Greece is set to miss the deadline on its €1.6 billion loan repayment due to the IMF. The country’s stalemate with its international creditors and the decision to hold a referendum on its bailout offer means Greece will become the first advanced economy to default to the fund in its 71-year history.

Here are nine essential things to know about the default:

1. The long-term damage may yet be minimal. If Greece is only in arrears to the IMF for a short period of time, it may be shown leniency down the line. The IMF’s policy on overdue payments does distinguish between short-term and protracted arrears.

2. This is not yet a full-blown sovereign debt default by Greece. This is still a first for an EU member state, but the IMF is keen to maintain a distinction between a country being “in arrears” and a “default”. This important semantic distinction is also made by major credit rating agencies. It means the consequences for Greece may be temporary and small, if they are able to find a speedy resolution and make the payment.

3. Being in arrears to the IMF is not a new phenomenon. Since 1997, arrears owed to the IMF that were at least six months overdue have ranged from €1.5 billion to €3 billion in any given month. This is not a position any country wants to be in, however. It places Greece in the company of countries whose governments are widely seen as dysfunctional, or even “failed states”. The only countries with IMF repayments at least six months overdue in the past decade have been Somalia, Sudan, Zimbabwe and Liberia.

4. The IMF will not allow any country to access its resources while it remains in arrears. For the IMF to be involved in any future new support package, arrears payments will first need to be settled, without the possibility of rescheduling payments. This makes Greece even more dependent on EU funding to bring liquidity back to its banks – making the outcome of the July 5 referendum even more important.

5. The IMF may now treat Greece even more harshly. It is hard to overstate how seriously the IMF takes the issue of prompt repayment of loans. In the past, countries that have deliberately missed payments have had to make significant moves towards adopting IMF policy preferences in order to regain access to its financial resources. This could include things like meeting stricter spending targets and enacting fundamental tax and pension reforms to gain future access to funds.

6. Greece is the IMF’s biggest-ever debtor. This means the stakes for the IMF are higher here than in other countries. Greece’s €1.6 billion payment would be the largest payment ever missed to the IMF.

Relations between Syriza and the IMF will not be easy going forward.EPA/Julien Warnand

7. Future relations are going to be tricky. It is difficult to see how the IMF could work with the Syriza-led coalition government after this default. There is an intense political dimension to the stalemate with the country’s creditors. The IMF does not like countries playing hardball over loan conditions. It likes populist appeals and inflammatory rhetoric even less. And it is fundamentally opposed to giving favourable deals to governments that violate their obligations to the organisation.

8. Greece’s default is a disaster for the IMF’s credibility. There is no positive spin that can be put on this. The IMF relies on countries making their payment obligations no matter what. This is why so few countries in recent years have gone into protracted arrears with the IMF. Greece’s credibility is already in dire straits, but the IMF has much to lose from its largest debtor “behaving badly”.

The IMF is already under fire from developing countries where Greece is seen as receiving special treatment. Unless the IMF brings the hammer down on Greece now, future borrowers outside of Europe will also delay IMF loan repayments when it is inconvenient.

9. Expect a severe response. If no quick resolution is found after Greece’s referendum on its bailout, the IMF must react strongly to preserve its credibility with other debtors. In the short term, the IMF is likely to step back sharply from seeking a compromise position with Greece. The IMF will insist the government makes key policy changes and meets its scheduled repayments before bailout negotiations can resume.

In the longer term, if Greece remains in arrears, the IMF could take the extreme step of suspending the country’s membership. Even if Greece didn’t need access to IMF resources, being suspended from the organisation would be another first for an advanced economy, and would see Greece’s reputation in the international financial community plummet further. Countries that remain in protracted arrears, such as Zimbabwe, have to complete an informal “staff-monitored programme” of policy conditions without funding as part of the process of normalising relations with the IMF.

Taken together, these nine points highlight the dangerous waters that Greece, the IMF, and the EU have now entered. Regardless of the referendum result, it is difficult to see the IMF cooperating with the government in Greece in the near future. Either fresh elections or a monumental change in policy direction will have to occur for that to happen.

Author: André Broome, Associate Professor of International Political Economy at University of Warwick

Beijing was in full party mode this week as delegates from 50 countries gathered to sign the articles of incorporation for the Asian Infrastructure Investment Bank (AIIB). Seven more countries are due to sign by the end of the year when the bank is expected to formally open its door for business.

This marks yet another milestone in the establishment of a China-led development lender that, according to its charter, aims to finance investments in infrastructure and other “productive” activities in Asia.

The mean and the lean

The share and governance structures of the bank have been under the radar. On one hand, China has vowed to bring something new to the table with a “new type” of multilateral development bank. On the other hand, western countries, whether those that have jumped aboard the bandwagon or those remaining on the sideline (particularly the US and Japan), have been wary. They are concerned the AIIB is part of Chinese plans to expand its geopolitical and economic interests at the expense of “international best practice”.

The proposed structure of the bank has been a compromise between China’s ambition and western concerns. Contributing almost US$30 billion of the institution’s US$100 billion capital base, China collects 30.34% of stake and 26.06% of voting rights within the multilateral institution. This makes China the largest shareholder in the bank, followed by India, Russia and Germany, with Australia and South Korea being equally fifth in shares.

What is notable is that China offered to forgo outright veto power in the bank’s routine operations, which helped win over some key founding members. However, a 26% voting right will give China veto power over “important” decisions that require a “super majority” of at least 75% of votes and approval of two-thirds of all member countries.

According to a report by the Wall Street Journal, the new lender will be overseen by a lean staff, in the form of an unpaid, non-resident board of directors. Established development banks (such as the World Bank) have been accused of being over-staffed, costly, and bureaucratic. But the AIIB approach tilts the power balance to the bank executives who will be based in Beijing and led by a Chinese-appointed governor. More institutional details must be worked out to strike a better balance between transparency, accountability, and efficiency.

Be in it to win it

The fact that a host of its allies have flocked to join China’s AIIB despite a campaign of dissuasion from Washington has sparked some serious soul searching in the power circle of the United States. Ben Bernanke, former chairman of the Federal Reserve, blamed the US Congress for the impasse in approving reforms to the IMF in granting emerging powers, particularly China, greater clout in the institution. Lawrence Summers, former US Treasury secretary, wrote recently that America’s blunder on the AIIB may be remembered as the moment it “lost its role as the underwriter of the global economic system”.

Indeed, Washington could have kicked the ball back to Beijing if it had taken a more participatory approach. The articles of association prove external concerns can be addressed through negotiation and compromise, but one needs to be at the table rather than pointing fingers from outside the room.

The current institutional framework suggests that previous fears of an unfettered Chinese influence within the bank were overblown. Yes, China could exert its veto power on important decisions, but conversations with Chinese bureaucrats suggest China is very unlikely to invoke it. After all, hijacking the agenda with its veto power has been the very way the US governs the institutions under its control, from which China is trying to distance itself.

