth is expected to be supported by strong inward migration, tourism, a pipeline of construction activity and accommodative monetary policy.

The trade-weighted exchange rate is more than 4 percent higher than projected in December, and a decline would be appropriate given the weakness in export prices.

House price inflation in Auckland has moderated in recent months, but house prices remain at high levels and additional housing supply is needed. Housing market pressures have been building in some other regions.

There are many risks to the outlook. Internationally, these are to the downside and relate to the prospects for global growth, particularly around China, and the outlook for global financial markets. The main domestic risks relate to weakness in the dairy sector, the decline in inflation expectations, the possibility of continued high net immigration, and pressures in the housing market.

Headline inflation remains low, mostly due to continued falls in prices for fuel and other imports. Annual core inflation, which excludes the effects of transitory price movements, is higher, at 1.6 percent.

While long-run inflation expectations are well-anchored at 2 percent, there has been a material decline in a range of inflation expectations measures. This is a concern because it increases the risk that the decline in expectations becomes self-fulfilling and subdues future inflation outcomes.

Headline inflation is expected to move higher over 2016, but take longer to reach the target range. Monetary policy will continue to be accommodative. Further policy easing may be required to ensure that future average inflation settles near the middle of the target range. We will continue to watch closely the emerging flow of economic data

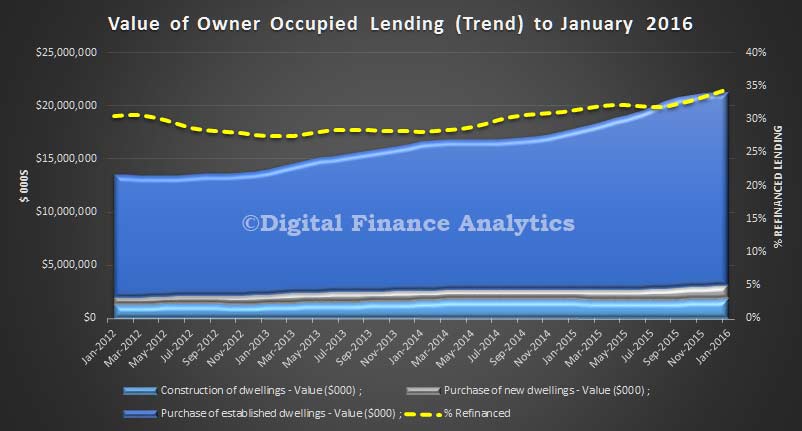

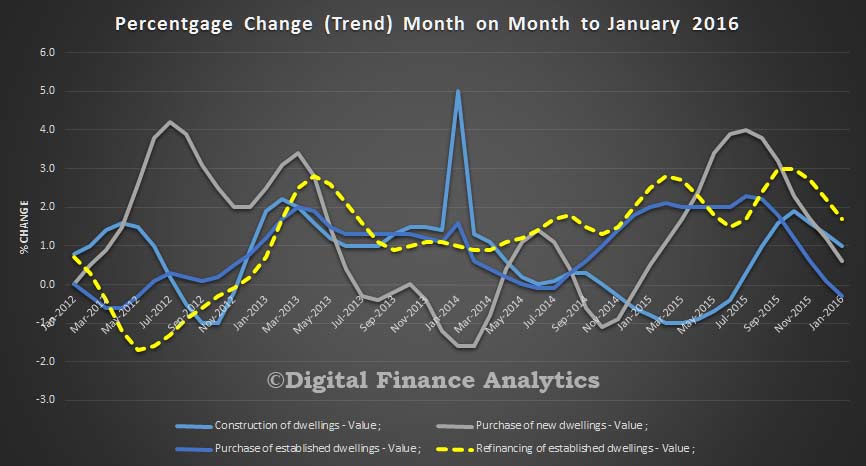

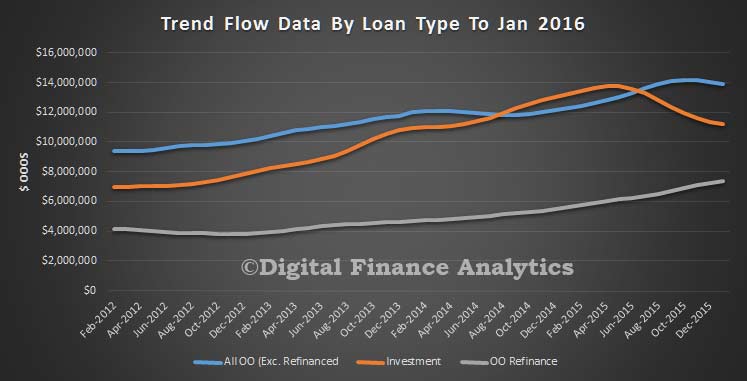

