The statement delivered today by the Governor, Glenn Stevens, to the House of Representatives Standing Committee on Economics in Canberra takes a dovish tone. We note especially the relatively optimistic note struck on employment.

The Australian economy continues to progress through a major adjustment, in the midst of testing international circumstances. The terms of trade have been falling for four years and have declined by a third since their peak – though that was a very, very high peak. They are now back to about the same level as in 2006 – still about 30 per cent above their 20th century average level.

Resources sector capital spending has been following the terms of trade with a lag. From an extraordinarily high peak – at about 8 per cent of GDP, nearly three times the peaks seen in most previous upswings – this investment has been falling for about two and a half years. By the time it is finished, this decline will probably total something like 5 per cent of GDP. We are probably now about halfway through the decline. It is having a predictable impact on those industries and regions that had earlier experienced the effects of the boom.

Resources sector exports have risen strongly as the greater capacity resulting from all the investment has been put to use. Australia now exports around three times the volume of iron ore that it did a decade ago, and around twice as much coal. A very large rise in exports of natural gas is in prospect over the next few years.

Outside the mining sector and parts of the economy most directly exposed to it, there are signs that conditions have been very gradually improving. Survey-based measures of business conditions have been a bit above their longer-run average levels for some time now, and the most recent readings are about where they were in 2010. A few of the non-mining sectors have shown quite marked improvements over the past twelve months.

To this we can add that the overall number of job vacancies in the economy has been increasing, even as employment opportunities in mining and some other areas diminish. The increase has not been rapid, but nonetheless the trend has clearly been upward for about two years. Since this time last year, moreover, we have seen a rise of about 200 000, or about 2 per cent, in employment. The labour force participation rate and the ratio of employment to population have both started to increase. The rate of unemployment, though variable from month to month, seems to have stopped rising, and it is at a level a bit lower than we had thought, six months ago, it might reach.

Of course, this performance is not uniform geographically or by industry. The two large south-eastern states show the largest increases in demand and employment, and dwelling prices, while conditions elsewhere are more subdued. By industry, the rise in employment has been strongest in services, especially those types of services delivered to households, though business services activities have also added to employment over the past year.

Monetary policy is seeking to support this transition, something it can do because inflation remains low. Very low interest rates, coupled with financial institutions wanting to lend, have played a part in the improvement in conditions in some sectors. Residential construction is running at very high levels, households are adding a little less of their incomes to savings and savers have been searching for higher returns. These are all indications of easy money at work. Cognisant of the risk that very low interest rates may foster a worrying debt build-up, regulatory initiatives are in place to maintain sound lending standards and capital adequacy. I hasten to add that the objective of such tools is not to control dwelling prices, but to contain leverage. The evidence is emerging that they are doing their job.

More recently, the significant decline in the exchange rate is starting to have more discernible effects on the pattern of spending and production. The decline over the past two years amounts to about 25 per cent against a rising US dollar and 18 per cent against the trade-weighted basket. We are hearing about the effects of this in our liaison and also seeing it in the data on such things as tourism flows as well as exports of business services. This is to be expected as the exchange rate adjusts to the change in the terms of trade.

Over the year to June, real GDP grew by 2 per cent. This was in line with our forecast of three months ago and at the lower end of our forecast range from a year ago. The effect of unusual weather conditions on exports meant that GDP as measured exaggerates both the strength in the March quarter and the weakness in the June quarter.

There are still some puzzles in reconciling what has happened to real GDP with what has happened to employment and indications from business surveys. Hopefully, those puzzles will be resolved over time.

Nonetheless, what is pretty clear is that the economy is growing, albeit not as fast as we would like, the adjustment to the decline in the terms of trade is well advanced, and non-mining activity is improving rather than deteriorating. If the latter trend continues, it is credible to think that we can achieve better output growth, particularly as we reach the later phases of the decline in mining investment. This is what is needed to bring down the unemployment rate.

As always, global factors will be important and the international setting continues to be a rather complex one. Since the last hearing, growth in the Chinese economy has continued to moderate. Growth in other parts of Asia was also weaker around the middle of the year. Reflecting these outcomes, forecasts for global growth over the period ahead are a little lower than they were six months ago.