In addition, it is less noted that the voting rights of the “Western” block, in its widest terms, (including South Korea and Singapore), are more than 30% in total. This means a mutual veto between China and western interests. In practice, this delicate balance tends to lead to negotiated consensus rather than open confrontation.

Engaging the new banker

For a long time, China has been urged to be a “responsible stakeholder” for the international community. The AIIB could well be a touchstone for China to demonstrate its ideas and ways of leadership. As Lou Jiwei, Chinese finance minister, said:

“This is China assuming more international responsibility for the development of the Asian and global economies.”

It is time to turn the table around. Instead of an endless debate on China’s strategic intentions as an emerging power, what we should do is explore ways to shape China’s behaviour to be more aligned with international expectations.

The new development bank presents a rare opportunity to achieve this in a multilateral context. So far China has largely acted on the sidelines in major international institutions, such as the World Trade Organisation and the G20 (before the Brisbane summit), and had leadership experiences in mostly regional settings, such as the Shanghai Cooperation Organisation.

The world has a new banker. However, it lacks expertise in international development finance; it lacks international governance experiences; and its ideas are untested.

These are not reasons for pessimism about the bank’s future. On the contrary, these are the very reasons we should join the initiative. By doing so, we could more effectively shape China’s view of the world and its role in the world when it is in need of ideas, expertise, and most importantly, support.

Whether China will be a friend or foe largely depends on whether we treat it as a friend or foe. After all, as Hillary Clinton once said of the US relationship with China: “How do you deal toughly with your banker?”

Author: Hui Feng, Research Fellow, Griffith Asia Institute and Centre for Governance and Public Policy at Griffith University

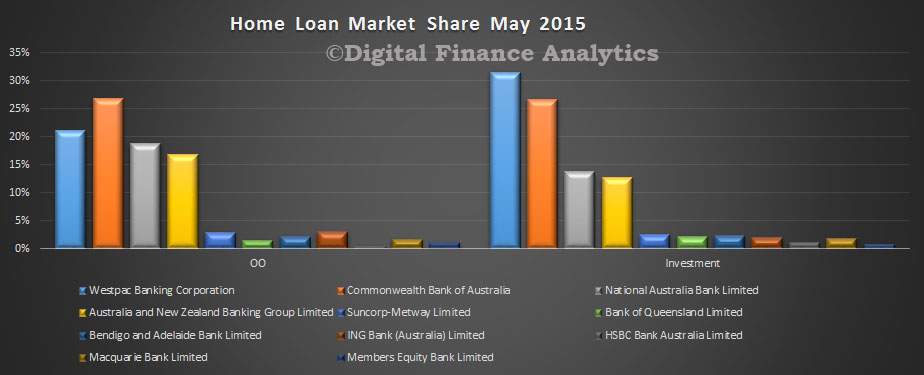

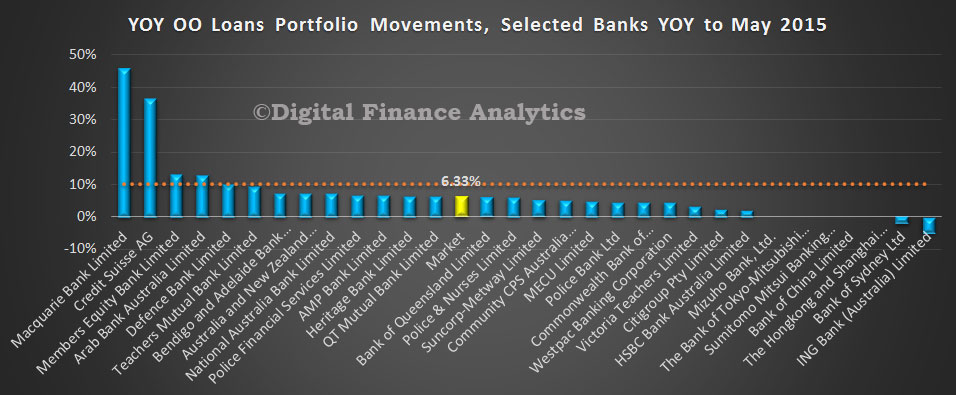

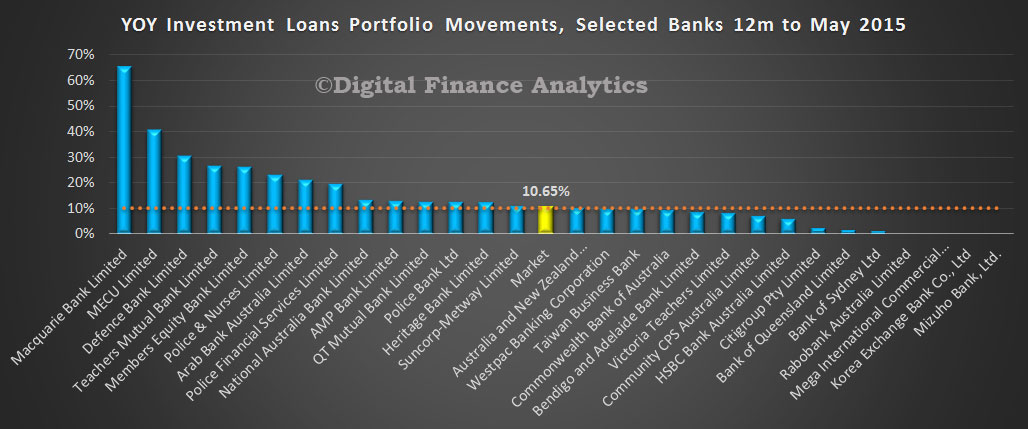

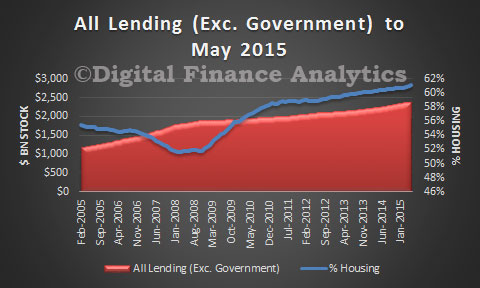

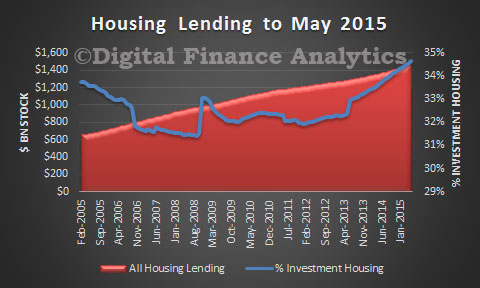

The latest APRA data on ADI’s banking statistics showed us a few interesting angles. Looking at housing first, total lending for residential property rose to $1.36 trillion, with owner occupied loans rising 0.57% in May, and investment loans rising 0.99%. These translate into year on year growth rates of 6.33% for owner occupied loans and 10.65% for investment loans, which is above the APRA “watch” rate of 10%. Housing lending for investors is still going gangbusters, as our earlier analysis from the RBA confirmed. The difference between the $1.36 trillion and the $1.47 trillion is the non bank sector.