The latest data from the ABS on housing finance to January 2016 shows that the total value of dwelling commitments excluding alterations and additions (trend) fell 0.6% in January 2016 compared with December 2015. $32.4 bn of loans were written, with loans for owner occupation worth $21.2bn (down 0.1%) and investment loans $11.2bn down 1.6%. The number of refinancing commitments for owner occupied housing (trend) rose 1.7% in January 2016, following a rise of 2.0% in December 2015. Banks are fighting for refinance market share. We think that tighter lending standards are biting, this is reflected in a rise in the number of households who are having problems getting the loan they want. One in ten are having difficulties.

The total value of owner occupied housing commitments (trend) fell (down $19m, 0.1%) in January 2016. A fall was recorded in commitments for the purchase of established dwellings (down $46m, 0.3%) while rises were recorded in commitments for the construction of dwellings (up $19m, 1.0%) and commitments for the purchase of new dwellings (up $8m, 0.6%).

The number of owner occupied housing commitments (trend) rose 0.4% in January 2016, following a rise of 0.6% in December 2015. Rises were recorded in commitments for the refinancing of established dwellings (up $346m, 1.7%), commitments for the purchase of new dwellings (up $37m, 1.2%) and commitments for the construction of dwellings (up $31m, 0.5%), while a fall was recorded in commitments for the purchase of established dwellings excluding refinancing (down $188m, 0.7%).

The total value of investment housing commitments (trend) fell (down $186m, 1.6%) in January 2016 compared with December 2015. Falls were recorded in commitments for the purchase of dwellings by others for rent or resale (down $23m, 1.9%) and commitments for the purchase of dwellings by individuals for rent or resale (down $178m, 1.9%), while a rise was recorded in commitments for the construction of dwellings for rent or resale (up $15m, 1.7%).

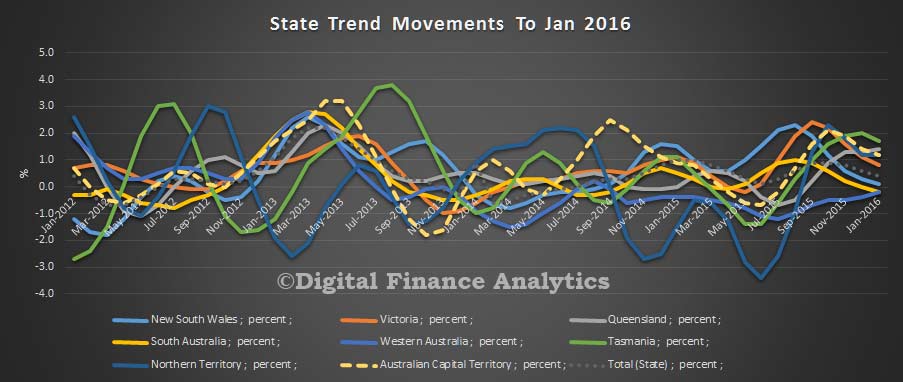

Between December 2015 and January 2016, the number of owner occupied housing commitments (trend) rose in Queensland (up $146m, 1.4%), Victoria (up $128m, 0.8%), New South Wales (up $23m, 0.1%), Tasmania (up $15m, 1.7%), the Australian Capital Territory (up $13m, 1.2%) and the Northern Territory (up $4m, 1.2%), while falls were recorded in South Australia (down $6m, 0.2%) and Western Australia (down $15m, 0.2%).