That was the backdrop for a period of volatility in some financial markets. The unwinding of an equity market bubble in China appears to have served as the proximate trigger for a revision of equity valuations around the world. Risk appetite diminished somewhat and the currencies of many emerging market economies came under downward pressure.

Whether that financial volatility itself will serve further to dampen global growth prospects remains to be seen. Sometimes such events portend a wider set of economic events, but just as often, they don’t.

In the present instance, it is important to stress that long-term debt markets and core funding markets for financial institutions have not been impaired. These markets remain open and it is still the case that highly rated private borrowers and most sovereigns can borrow at remarkably low cost. Things could change, but at present we do not see anything approaching the dislocation of funding channels seen in serious crises.

To be sure, emerging market countries are under some pressure and some of them have specific problems that are being recognised by markets. At the same time, though, many emerging market countries have done quite a bit to improve their resilience over the years.

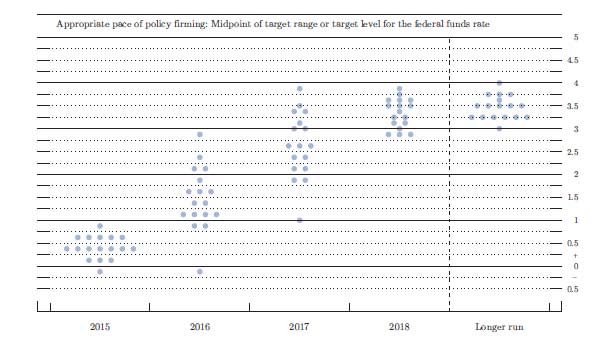

It’s also worth noting that performance in the Unites States continues to improve. Everyone knows that, eventually, this will have to be reflected in less accommodative US monetary policy. Some fretting about the first increase in US interest rates for nine years is to be expected, no matter how well telegraphed it has been. The more important factor, though, will be the pace of subsequent increases. The Federal Reserve has indicated this is expected to be very gradual, but of course that will depend on what happens with the US economy. There is a degree of irreducible uncertainty here and hence the possibility of further financial market volatility at some point. Overall though, it seems very likely that global interest rates will still be quite low for quite some time yet.

For Australia, we cannot, of course, determine our terms of trade or other forces in the global economy. We can only adjust to them. The record of adjustment in recent years is good. We negotiated the financial crisis without a major financial crisis of our own or a big downturn in economic activity. We negotiated the first two phases of the resources boom without major inflationary problems, and are part way through our adjustment to the third phase – so far without a major slump in overall economic activity. There is still a pretty good chance that we will come out of this episode fairly well, and much better than we came out of previous episodes of this type.

I now turn briefly to another area of the Bank’s responsibilities, namely the payments system. The New Payments Platform (NPP) will enable real-time, data-rich payments on a 24/7 basis for households, businesses and government agencies. The Payments System Board, having worked to facilitate the process of the private sector coming together to drive this project, supports the industry’s efforts. The Reserve Bank itself is making good progress in its own part in this project.

In the card payments area, the Bank has announced a review and we released an Issues Paper in early March. Among other things, the review contemplates the potential for changes to the regulation of card surcharges and interchange fees. It provides an opportunity to consider some of the issues raised in the Financial System Inquiry. As usual, the Bank has been consulting widely, including via a roundtable in June that included representatives from over 30 interested organisations.

The Payments System Board has asked the staff to liaise with industry participants on the possible ‘designation’ of certain card systems. A decision to designate a system is the first of a number of steps the Bank must take to exercise any of its regulatory powers in respect of a payment system, but does not commit it to a regulatory course of action. The Payments System Board will have further discussions on the case for changes to the regulatory framework at future meetings. In the event that the Board were to propose changes to the regulatory framework, the Bank would, as usual, undertake a thorough consultation process on any draft standards.

In our financial stability role, a focus has been on central counterparties, which facilitate efficient and safe clearing of some types of financial transactions. These entities are increasingly important given the way global regulatory standards have been moving. The Bank has focused on ensuring their risk management meets the highest standards and that they have the capacity to recover from financial shocks. We have also done a lot of work to ensure that our regulatory framework is appropriately recognised by regulators in other jurisdictions, which is important if we are to keep the Australian financial system connected with the global system.