Looking in more detail at the individual lenders, CBA still leads the majors in the owner occupied loan stakes, and Westpac is ahead on investment mortgages, by a distance.

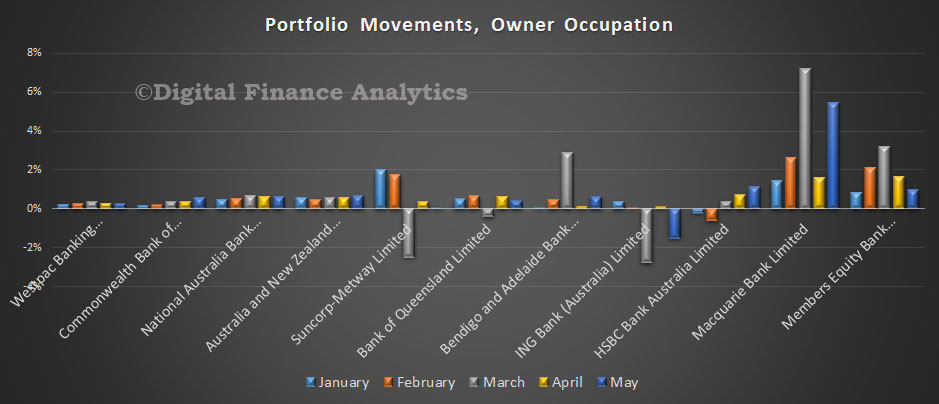

More detailed portfolio analysis shows that ANZ and NAB have been more aggressive on owner occupied loan growth than the other majors, but some of the smaller players are still making hay; Macquarie and Members Equity in particular.

The average growth rate over the last 12 months was 6.33%, and we see many players below this, and ING’s portfolio share falling.

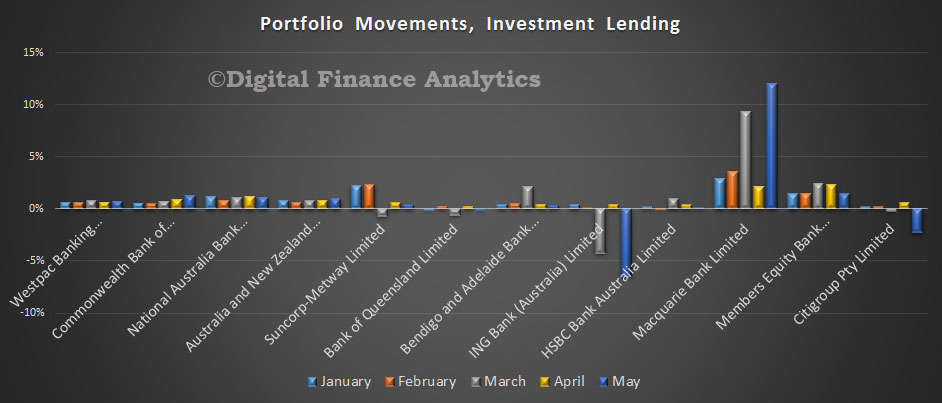

Turning to portfolio movements on investment loans, Westpac has slowed their growth relative to the other majors, and Macquarie is still lending hard.

The market average growth over the past year was 10.65%, above the 10% APRA “alert” level. Some of the smaller players are well above (and we think APRA was concerned about some of these players and their rapid growth). We also see several of the majors above the threshold and they might expect to receive a “please explain” letter from the regulator. That said, no-one is clear on when the 10% hurdle should be measured from, so they might have until December to get into line. If they do, they would be required to slow their growth in coming months. There are some signs of discounts falling and LVR thresholds lowering. The regulatory noose may be tightening, but so far to little effect.

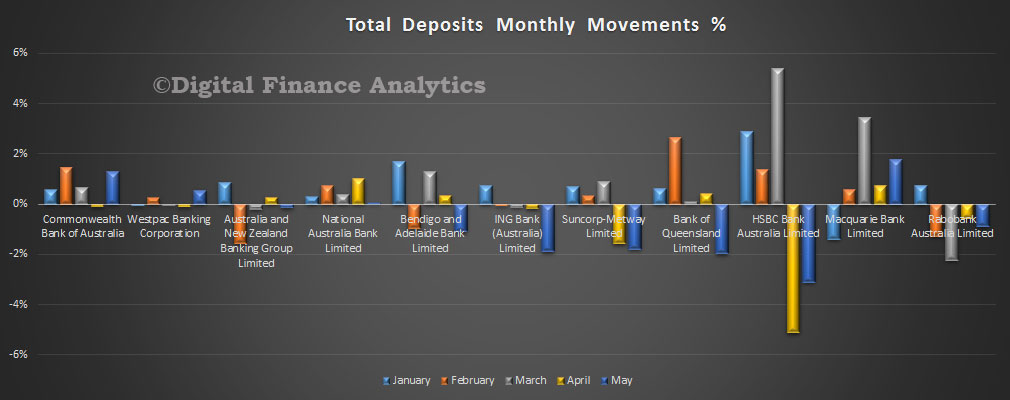

Turning to deposits, we saw growth of 0.04% to $1,83 trillion.

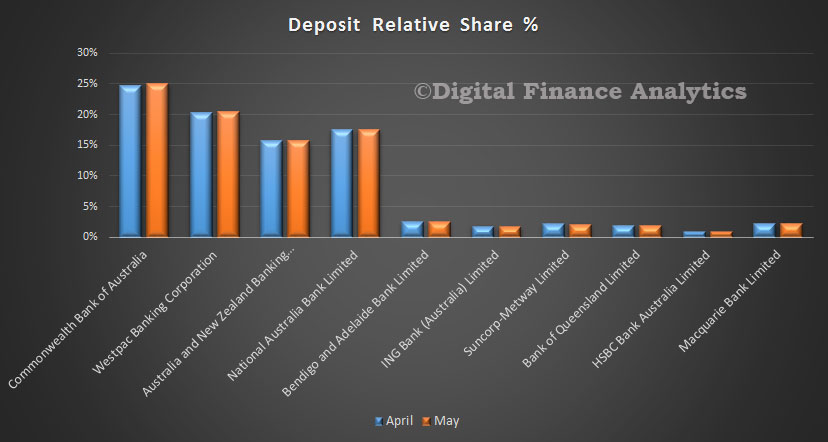

CBA picked up share a little at the expense of some of the smaller lenders, including ING, Bendigo, Suncorp, Bank of Queensland and Rabobank. Many of the smaller players have cut their deposit rates harder to “manage” profitability (i.e. squeeze savers).