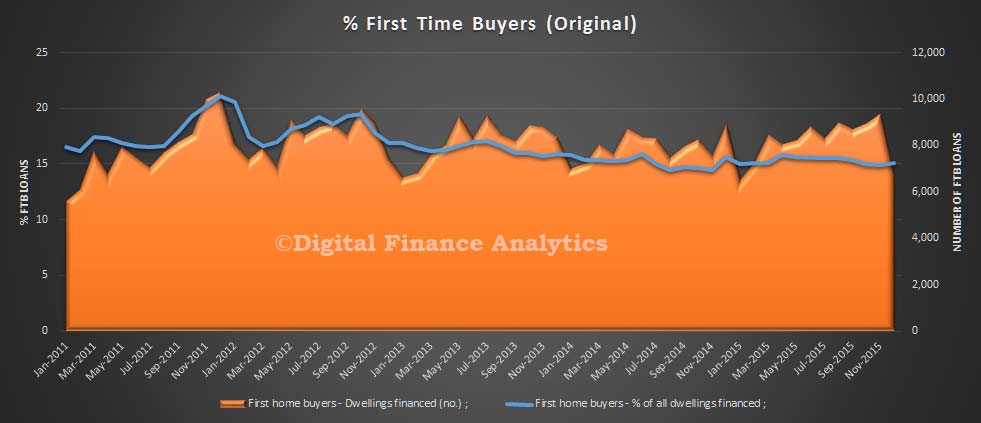

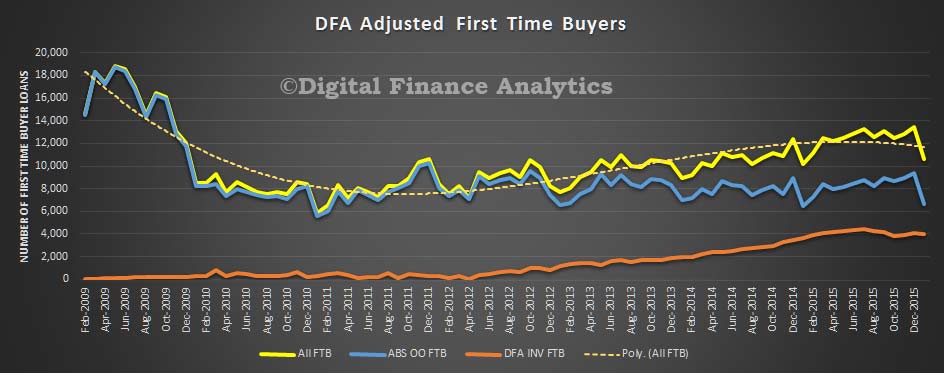

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments remain unchanged at 15.1% in January 2016 from December 2015. However, the number of loans fell from 9,357 to 6,669 in the month. Between December 2015 and January 2016, the average loan size for first home buyers fell $-9,300 to $338,800. The average loan size for all owner occupied housing commitments fell $-5,400 to $372,400 for the same period.

The number of first time buyers going direct to the investment market fell 3%, but remains elevated compared with previous years. These transactions are based on our survey data and are not counted in the ABS FTB OO data.

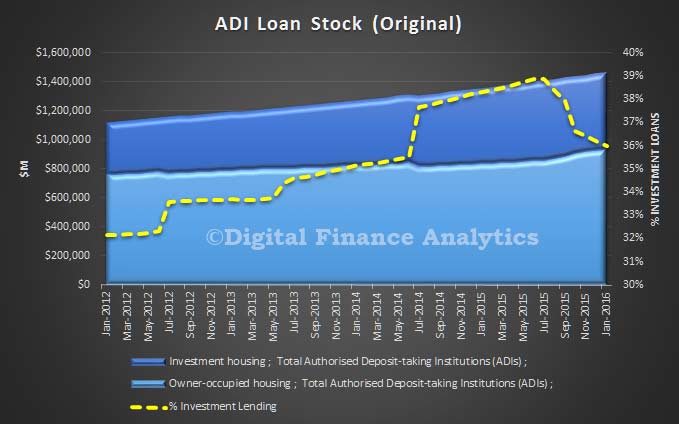

At the end of January 2016, the value of outstanding housing loans financed by Authorised Deposit-taking Institutions (ADIs) was $1,466b, up $8b (0.5%) from the December 2015 closing balance. Owner occupied housing loan outstandings financed by ADIs rose $8b (0.8%) to $939b and investment housing loan outstandings financed by ADIs was flat at $528b. Overall 36% of loans are for investment housing purposes.

