Any measures in the federal budget aimed at housing affordability will have little impact on getting more people owning their own homes, according to latest budget monitor report from Deloitte Access Economics.

The concept of home and all that it means will come into focus at the federal budget next week with treasurer Scott Morrison indicating he will take action to increase home ownership.

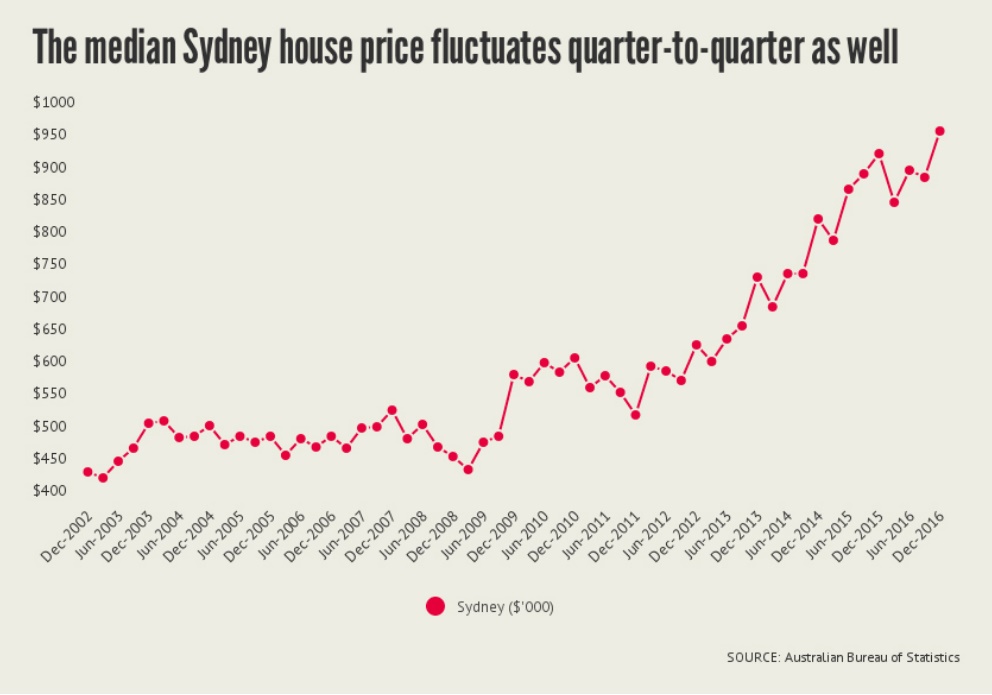

The key questions are why housing has become so expensive and what can be done to get young people back into the market, especially in Sydney and Melbourne where prices have skyrocketed.

Nationally, house prices have risen 12.9% over the last year, with hot spot Sydney jumping almost 20%, according to the latest numbers.

Deloitte Access Economics blames record low interest rates.

“Affordability is through the floor because interest rates are through the floor,” according to the budget monitor report, led by respected budget forecaster Chris Richardson.

Deloitte Access Economics says politicians are increasingly pretending “they” can do something about it.

“Housing affordability is stunningly important … today’s housing prices are dangerously dumb, especially so in Sydney,” says Deloitte Access Economics.

Among the measures the federal government could announce in the 2017 budget are cutting the capital gains tax discount and supporting capital raising for social housing.

“But the likely impact of any of these on affordability would require a microscope to observe,” says Deloitte.

“Yes, there’s good policy there and much that we’d support,” says Deloitte.

“But affordability is rotten because interest rates have never been lower.”

Deloitte says each percentage point increase in interest rates would strip some 7% off average housing prices.

Here’s how mortgage rates have fallen over the last three decades:

Source: Deloitte Access Economics

“If politicians, state and federal, are leaving punters with the impression that they can solve housing affordability, then they’re leading us down the garden path,” says the budget monitor report.

“And that’s unfortunate, because the electorate is already incredibly disappointed in the ability of politicians to deliver anything.”

Shane Oliver, head of investment strategy and chief economist at AMP Capital, notes that the government is now playing down what it can deliver on housing affordability.

“Maybe a few fiddles to encourage downsizing but since the big issue is supply and that is a state issue there is not really much it can do,” he says.

The federal government may be poised to unveil a special savings account and tax breaks for first home buyers in next week’s budget, despite government ministers refusing to confirm leaked reports in the media at the weekend.

With the housing affordability crisis close to the top of voter concerns, the federal Treasurer last week appeared to change focus from the housing sector to infrastructure, but those hoping to get into the housing market will be encouraged to hear the issue may be tackled, if in limited form only.

Reports suggested that Treasurer Scott Morrison’s upcoming budget would feature a provision allowing aspiring first home buyers to salary sacrifice in order to raise their needed deposits.