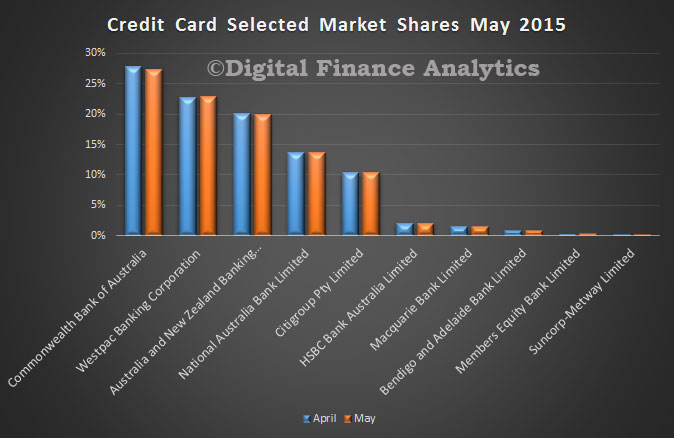

Finally, credit cards, total borrowing fell 0.38% in the month, to $41.2 billion. Little overall change in position, though we note CBA lost a little share, whilst Westpac gained slightly. The current focus on card interest rates may have an impact in coming months, but little impact so far.

The RBA lending aggregates for May 2015 tell the ongoing story of housing lending dominated by investment loans, and housing becoming an ever larger proportion of total bank debt. Total bank lending stock grew to $2.4 trillion in May, with $1.47 trillion in housing, growing at 0.42% in the month, business lending up 0.35% to $792 million and personal lending (excluding housing) down a little to $141 million. Overall housing lending was 61.1% of all bank lending (excluding government loans) – an all time high.

Looking more closely at housing, the $1.47 trillion was split into owner occupied lending of $958 million, up 0.42% in the month, and investment lending of $508m, up 0.81%, showing again the disproportionate focus on investment property.

We can but reiterate our two key points. First, housing lending is squeezing out productive lending to business, and in so doing continues to inflate banks balance sheets, and house prices, neither productive economically speaking; whilst business finds it hard to get the support it needs to create productive growth. In the context of a mining slow down, this is a serious problem, which will not be addressed by $20k capital write-offs. Capital rules favour home lending too much.

Second, the distortions created by ever larger bands of property investors, makes it harder for younger families to buy a home – indeed many are going direct to the investment sector in a bid to get a look in. However, those who analyse relative risks in an investment portfolio versus an owner occupied portfolio indicate there are higher risks in the investment pools, especially in a down turn. These risks are not recognised by the current Basel rules, and such risks are not currently priced into investment loans.

The data so far does not demonstrate any impact from the “tighter” APRA rules for investment lending, maybe next month? Even if one or two banks slow their investment lending growth rates and tighten their underwriting criteria, others will happily step in.

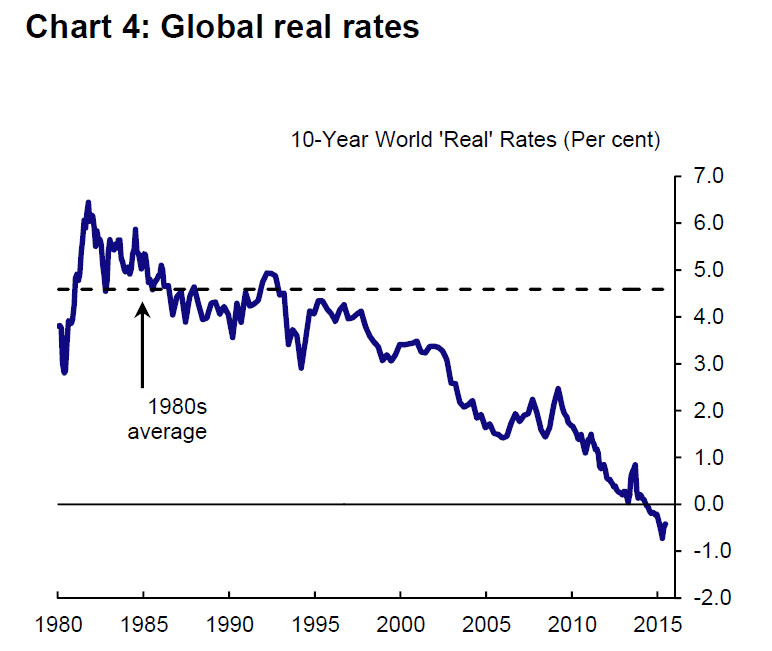

In a speech at the Open University, The Bank of England’s Chief Economist, Andy Haldane explores why interest rates in advanced economies have got “stuck” and how policymakers should respond. Highly relevant given the recent BIS report which said there was too much reliance on risky low interest rate monetary policy.

Official interest rates in the major economies remain stuck at unprecedentedly low levels. Central banks have made vigorous attempts to dislodge them, including through special liquidity schemes, asset purchases and forward guidance. Yet interest rates remain stuck. This stickiness in interest rates has surprised both policymakers and financial markets. After they hit their floor, financial markets expected official rates in the US to unstick in 6 months, in the UK in 10 months, in Japan in 13 months and in the euro-area in 14 months. But they have remained stuck: in Japan for over 20 years and in the US, the UK and the euro-area for over 6 years. Indeed, the expected time to lift-off remains as many months away today as when rates first hit their floor: in the US 9 months, in the UK 10 months, in the euro-area 34 months, in Japan 72 months. In Australia, rates are as low as they have been in living memory, and some advocate further cuts still.

Andy explores two possible factors that may have contributed to current low levels of interest rates: “dread risk and recession risk. The first generates an elevated perception of risk, the second an asymmetric balance of risk. Both are relevant to explaining the path of interest rates, the likely fortunes of the economy and the optimal setting of monetary policy.”

The effects of dread risk have, Andy argues, “proved lasting and durable.” The fear of a further financial crisis and the risk-averse behaviours that follow help “explain the sluggishness of the recovery, and the adhesiveness of interest rates, since the crisis.” And, “if the past is any guide, these scars may heal only slowly.”

In a discussion of recession risk, Andy considers what we can expect for future growth on the basis of past trends. He finds that “the probability of an expansion lasting for longer than 10 years is, on past evidence, less than 10%.”

“If a recession were to strike in the period ahead, a relevant question for monetary policy is how much room for manoeuvre might be necessary to cushion its effects.” Comparing the magnitude of previous loosening cycles to the current path of the yield curve Andy finds, “recession probabilities exceed interest rate threshold probabilities by a factor of anywhere between 1.5 and 4.”

“Put differently, based on these estimates there is a considerably greater chance of interest rates needing to be cut to their floor to meet recessionary needs than of them gliding back to levels that could safely cushion a recession. Even after interest rates have lifted off from their floor, it is more likely than not they may return there over a ten-year horizon.”

What, therefore, are implications for monetary policy of continued dread and recession risk? Using the forecast from the May Inflation Report Andy has updated the interest rate trajectories he produced earlier this year. “As then, they suggest the optimal path for interest rates involves an immediate cut in rates for about a year, which pushes inflation back to target and closes the output gap. Thereafter, interest rates rise gradually in line with the market curve.”

However, the trajectories are illustrative and may “underplay the effects of risk” such as the dread risk and recession risk he has focused on here. He argues these risks have led to a cautious response to the recovery by both households and, to some extent, businesses which may “skew growth risks to the downside”. As a result, while April’s wage data was “encouraging news… one swallow does not a summer make.” “Wage growth is causing some fluttering, but not in this dovecote.”