In a speech delivered at Nottingham University, Martin Weale discussed a range of unconventional policy options available to central banks. He underlined that he not believe the UK’s Monetary Policy Committee (MPC) will need to expand its use of unconventional policy any time soon, but it was important to assess these options as “the Committee does not want to be a monetary equivalent of King Æthelred the Unready”.

Martin analysed the historical experience of the four main unconventional strategies that had been deployed by central banks: quantitative easing; forward guidance; monetary finance; and negative interest rates.

On quantitative easing, Martin outlined his own analysis of its impact in the UK and US. While noting arguments that QE would be less effective now than it had been in the past, Martin said his own analysis contradicted that suggestion – a finding which was part of the reason why he had been more inclined to vote for interest rate rises than his colleagues in recent years: “There is less reason to delay policy tightening if you are confident that you have a means of providing material further support should it be needed”.

In addition, Martin pointed out that the MPC could, in future, expand the range of assets it purchases under QE, noting that in the early 1980s it held substantial amounts of non-government securities. He said: “While there were, at that time, very good reasons why the Bank of England did not want to make substantial purchases of private-sector assets, it is not clear to me how far those are necessarily an insuperable obstacle.”

Turning to forward guidance, Martin found that state-contingent forward guidance tended to have a “relatively modest effect on output and inflation.” Martin noted that this finding depends on where the relevant threshold was set and, in any case, the MPC has only considered such thresholds as reference points rather than rules. Without a rule-based system, he argued, it is hard to be clear about the circumstances in which this sort of state-based guidance will be used, and thus its impact cannot be easily evaluated. He said: “The Monetary Policy Committee does not follow a rule for interest rates and it therefore cannot amend such a rule. It can, of course, do what it did in August 2013, but it is not clear how such a policy can be transformed into a general part of the policy armoury in a way which makes it possible to assess its effects”.

Moving beyond policies the Bank of England has pursued in recent years, Martin stated that – assuming that central bank reserves would continue to be remunerated – he struggled to see a clear difference between some versions of monetary finance and QE. The difference between the two, conceptually, has generally been that the former is seen as permanent and the latter as temporary. However, Martin noted it is not possible for a government to force its successors to maintain a ‘helicopter drop’ as a permanent feature of the landscape. He said: “That is not to say that asset purchases are monetary financing…but rather that an attempt at monetary financing may blur into something not very different from asset purchases, in that both shorten the maturity of public sector debt.” He observed that if some form of reserve requirement were imposed, with reserves unremunerated, the effect was not very different from a tax on banks which would eventually lead to lower spending.

Addressing recent global discussions about negative interest rates, Martin believes they “probably do provide some support, but the extent of this depends on how banks behave, and whether they are able to pass on the full amount of the rate reduction to borrowers”. However, while some challenges – such as banks moving reserves from central banks into cash – could potentially be overcome, Martin underlined that “there is a risk of adverse side-effect and it would be wrong to introduce negative interest rates without being confident that these side-effects were going to be small.” He added: “Equally, measures designed to protect the domestic economy from the effects of negative interest rates mean that the policy becomes close to one of beggar-my-neighbour exchange rate management”.

Martin concluded by arguing that “it is appreciably more likely that monetary tightening rather than monetary easing will be needed in the United Kingdom over the next two years”, noting that financial markets and commodity prices have recovered over the last month, while disappointing recent productivity indicated that unit labour wage costs were stronger than is apparent in headline wage figures. “Nevertheless”, he concluded, “should the need for further easing arise because of a sharp weakening in the outlook for inflation, the scope for further asset purchases is substantial, while the obstacles we saw to reducing Bank Rate below 1/2 per cent are no longer material. These observations should allay concerns that it will be difficult to bring inflation back to target”.

Alex begins by observing that investors’ questions about returns have not translated, as they have done before, into questions about resilience. When UK bank price-to-book ratios were this low in 2009, senior unsecured debt spreads were over 350bps – compared to 73bps today. Underlying that is the transformation of bank capital. In the 2015 stress test, banks absorbed losses of £37bn – over twice the losses of the system in the crisis – even while continuing to grow credit to the real economy.

In December, the Bank of England gave a clear statement about the appropriate baseline level of capital for the systemic part of the UK banking system. Across major UK banks, no less than 3.75% of total assets should be funded with tier 1 capital. On current measures of risk, we expect these banks to fund no less than 13½% of risk weighted assets with tier 1 capital.

