We ran our regular live Q&A event last night, and had the biggest audience ever (thanks to all those who took part).

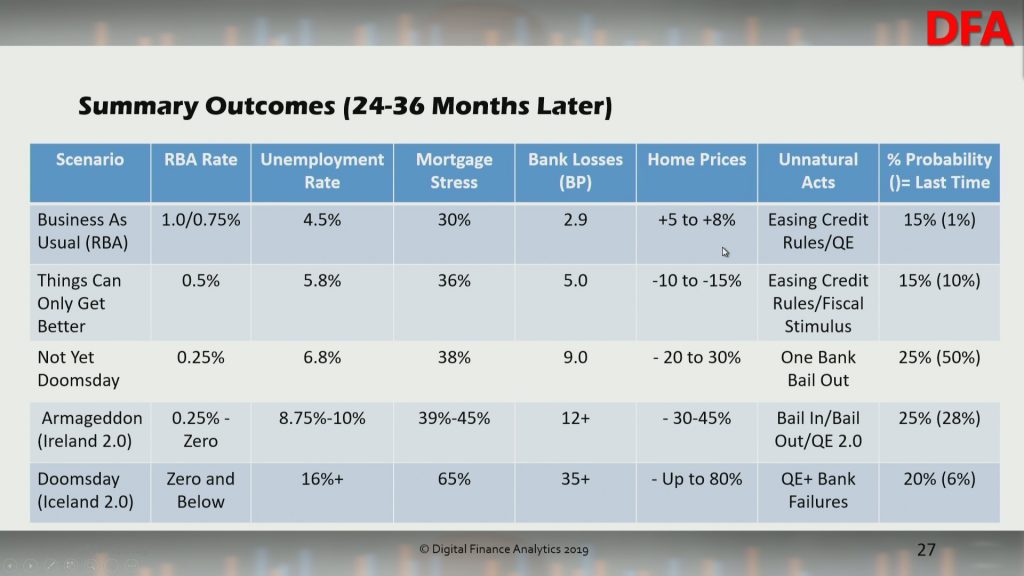

During the show we discussed the latest data from the RBA, ABS and Moody’s, and our updated scenarios. In the current “risk-on” environment, and with the RBA’s pivot to lower rates, QE and lifting the money supply incorporated into our modelling, plus the heightened international risk profiles; there are some big changes to our scenarios.

Given the RBA (and the FED) have flipped to more QE, the future could play out a number of ways over the next 2-3 years. Indeed, if the RBA does get unemployment down to 4.5%, it is possible home prices will be higher by then.

We are expecting a small bounce, but then further falls in home prices as the broader economy weakens, and the risks from an international crisis rise further. But remember average rises or falls mask significant variations. We discuss specific examples on the show where prices have already dropped more than 30%.

You can watch the edited version of the show and our rationale for the scenario revision.

Alternatively, the original stream, including the live chat replay is available.

And we also included a view behind the scenes during the session.

Macquarie Securities (Australia) Limited (‘Macquarie’) has paid a penalty totalling $300,000 to comply with an infringement notice given by the Markets Disciplinary Panel (‘the MDP’).

The MDP had reasonable grounds to believe that Macquarie contravened

the market integrity rules that deal with the provision of regulatory

data to ASX and Chi-X.

Over a four-year period from July 2014 to July 2018, Macquarie

transmitted approximately 42 million orders to ASX and Chi-X that

included incorrect regulatory data or omitted required regulatory data.

Over the same period, Macquarie also submitted approximately

377,000 trade reports to ASX and Chi-X with the same deficiencies.

The kinds of regulatory data that was incorrect or missing was information about:

‘capacity’: a notation to identify whether Macquarie was acting as principal or agent;

‘origin’: a notation to identify the person on whose instructions Macquarie was acting; and

‘intermediary’: the AFSL number of an intermediary using Macquarie’s automated order processing system.