This, in combination, with the downside risk to the MPC meeting its 2% inflation target two years hence, gives Andy “considerable sympathy” with the argument that interest rates should be “lower for longer” to manage the risks from raising rates too soon. A rate rise “however modest” would be a further example of bad news to already cautious consumers: “A policy of early lift-off could be self-defeating. It would risk generating the very recession today it was seeking to insure against tomorrow.”

This leads Andy to conclude: “my judgement on the appropriate monetary stance in the UK is relatively little altered from earlier in the year. The current level of interest rates remains, in my view, appropriate to assure the on-going recovery and to insure against potential downside risks to demand and inflation. Looking ahead, I have no bias on either the size or direction of future interest rate moves.”

As negotiations go down to the wire, the IMF is once again being cast in the role of dictator. It is the enforcer of controversial structural reforms to a country experiencing severe economic distress, the social consequences of which have been disastrous over the last seven years. In many ways, however, the IMF is used as a scapegoat for promoting unpopular policy choices by the elected politicians and unelected bureaucrats of the eurozone who are well aware of the organisation’s fundamental commitment to favouring fiscal consolidation.

As the June 30 deadline approaches for Greece’s €1.5 billion debt repayment, here are the five key things to know about the IMF’s position.

1. Keeping the eurozone in tact

Keeping the eurozone together is a paramount concern for IMF negotiators. They will therefore almost certainly not recommend that Greece consider taking the nuclear option of abandoning the euro, which would be the likely result of defaulting on its debts.

This is because of the risk of systemic instability. And also because of the potential for eurozone rules to act as an external constraint on future economic policy choices in Greece – which the IMF has long seen as in need of further structural reforms and greater fiscal discipline.

Plus the organisation has a long history of exhibiting a status quo bias whenever it has been faced with the possibility of regional monetary distintegration, such as in the case of the ruble zone during 1991-93.

2. Reputational costs

The IMF is acutely aware of the reputational costs it faces if it is blamed for a sovereign default by Greece – let alone if Greece is eventually forced out of the euro. Here, the stakes involved with the terms of the Greek bailout, and whether or not Greece remains in the euro, differ markedly for the IMF compared with its “Troika” partners, the European Central Bank and the European Commission.

After the IMF took the lead in coordinating a multilateral response to the Asian financial crisis in 1997-98 it shouldered most of the blame for policy mistakes that inflamed the crisis. This motivated many countries to shun the organisation over the next decade until the onset of the global financial crisis in 2008.

The IMF’s Lagarde must take into account other eurozone economies.EPA/Olivier Hoslet

There can be no real winners from the high stakes poker match between Greece, the EU, and the IMF that has been running since the Syriza-led coalition came to power in January. But how the IMF’s reputation fares in the aftermath of the eurozone crisis will have a significant impact on its future crisis management role, both in Europe and beyond.

This is one of the reasons behind the IMF’s decision in 2013 to publicly admit to making notable errors in underestimating the damage that the initial round of austerity policies in 2010-11 would do to the Greek economy. This acknowledgement helped to place a small amount of distance between the IMF’s position and the apparent commitment of EU leaders to austerity-at-any-cost, while reducing the potential for the IMF to be used as the scapegoat for mistakes also made by its Troika partners.

A concern with protecting its reputation is also why the IMF has been at pains to emphasise in press briefings that it has pushed for “social fairness and social balance” in the design of reforms to the Greek pension system.

3. Greece’s commitment to structural reform

How flexible the IMF will be in reaching a compromise with the Greek government depends in large part on how they assess Greece’s commitment to implementing structural economic reforms.

Over the five months since it was elected, the Syriza government has demonstrated little or no political will for implementing major overhauls of the pensions system and the tax system, which are key concerns for the IMF.

A broader issue here is the IMF’s principle of “uniformity of treatment” for borrowers. There will inevitably be internal debates over how much the IMF should compromise with Greece over its bailout terms. But this principle constrains how flexible the organisation can be seen to be for any individual country, to avoid future borrowers also demanding softer loan conditions such as through looser policy targets or a slower pace of structural reforms.

4. Views on tax reform

The IMF’s long-standing views on tax reform also limit its flexibility towards Greece’s recent proposals for tax rises. Here, as in other countries, the IMF is seeking a substantial broadening of the tax base through the expansion and simplification of consumption taxes.

It is concerned that tax increases alone cannot plug the fiscal gap in a country with a notoriously leaky tax system. Though much of Syriza’s proposed changes may increase tax revenue in the short-term, the IMF is more interested in structural reform of the tax system that can help in shaping long-term policy.

In the meantime, cutting public spending in Greece, from the IMF’s perspective, is both easier for the government to achieve as a stopgap solution and is a better indicator for the country’s creditors of the government’s political commitment to implementing painful reforms.

5. Leadership

During the four years that former French finance minister Christine Lagarde has served as the IMF Managing Director, her public comments on Greece have gradually moved towards recognition of the need for debt relief. This is a significant shift from the organisation’s official position in 2010-11, and has expanded the negotiating space available to the IMF. Meanwhile it has placed pressure on its Troika partners to deliver some form of debt relief down the track.

Yet despite growing acknowledgement that debt relief will need to be part of any long-term agreement to achieve fiscal stability in Greece, this is only likely to be formally placed on the negotiating table after the government first agrees to a comprehensive package of structural reforms.

The end game

As the negotiations over Greece’s economic future enter the end game, the chasm between the debtor country and its creditors remains both wide and deep. The carrot of debt relief is only likely to materialise once substantial progress is made on implementing the structural reforms that have been deemed unacceptable by Greece’s Syriza government.

It is hard to imagine how a workable long-term solution can be fudged at this stage of the process. This would need either the creditors relaxing their demands for continued austerity or the government caving in and accepting the structural reforms it campaigned against in the election in January. The former is highly unlikely, given the signal this would send to other economies. The latter seems equally unlikely and if it happens might result in the collapse of the government and fresh elections, starting the messy process of muddling through negotiations all over again.

Author: André Broome, Associate Professor of International Political Economy at University of Warwick

Greece will hold a referendum on July 5 on whether the country should accept the bailout offer of international creditors. The government’s decision to reject what was on offer and call the referendum is ultimately an attempt to take charge of its domestic policy and reaffirm its credibility with voters.

Although Greece is hard strapped for cash this is clearly a political decision with profound consequences for the future of the European Union. It is also the right one.

This is not merely useful as a negotiating tactic for obtaining a better deal with its creditors, as many commentators might suggest. The coalition of the left, Syriza, had no choice but to oppose further measures that would lock its economy into a deflationary spiral, the trappings of which are destroying Greek society.

The Greek position

Elected with the mandate to end the savage austerity policies already imposed, Syriza could hardly accept the further cuts demanded. These include cuts in income support for pensioners below the poverty line and a VAT hike of up to 23% on food staples. Even more onerous was the demand that Greece should deliver a sustained primary budget surplus of 1% for 2016, gradually increasing to 3.5% in the following years when its economy has already been contracting for six years.