Alex says that “after a long march to build capital strength, UK banks are within a hair’s breadth of that [expectation] today. And the rewards of greater resilience are being reaped”.

It was obvious in the aftermath of the crisis where bank capital needed to go. Up. A lot. And with market confidence so low at the time, more capital not only boosted resilience, it also was needed for lending to resume. Alex emphasises that “capital was good for resilience and good for growth”.

However, after a point, another unit of capital buys a much smaller fall in the probability of bank failure. And the evidence that higher capital requirements can push up bank funding costs – costs which will be borne by real borrowers and real savers – cannot be ignored.

How to best protect the real economy without holding it back? The UK answer has three parts.

First, to protect the economy from the consequences of bank failure. And to do so at minimal economic cost. Effective bank resolution unlocks this, opening the door to preserving the functions of failed banks without recourse to the taxpayer. The G20 agreement on Total Loss Absorbing Capacity (TLAC) standards is “a game changer because it hardwires the recapitalisation of failing banks”. Rapid recapitalisation of failed banks speeds economic recovery. International estimates suggest that the removal of the ‘too big to fail’ subsidy cuts the risk of failure by a third. Alex says that “it is essential that efforts to ensure even the largest banks can be resolved remain on track”.

But even with an effective resolution backstop in place, the costs of systemic bank failure are far from insignificant.

So the second part is a baseline capital standard that makes the economic disruption caused by a weak banking system extremely rare. But not more so. In the UK, even the two biggest failures of the crisis suffered losses comfortably within the baseline described above. Going further could have a sharply diminishing further effect on the probability of banking failure and could run the risk of economic cost. The biggest banks will be subject to a baseline capital buffer of nearly 5% of risk weighted assets, sitting on top of an 8.5% hard floor for tier 1 capital. This “gives room for systemic banks to absorb losses without being forced to close their doors and cease their service to the economy. It achieves not just greater bank resilience, but greater resilience of service to the macro economy”.

But it would be a mistake to think that a 5% capital buffer is always and everywhere the right one.

So the third part is flexibility. Flexibility to raise capital buffers if the threat of future losses grows, and cut them again if those threats materialise of recede. This avoids what might otherwise be a need to capitalise the system for the very riskiest times, all the time. Alex explains that the Bank is “seeking to match the size of those [capital] buffers – the strength of defence – to the threat of future losses as they change over time”. With the stress scenario varying systematically with our assessment of the risks, the stress test will guide as to how – given banks’ exposures – the Bank’s judgement about the risks should be reflected in capital buffers. The Bank will have a bias to acting early and gradually. It expects to be adding around 1% to the countercyclical capital buffer on UK exposures of all banks, even before the overall threat of future losses looks high. These capital buffers will go as far as needed to ensure banks’ defences keep up with threats if they grow. And if threats materialise, or shrink, the Bank will reduce its expectation for capital buffers back towards the baseline level.

Flexibility extends beyond moving capital buffers up and down. We are learning about the effects of higher capital and leverage requirements. Developments such as the signs of reduced liquidity in sovereign repo markets are prompting us to assess whether targeted amendments to the design of regulations could benefit the real economy, without exposing it to more risk. Alex says that “the design of new requirements was macroprudential. So must be their implementation”.

Alex concludes that “with resolution regimes well advanced and game-changing bail-in principles established, the upward march to higher capital levels can soon reach the new baseline. A baseline that, on what we know today, protects the real economy without unnecessary risk of holding it back. And with the flexibility to adapt and continually align resilience with threats, we have a compelling answer to the question of how to marry prudence with macroeconomic sense. So that you can protect and serve the real economy in good times and bad”.

FED Vice Chairman Stanley Fischer spoke at the “Policy Challenges in an Interconnected World” Conference. In his speech, “Reflections on Macroeconomics Then and Now“, he highlighted some of the macroeconomic uncertainties which beset the economy.

I would like briefly to take up several topics in more detail. Some of them are issues that have remained central to the macroeconomic agenda over the past 50 years, some have to my regret fallen off the agenda, and others are new to the agenda.