The MDP emphasised that the provision of accurate regulatory data

enhances market transparency and ensures an orderly market. The

provision of incorrect or missing regulatory data to market operators

impedes informed regulatory decision-making by market operators and by

ASIC.

The MDP found that while Macquarie intended to comply with the market integrity rules, there were weaknesses in the configuration and integration of Macquarie’s systems, its processes for on-boarding new clients and its control framework.

The MDP considers Macquarie’s conduct to be negligent, having regard

to Macquarie’s poor design and implementation of updates to key systems,

the high number of orders and trade reports containing incorrect or

missing data, the multiple categories of incorrect or missing data and

the length of time the problems persisted without detection by

Macquarie.

Given Macquarie’s scale, market share and high market flows, the MDP

considers that market participants such as Macquarie have greater

potential and capacity to undermine market integrity. A market

participant such as this should carry a greater responsibility to

properly manage the risks that flow from their conduct. If that risk is

poorly managed, the financial consequences to the market participant

should be commensurately greater.

The MDP noted that, once Macquarie became aware of the scale of the

issues, which it reported to ASIC, it undertook a comprehensive review

to identify the causes, and promptly implemented remedial measures.

Five global investment banks are facing a cartel class action lawsuit after a suit was filed at the Federal Court yesterday, via InvestorDaily.

Maurice

Blackburn Lawyers, who is also taking on AMP in a class action, have

launched the suit against UBS, Barclays, Citibank, Royal Bank of

Scotland and JP Morgan, claiming the banks colluded to rig foreign

exchange rates.

The suit alleges that between January 2008 and 15

October 2013, traders in chat rooms bearing names such as ‘The Cartel’

and ‘The Mafia’ communicated directly with each other to coordinate the

manipulation of FX benchmark rates.

“The chat rooms included

those named ‘The Cartel’, ‘The Mafia’, ‘One Team’, ‘One Dream’, ‘The

Players’, ‘The Three Musketeers’, ‘A Co-Operative’, ‘The A-Team’, ‘The

Sterling Lads’, ‘The Essex Express’ and ‘The Three Way Banana Split’,”

according to Maurice Blackburn’s statement of claim.

It is

alleged that the actions resulted in the pricing of ‘spreads’ and the

triggering of client stop loss orders and limit orders.

“Sharing

with each, alternatively one or more, of the other respondents, and/or

one or more of the other cartel participants, information in relation to

trade in FX Instruments with respect to one or more of the affected

currencies, including in relation to trade volumes and/or trade

strategy,” said the statement of claim.

The alleged conduct has

been the subject of extensive regulatory and private enforcement action

worldwide including settlements in the US and Canada resulting in the

payment of US$2.3 billion and CA$107 million respectively.

Some

of the allegedly affected currencies include the Australia, Canadian,

New Zealand and US dollar as well as the Russian ruble, Indian rupee,

the Euro and the British pound.

Maurice Blackburns principal

lawyer Kimi Nishimura said that the cartel behaviour could have affected

a number of Australian business and investors.

“Australian

businesses and investors – particularly medium to large importers,

exporters, institutional investors and businesses with operations

overseas – have been affected by the distortion of the FX market by

these banks.

“Such cartel behaviour cheats Australian businesses

in circumstances where they may already have been vulnerable to currency

fluctuations,” she said.

The class action will be represented by

lead plaintiff J.Wisbey and Associates, a medical equipment importer,

but is open to any customers that brought or sold currency during the

period where total value of transactions exceeded over $500,000.

Spokespeople for the banks involved did not issue a statement at time of writing.

I discuss the markets with Tony Locantro from Alto Capital, and get his take on which sectors might be of interest at the moment.

Bitcoin gets his thumbs down!

Please note that I have no financial relationship with Tony, I was simply interested in his perspective, and that this does not constitute financial advice.

Economist John Adams explores the post election environment in a discussion with Martin North, including the various strategies which are now in train to entice home buyers back into the market – the ponzi scheme continues…. the debt mounts.