By most counts the austerity policies imposed by Greece’s creditors in 2010 in exchange for the bailout money (of €240 billion) have been an abject economic and moral failure. The International Monetary Fund itself has acknowledged “a notable failure” in managing the terms of the first Greek bailout, in setting overly optimistic expectations for the country’s economy and underestimating the effects of the austerity measures it imposed.

Yet in the terms presented to Greece by their creditors there is no commitment to reducing Greece’s crippling debt (which all commentators acknowledge is unrepayable). Nor is there any tangible proposal for rebuilding the Greek economy.

Germany, France, and the EU, aided by the IMF and ECB, continue to insist on implementing policies that have so manifestly failed Greece. They do so to avoid having to justify the massive bailouts of their own financial systems – shifting the burden from banks to taxpayers – if Greece fails to make the repayments. The leading EU partners must not be seen to act leniently towards Greece as this might encourage anti-austerity parties Spain and elsewhere.

Leader of Spain’s anti-austerity party, Podemos, Pablo Iglesias, rallying with Alexis Tsipras.EPA/Orestis Panagiotou

Broken Europe

But the social and political costs of these policies have put the legitimacy of the entire European integration project in question. By being locked into austerity policies, Europe is tearing itself apart.

This brings to the fore the faulty institutional framework that has exacerbated these issues. European integration was conceived by a set of elites, while many EU citizens have never fully embraced the idea: the EU tends to be regarded as an economic entity rather than a cultural or social one. The “ever closer union” remains an aspiration, while EU institutions patch up compromises between its most powerful members.

The ill-thought and haphazard implementation of the common currency is perhaps the most costly compromise of all. The Greek government is therefore right to ask for generous debt relief to allow the economy to have a fresh start in exchange for reforms that will address the perennial problems of corruption and inequality that bedevil Greek society.

The right decision

Greece has many problems – including unfair taxation (64% of taxes are paid by salaried employees and pensioners), corrupt elites who have governed the country for at least four decades with fellow European governments repeatedly turning a blind eye to their flouting of rules, and the oligarch-owned media which are neither independent nor free. But accepting the bailout would only feed into the system that got Greece into this crisis.

Meanwhile, the newcomer to Greek politics, Syriza, has been told it will only receive the funds agreed under the previous bailout terms if it is ready to implement further policies that will decimate the poor and impoverish the middle class even more. Cutting pensions, many of which are already below the eurozone average when almost one in two of them are facing poverty, would be a mistake.

So would conceding to the firing of an additional 150,000 public sector workers when their overall headcount has already been reduced by 161,000 since 2010 – a 19% reduction, according to the IMF.

Contrary to popular belief, the number of public sector employees as a percentage of the workforce in Greece is 14% below the OCED average, but austerity has had an even more disastrous impact on employment in the private sector, with an estimated 400,000 businesses closing down in the past five years.

No country has ever succeeded in emerging from financial crisis by means of austerity. Further austerity would have made the impossibly bad situation that Greece is in worse still. In rejecting the creditors’ further demands, the Greek government stands for the working people of Greece – and Europe too.

Author: Marianna Fotaki, Network Fellow, Edmond J Safra Center for Ethics, Harvard University and Professor of Business Ethics at University of Warwick,

Since our last episode, the crisis in Greece has escalated further. Negotiations between the government and its creditors collapsed over the weekend, and restrictions on bank withdrawals will now follow.

The next step is for the government to issue the equivalent of IOUs to pay salaries and pensions. The country is seemingly on the slippery slope to exiting the euro.

Many of us doubted that it would come to this. In particular, I doubted that it would come to this.

Nearly a decade ago, I analyzed scenarios for a country leaving the eurozone. I concluded that this was exceedingly unlikely to happen. The probability of a Grexit, or any Otherexit, I confidently asserted, was vanishingly small.

My friend and UC Berkeley colleague Brad DeLong regularly reminds us of the need to “mark our views to market.” So where did this prediction go wrong?

Why a euro exit didn’t make sense

My analysis was based on a comparison of economic costs and benefits of a country exiting the euro. The costs, I concluded, would be severe and heavily front-loaded.

Raising the possibility, however remote, of exit from the euro would ignite a bank run in said country. The authorities would be forced to shutter the financial system. Economic activity would grind to a halt. Losing access to not just their savings but also imported petrol, medicines and foodstuffs, angry citizens would take to the streets.

Not only would any subsequent benefits, by comparison, be delayed, but they would be disappointingly small.

With the government printing money to finance its spending, inflation would accelerate, and any improvement in export competitiveness due to depreciation of the newly reintroduced national currency would prove ephemeral.

In Greece’s case, moreover, there is the problem that the country’s leading export, refined petroleum, is priced in dollars and relies on imported oil, which is also priced in dollars. So much for the advantages of a depreciated currency.

Agricultural exports for their part will take several harvests to ramp up. And attracting more tourists won’t be easy against a drumbeat of political unrest.

What went wrong?

How did Greece end up in this pickle? Some say that the specter of a bank run was no longer a deterrent to exit once that bank run started anyway due to the deep depression into which the Greek economy had sunk.

But what is remarkable is how the so-called bank run remained a jog – it was still perfectly manageable until the Greek government called its referendum on the terms of the bail out deal offered by international creditors, negotiations broke down and exit became a real possibility.

Nonperforming loans — ones that are in default or close to it — were already rising, to be sure, but the banks still had all the liquidity they needed. The European Central Bank supported the Greek banking system with emergency liquidity assistance (ELA) right up to the very end of June. Only when Greece stopped negotiating did the Central Bank stop increasing ELA. And only then did a full-fledged bank run break out.

So I stand by the economic argument. Where I need to mark my views to market, however, is for underestimating the role of politics. In particular, I underestimated the extent of political incompetence – not just of the Greek government but even more so of its creditors.

In January Syriza had run on a platform of no more spending cuts or tax increases but also of keeping the euro. It should have anticipated that some compromise would be needed to square this circle. In the event, that realization was strangely late in coming.

And Prime Minister Alexis Tsipras and his government should have had the courage of its convictions. If it was unwilling to accept the creditors’ final offer, then it should have stated its refusal, pure and simple. If it preferred to continue negotiating, then it should have continued negotiating. The decision to call a referendum in midstream only heightened uncertainty. It was a transparent effort to evade responsibility. It was the action of leaders more interested in retaining office than in minimizing the cost to the country of the crisis.

A hard lesson learned

Still, this incompetence pales in comparison with that of the European Commission, the ECB and the IMF.

The three institutions opposed debt restructuring in 2010 when the crisis still could have been resolved at low cost. They continued to resist it in 2015, when a debt write-down was the obvious concession to Mr Tsipras & Company. The cost would have been small. Pretending instead that Greece’s debts could be repaid hardly enhanced their credibility.

Instead, the creditors first calculated the size of the primary budget surpluses that Greece would have to run in order to hypothetically repay its debt. They then required the government to raise taxes and cut spending sufficiently to produce those surpluses.