Inflation and unemployment: Estimated Phillips curves appear to be flatter than they were estimated to be many years ago–in terms of the textbooks, Phillips curves appear to be closer to what used to be called the Keynesian case (flat Phillips curve) than to the classical case (vertical Phillips curve). Since the U.S. economy is now below our 2 percent inflation target, and since unemployment is in the vicinity of full employment, it is sometimes argued that the link between unemployment and inflation must have been broken. I don’t believe that. Rather the link has never been very strong, but it exists, and we may well at present be seeing the first stirrings of an increase in the inflation rate–something that we would like to happen.

Productivity and growth: The rate of productivity growth in the United States and in much of the world has fallen dramatically in the past 20 years. The table shows calculated rates of annual productivity growth for the United States over three periods: 1952 to 1973; 1974 to 2007; and the most recent period, 2008 to 2015. After having been 3 percent and 2.1 percent in the first two periods, the annual rate of productivity growth has fallen to 1.2 percent in the period since the start of the global financial crisis.The right guide to thinking in this case is given by a famous Herbert Stein line: “The difference between a growth rate of 1 percent and 2 percent is 100 percent.” Why? Productivity growth is a major determinant of long-term growth. At a 1 percent growth rate, it takes income 70 years to double. At a 2 percent growth rate, it takes 35 years to double. That is to say, that with a growth rate of 1 percent per capita, it takes two generations for per capita income to double; at a 2 percent per capita growth rate, it takes one generation for per capita income to double. That is a massive difference, one that would very likely have severe consequences for the national mood, and possibly for economic policy. That is to say, there are few issues more important for the future of our economy, and those of every other country, than the rate of productivity growth.At this stage, we simply do not know what will happen to productivity growth.Robert Gordon of Northwestern University has just published an extremely interesting and pessimistic book that argues we will have to accept the fact that productivity will not grow in future at anything like the rates of the period before 1973. Others look around and see impressive changes in technology and cannot believe that productivity growth will not move back closer to the higher levels of yesteryear.7 A great deal of work is taking place to evaluate the data, but so far there is little evidence that data difficulties account for a significant part of the decline in productivity growth as calculated by the Bureau of Labor Statistics.

The ZLB and the effectiveness of monetary policy: From December 2008 to December 2015, the federal funds rate target set by the Fed was a range of 0 to 1/4 percent, a range of rates that was described as the ZLB (zero lower bound).9 Between December 2008 and December 2014, the Fed engaged in QE–quantitative easing–through a variety of programs. Empirical work done at the Fed and elsewhere suggests that QE worked in the sense that it reduced interest rates other than the federal funds rate, and particularly seems to have succeeded in driving down longer-term rates, which are the rates most relevant to spending decisions.Critics have argued that QE has gradually become less effective over the years, and should no longer be used.It is extremely difficult to appraise the effectiveness of a program all of whose parameters have been announced at the beginning of the program. But I regard it as significant with respect to the effectiveness of QE that the taper tantrum in 2013, apparently caused by a belief that the Fed was going to wind down its purchases sooner than expected, had a major effect on interest rates.More recently, critics have argued that QE, together with negative interest rates, is no longer effective in either Japan or in the euro zone.That case has not yet been empirically established, and I believe that central banks still have the capacity through QE and other measures to run expansionary monetary policies, even at the zero lower bound.

The monetary-fiscal policy mix: There was once a great deal of work on the optimal monetary-fiscal policy mix. The topic was interesting and the analysis persuasive. Nonetheless the subject seems to be disappearing from the public dialogue; perhaps in ascendance is the notion that–except in extremis, as in 2009–activist fiscal policy should not be used at all. Certainly, it is easier for a central bank to change its policies than for a Treasury or Finance Ministry to do so, but it remains a pity that the fiscal lever seems to have been disabled.

The financial sector: Carmen Reinhart and Ken Rogoff’s book, This Time Is Different, must have been written largely before the start of the great financial crisis. I find their evidence that a recession accompanied by a financial crisis is likely to be much more serious than an ordinary recession persuasive, but the point remains contentious. Even in the case of the Great Recession, it is possible that the U.S. recession got a second wind when the euro-zone crisis worsened in 2011. But no one should forget the immensity of the financial crisis that the U.S. economy and the world went through following the bankruptcy of Lehman Brothers–and no one should forget that such things could happen again.The subsequent tightening of the financial regulatory system under the Dodd-Frank Act was essential, and the complaints about excessive regulation and excessive demands for banks to hold capital betray at best a very short memory.We, the official sector and particularly the regulatory authorities, do have an obligation to try to minimize the regulatory and other burdens placed on the private sector by the official sector–but we have a no less important obligation to try to prevent another financial crisis. And we should also remember that the shadow banking system played an important role in the propagation of the financial crisis, and endeavor to reduce the riskiness of that system.