They ignored the fact that, in so doing, they consigned the country to an even deeper depression. By privileging their own balance sheets, they got the Greek government and the outcome they deserved.

The implication is clear. Never underestimate the ability of politicians to do the wrong thing. I will try to remember next time.

Author: Barry Eichengreen, Professor of Economics and Political Science at University of California, Berkeley

According to Moody’s, the Basel III disclosure standards which were finalised recently, are positive for creditors of internationally active banks because they will improve transparency into bank funding, allowing investors to assess the adequacy and reliability of funding for a bank’s least-liquid assets, including loans.

Detailed NSFR disclosure is positive for bank investors evaluating a bank’s liquidity and stable funding position since the ratio is distinct from the LCR, measuring a different type of funding risk. The LCR measures whether banks hold enough high-quality liquid assets (HQLA) that could be liquidated to cover stressed cash outflows (e.g., deposit outflows and maturing liabilities that cannot be rolled over) over a 30-day period. The NSFR measures whether funding of longer duration adequately supports less liquid longerterm assets such as loans.

The NSFR template aligns with the LCR disclosure template, which for investors provides some consistency in evaluating short- and long-term liquidity risks. Both, for example, require disclosure of stable and less stable retail deposits, and wholesale deposits used for operational purposes. These disclosures are used to calculate stressed cash outflows in the LCR, and in the NSFR are categories of available stable funding. The Basel Committee noted that in formulating the template, it balanced usability of disclosure with “undesirable dynamics during stress.” Although the Basel Committee did not specify exactly how it achieved the trade-off in the disclosure framework, this has likely restricted funding transparency to some degree.

In addition to a standardized reporting template, the NSFR disclosure standards require qualitative disclosures that are important in evaluating a bank’s stable funding position. The disclosure of interdependent assets and liabilities, which are assigned 0% required stable funding and available stable funding factors in the NSFR calculation, is key because the interdependency is judged by national discretion and could drive significant differences in ratios across banks. The disclosures also will describe drivers of changes in the NSFR categories across reporting periods, which should help investors understand how a bank’s NSFR has changed over time.

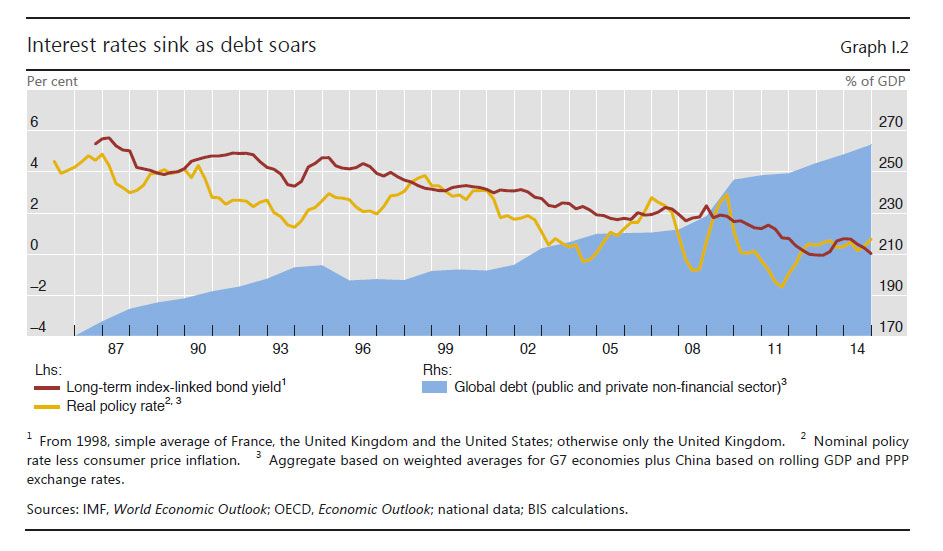

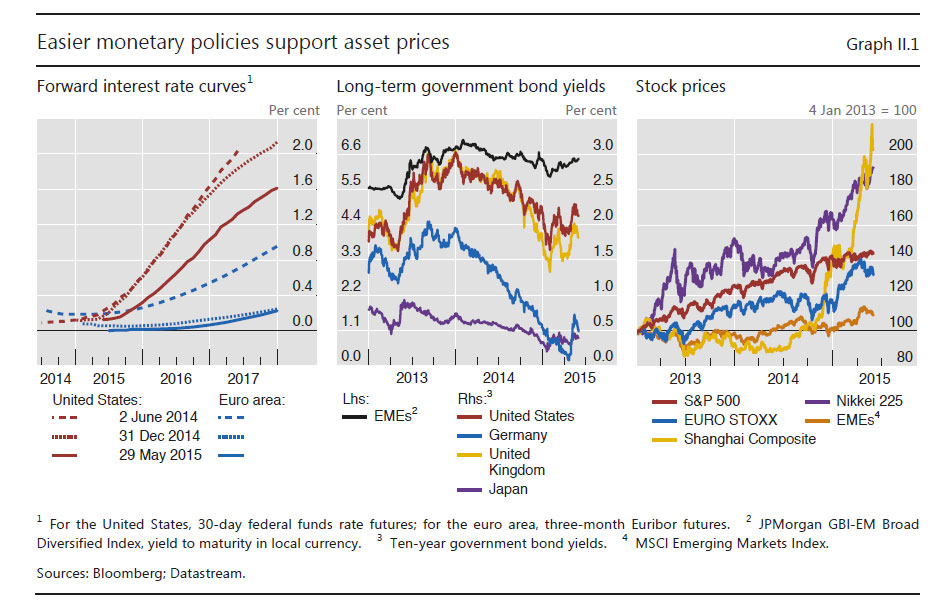

The 85th Annual Report from the Bank for International Settlements has just been released. This is an important document because in its economic chapters the authors attempt to get to grips with some of the critical issues creating uncertainty in the global economy and the financial system. Here is a summary of the main arguments.

Chapter I: Is the unthinkable becoming routine?

Globally, interest rates have been extraordinarily low for an exceptionally long time, in nominal and inflation-adjusted terms, against any benchmark. Such low rates are the most remarkable symptom of a broader malaise in the global economy: the economic expansion is unbalanced, debt burdens and financial risks are still too high, productivity growth too low, and the room for manoeuvre in macroeconomic policy too limited. The unthinkable risks becoming routine and being perceived as the new normal. This malaise has proved exceedingly difficult to understand. The chapter argues that it reflects to a considerable extent the failure to come to grips with financial booms and busts that leave deep and enduring economic scars. In the long term, this runs the risk of entrenching instability and chronic weakness. There is both a domestic and an international dimension to all this. Domestic policy regimes have been too narrowly concerned with stabilising short-term output and inflation and have lost sight of slower-moving but more costly financial booms and busts. And the international monetary and financial system has spread easy monetary and financial conditions in the core economies to other economies through exchange rate and capital flow pressures, furthering the build-up of financial vulnerabilities. Short-term gain risks being bought at the cost of long-term pain. Addressing these deficiencies requires a triple rebalancing in national and international policy frameworks: away from illusory short-term macroeconomic finetuning towards medium-term strategies; away from overwhelming attention to near-term output and inflation towards a more systematic response to slowermoving financial cycles; and away from a narrow own-house-in-order doctrine to one that recognises the costly interplay of domestic-focused policies. One essential element of this rebalancing will be to rely less on demand management policies and more on structural ones, so as to abandon the debt-fuelled growth model that has acted as a political and social substitute for productivity-enhancing reforms. The dividend from lower oil prices provides an opportunity that should not be missed. Monetary policy has been overburdened for far too long. It must be part of the answer but cannot be the whole answer. The unthinkable should not be allowed to become routine.

Chapter II: Global financial markets remain dependent on central banks

Accommodative monetary policies continued to lift prices in global asset markets in the past year, while diverging expectations about Federal Reserve and ECB policies sent the dollar and the euro in opposite directions. As the dollar soared, oil prices fell sharply, reflecting a mix of expected production and consumption, attitudes to risk and financing conditions. Bond yields in advanced economies continued to fall throughout much of the period under review and bond markets entered uncharted territory as nominal bond yields fell below zero in many markets. This reflected falling term premia and lower expected policy rates. The fragility of otherwise buoyant markets was underscored by increasingly frequent bouts of volatility and signs of reduced market liquidity. Such signs were perhaps clearest in fixed income markets, where market-makers have scaled back their activities and market-making has increasingly concentrated in the most liquid bonds. As other types of players, such as asset managers, have taken their place, the risk of “liquidity illusion” has increased: market liquidity appears ample in normal times, but vanishes quickly during market stress.

Chapter III: When the financial becomes real

Plummeting oil prices and a surging US dollar shaped global activity in the year under review. These large changes in key markets caught economies at different stages of their business and financial cycles. The business cycle upswing in the advanced economies continued and growth returned to several of the crisis-hit economies in the euro area. At the same time, financial downswings are bottoming out in some of the economies hardest-hit by the Great Financial Crisis. But the resource misallocations stemming from the pre-crisis financial boom continue to hold back productivity growth. Other countries, less affected by the crisis, notably many EMEs, are experiencing different challenges. The shift in global conditions has coincided with slowing output growth and peaks in domestic financial cycles. There is the danger that slowing growth in EMEs could expose financial vulnerabilities. Better macroeconomic management and more robust financial structures, including longer debt maturities and reduced exposure to currency risk, have increased resilience. But the overall amount of debt has increased and the shift from banks to capital market funding could raise new risks.

Chapter IV: Another year of monetary policy accommodation

Monetary policy continued to be exceptionally accommodative, with many authorities easing or delaying tightening. For some central banks, the ultra-low policy rate environment was reinforced with large-scale asset purchase programmes. In the major advanced economies, central banks pursued significantly divergent policy trajectories, but all remained concerned about the dangers of inflation running well below inflation objectives. In most other economies, inflation rates deviated from targets, being surprisingly low for some and high for others. The deviation of inflation from expected levels and questions surrounding the sources of price changes underscore an incomplete understanding of the inflation process, especially regarding its medium- and long-term drivers. At the same time, signs of growing financial imbalances around the globe highlight the risks of accommodative monetary policies. The persistence of those policies since the crisis casts doubt on the suitability of current monetary policy frameworks and suggests that resolving the tension between price stability and financial stability is the key challenge. This puts a premium on accounting for financial stability concerns much more systematically in monetary policy frameworks.

Chapter V: The international monetary and financial system

The suitable design of international monetary and financial arrangements for the global economy is a long-standing issue. A key shortcoming of the existing system is that it tends to heighten the risk of financial imbalances, leading to booms and busts in credit and asset prices with serious macroeconomic consequences. These imbalances often occur simultaneously across countries, deriving strength from international spillovers of various types. The global use of the dollar and the euro allows monetary conditions to affect borrowers well beyond the respective issuing economies. Many countries also import monetary conditions when setting policy rates to limit interest rate differentials and exchange rate movements against the major currencies. The global integration of financial markets tends to reinforce these dynamics, by allowing common factors to drive capital flows and a common price of risk to move bond and equity prices. Policies to keep one’s own house in order by managing financial cycles would help to reduce such spillovers. In addition,

central banks need to better internalise spillovers, not least to avoid the effects of their actions spilling back into their own economies. Moving beyond enlightened self-interest would require international cooperation on rules constraining domestic policies.

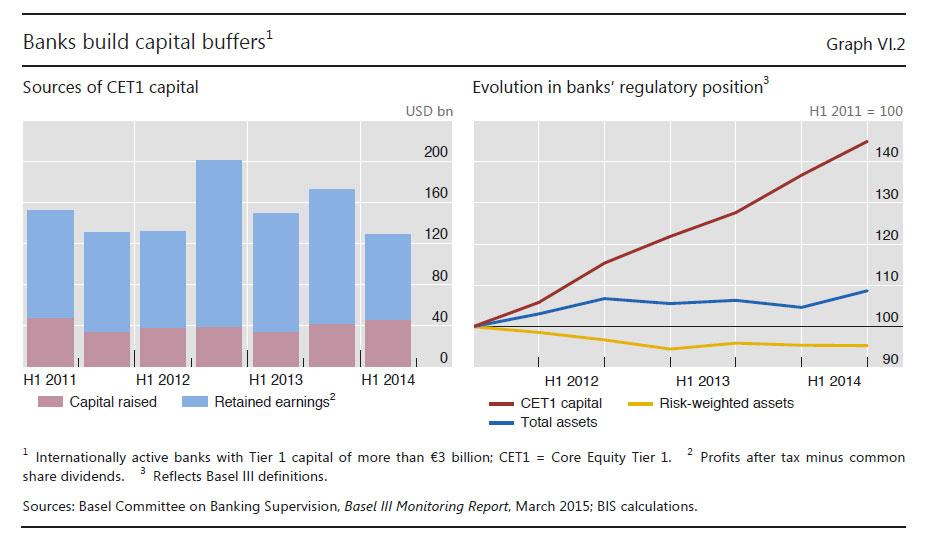

Chapter VI: Old and new risks in the financial landscape

Risks in the financial system have evolved against the backdrop of persistently low interest rates in advanced economies. Despite substantial efforts to strengthen their capital and liquidity positions, advanced economy banks still face market scepticism. As a result, they have lost some of their traditional funding advantage relative to potential customers. This adds to the challenges stemming from the gradual erosion of interest income and banks’ growing exposure to interest rate risk, which could weaken their resilience in the future. By contrast, EME banks have so far benefited from market optimism amid buoyant conditions that may be masking the build-up of financial imbalances. For their part, insurance companies and pension funds have faced ballooning liabilities and muted asset returns. Asset-liability mismatches are weakening institutional investors and threaten to spill over into the real economy. As these investors offload risks onto their customers and banks retreat from traditional intermediation, asset managers are taking on an increasingly

important role. Regulatory authorities are carefully monitoring the financial stability implications of the growing asset management sector.