The economy and the price of oil: For some time, at least since the United States became an oil importer, it has been believed that a low price of oil is good for the economy. So when the price of oil began its descent below $100 a barrel, we kept looking for an oil-price-cut dividend. But that dividend has been hard to discern in the macroeconomic data. Part of the reason is that as a result of the rapid expansion of the production of oil from shale, total U.S. oil production had risen rapidly, and so a larger part of the economy was adversely affected by the decline in the price of oil. Another part is that investment in the equipment and structures needed for shale oil production had become an important component of aggregate U.S. investment, and that component began a rapid decline. For these reasons, although the United States has remained an oil importer, the decrease in the world price of oil had a mixed effect on U.S. gross domestic product. There is reason to believe that when the price of oil stabilizes, and U.S. shale oil production reaches its new equilibrium, the overall effect of the decline in the price of oil will be seen to have had a positive effect on aggregate demand in the United States, since lower energy prices are providing a noticeable boost to the real incomes of households.

Secular stagnation: During World War II in the United States, many economists feared that at the end of the war, the economy would return to high pre-war levels of unemployment–because with the end of the war, demobilization, and the massive reduction that would take place in the defense budget, there would not be enough demand to maintain full employment.Thus was born or renewed the concept of secular stagnation–the view that the economy could find itself permanently in a situation of low demand, less than full employment, and low growth.10 That is not what happened after World War II, and the thought of secular stagnation was correspondingly laid aside, in part because of the growing confidence that intelligent economic policies–fiscal and monetary–could be relied on to help keep the economy at full employment with a reasonable growth rate.Recently, Larry Summers has forcefully restated the secular stagnation hypothesis, and argued that it accounts for the current slowness of economic growth in the United States and the rest of the industrialized world. The theoretical case for secular stagnation in the sense of a shortage of demand is tied to the question of the level of the interest rate that would be needed to generate a situation of full employment. If the equilibrium interest rate is negative, or very small, the economy is likely to find itself growing slowly, and frequently encountering the zero lower bound on the interest rate.

Research has shown a declining trend in estimates of the equilibrium interest rate. That finding has become more firmly established since the start of the Great Recession and the global financial crisis. Moreover, the level of the equilibrium interest rate seems likely to rise only gradually to a longer-run level that would still be quite low by historical standards.

What factors determine the equilibrium interest rate? Fundamentally, the balance of saving and investment demands. Several trends have been cited as possible factors contributing to a decline in the long-run equilibrium real rate. One likely factor is persistent weakness in aggregate demand. Among the many reasons for that, as Larry Summers has noted, is that the amount of physical capital that the revolutionary information technology firms with high stock market valuations have needed is remarkably small. The slowdown of productivity growth, which as already mentioned has been a prominent and deeply concerning feature of the past six years, is another important factor.12 Others have pointed to demographic trends resulting in there being a larger share of the population in age cohorts with high saving rates.13 Some have also pointed to high saving rates in many emerging market countries, coupled with a lack of suitable domestic investment opportunities in those countries, as putting downward pressure on rates in advanced economies–the global savings glut hypothesis advanced by Ben Bernanke and others at the Fed about a decade ago.

Whatever the cause, other things being equal, a lower level of the long-run equilibrium real rate suggests that the frequency and duration of future episodes in which monetary policy is constrained by the ZLB will be higher than in the past. Prior to the crisis, some research suggested that such episodes were likely to be relatively infrequent and generally short lived.15 The past several years certainly require us to reconsider that basic assumption. Moreover, recent experience in the United States and other countries has taught us that conducting monetary policy at the effective lower bound is challenging.16 And while unconventional policy tools such as forward guidance and asset purchases have been extremely helpful and effective, all central banks would prefer a situation with positive interest rates, restoring their ability to use the more traditional interest rate tool of monetary policy.

The answer to the question “Will the equilibrium interest rate remain at today’s low levels permanently?” is also that we do not know. Many of the factors that determine the equilibrium interest rate, particularly productivity growth, are extremely difficult to forecast. At present, it looks likely that the equilibrium interest rate will remain low for the policy-relevant future, but there have in the past been both long swings and short-term changes in what can be thought of as equilibrium real rates.

Eventually, history will give us the answer. But it is critical to emphasize that history’s answer will depend also on future policies, monetary and other, notably including fiscal policy.

Markets have been roiled since the start of the year by concerns about growth in China and other emerging market economies, and about the health of large global banks.

“The tension between the markets’ tranquillity and the underlying economic vulnerabilities had to be resolved at some point. In the recent quarter, we may have been witnessing the beginning of its resolution,” said Claudio Borio, Head of the Monetary and Economic Department.

recounts how financial market turmoil has emerged and spread since the beginning of 2016.

shows how international financing flows slowed in the second half of 2015, possibly signalling a turning point in global liquidity. Banks’ cross-border claims on emerging economies fell in the third quarter, and outstanding international debt securities contracted by $47 billion in Q4, the biggest fall in three years. Emerging market net debt issuance was essentially flat in the second half of the year.

proposes an alternative perspective on the decline in cross-border bank lending to China, the main driver of the drop in cross-border claims on emerging economies. The analysis finds that the outflows ultimately resulted from lower offshore renminbi deposits and Chinese firms’ paydown of foreign currency debt both cross-border and inside China.

“The combination of reduced offshore renminbi deposits and Chinese firms’ paydown of foreign currency debt reflects the unwinding of carry trades and explains the downward pressure on China’s currency,” said Hyun Song Shin, Economic Adviser and Head of Research. “It also shows why the offshore renminbi rate trades at a discount to the onshore rate during periods of stress.”

Four special features examine a range of economic, financial and policy issues:

Morten Bech and Aytek Malkhozov (BIS)* find that modestly negative policy rates have so far been transmitted through to money markets in a similar way to positive rates. But the pass-through to key bank rates has been uneven, and there is great uncertainty about the behaviour of individuals and institutions if rates were to decline further into negative territory or remain negative for a prolonged period.

Dietrich Domanski, Michela Scatigna and Anna Zabai (BIS)* explore recent trends in household wealth inequality. Their simulation suggests that wealth inequality has risen in the advanced economies at the centre of the Great Financial Crisis. To the extent that it has boosted asset prices, monetary policy may have affected inequality in opposite ways: reducing it through rising house prices, but increasing it through higher equity prices.

Patrick McGuire and Goetz von Peter (BIS)* study the drivers of the contraction in bank credit during and after the Great Financial Crisis and find that banks which provided locally funded credit to borrowers proved to be the most stable post-crisis.

Drawing from a recent survey of major trading platforms, Morten Bech, Anamaria Illes, Ulf Lewrick and Andreas Schrimpf (BIS)* review the rising use of electronic and automated trading in fixed income markets. An important recent development has been the increase in electronic trading of corporate bonds, which has more than doubled over the last five years.

* Signed articles reflect the views of the authors and not necessarily those of the BIS.

Analysis of the count of branches by selected banks, which includes agency outlets, shows that most have reduced their footprints slightly, other than Bendigo/Adelaide Bank, who grew their footprint by 5.6% in 204-15.

Analysis of the count of branches by selected banks, which includes agency outlets, shows that most have reduced their footprints slightly, other than Bendigo/Adelaide Bank, who grew their footprint by 5.6% in 204-15. On the other hand, Bank of Queensland has reduced the number of franchise branches and recorded a drop of 8.1% in 2014-15.

On the other hand, Bank of Queensland has reduced the number of franchise branches and recorded a drop of 8.1% in 2014-15. We conclude that so far banks are not responding to the digital revolution by closing branches, although some have reconfigured existing ones into smaller and more efficient units.

We conclude that so far banks are not responding to the digital revolution by closing branches, although some have reconfigured existing ones into smaller and more efficient units. Players need to adapt more quickly to the digital world. We are past an omni-channel (let them choose a channel) strategy. Digital migration needs to become central strategy because the winners will be those with the technical capability, customer sense and flexibility to reinvent banking in the digital age.

Players need to adapt more quickly to the digital world. We are past an omni-channel (let them choose a channel) strategy. Digital migration needs to become central strategy because the winners will be those with the technical capability, customer sense and flexibility to reinvent banking in the digital age.

{kind=link}