If that is true, it will be a case of back to the future, as a similar measure was introduced during Kevin Rudd’s first turn as prime minister before being scrapped by the Abbott government.

While Resources Minister Matt Canavan would not deal in specifics during a Sky News interview on Sunday, he stressed that home ownership would be a key theme of the upcoming budget.

“We are focused on making sure Australians can afford a home,” he said. “It is a fundamental principal.”

Under the Labor scheme, First Home Saver Accounts saw the government make co-contributions of up to $1020 (or 17 per cent) on the first $6000 that account holders deposited each year.

While there were tax concessions associated with the accounts, there were also restrictions around access to the funds, including that they were only to be used towards payment for first homes.

That scheme proved to be something of a disappointment. While Labor treasurer Wayne Swan predicted as many as 750,000 accounts would be established, only 46,000 had been opened when his successor, Abbott-era treasurer Joe Hockey, wound it up six years later in 2014.

And there was no shortage of critics, including the consumer group CHOICE, which complained in a submission to Treasury that it provided disproportionate assistance to high-income earners while doing little to help those who genuinely needed it.

“We are unaware of any evidence to suggest that sufficient savings are more difficult to achieve for higher-income earners,” CHOICE noted sarcastically.

Another criticism came from Treasury itself, which warned that the scheme as initially conceived would be complex to administer while not benefitting those on low incomes.

If the Turnbull government is indeed planning to revive home-saver accounts or something similar, the one near-certainty is that government contributions and associated tax breaks will need to be far more substantial if they are to have a positive impact than under Labor, when house prices were substantially less.

Despite First Home Saver Accounts being in effect for six years, Labor frontbencher Mark Butler insisted on Sunday that they had not had time to work – and, if something similar were to be re-introduced, it wouldn’t do much good anyway.

“The critical message is this,” he told the ABC’s Insiders, “you cannot deal with housing affordability in Australia without dealing with negative gearing.”

Greens senator Sarah Hanson-Young also rejected the notion that salary sacrificing would have a major effect.

“We have to bring the pressure down, not just give people more money to go straight into the hands of property investors.”

There’s been quite a bit of speculation over whether Australia has a property market bubble – where house prices are over-inflated compared to a benchmark – and when it might burst. According to housing experts, there’s at least four scenarios where this could happen.

Australia could see a property bubble burst due to:

Lending tightening, interest rate hikes and mortgage stress

Underemployment and unemployment creating a slow deflation

Government intervention failure and market repair

Global crisis

These four scenarios focus on different tension points in Australia’s and the global economy. One scenario focuses on the balance of actions between regulators like APRA and the Reserve Bank, combined with household mortgage stress. Another envisions the affect that unemployment might have in certain areas.

Some of the factors we may see play out, such as the federal and state government trying to intervene to “fix” problems in the market, as happens in one scenario. But other factors may be out of the government’s control, for example, where a global crisis pushes up risk premiums.

All of these scenarios highlight just how complicated and interrelated the steps that lead to a property bubble burst could be.

Lending tightening, interest rate hikes and mortgage stress

Associate Professor Harry Scheule, UTS Business School

Following increases in interest rates in the US and Europe, as those markets recover, the Australian dollar begins to decline – forcing the Reserve Bank of Australia (RBA) to increase interest rates.

Higher interest rates lead to higher monthly repayments, as most of Australia’s home loans are adjustable. Interest only loans are the most exposed. Higher interest rates also lead to more mortgage delinquencies.

The banks tighten bank lending standards in response to the increase in delinquencies. This further constrains interest-only borrowers seeking to refinance after the end of the interest-only terms. This means more mortgage stress, as many had expected to roll over the interest-only period indefinitely, but now they are forced to make principal repayments next to interest payments.

The cycle between delinquencies and tightening bank lending standards continues and as a result there’s a noticeable drop in loan supply and a fall in house prices.

Underemployment and unemployment create a slow deflation

Danika Wright, Lecturer in Finance, University of Sydney

Unemployment and underemployment – workers who want to work more but can’t – increase. As the apartment development boom dies down, and without a mining boom to replace it, construction industry workers are at high risk.

Households with a lot of mortgage debt are forced to limit their spending, particularly on discretionary items. This in turn affects companies that employ retail workers, reducing hours and employment.

Employment opportunities are a major component of house price amenity, in part because demand for housing is pushed higher by inbound work-related migration. So, as there are less jobs nearby, the amenity value of some areas decreases.

The amount of people at risk of defaulting on their mortgage increases in areas where there is a loss of employment or reduced income. In 2008, arguably the last time Sydney house prices went through a correction, the incidence of mortgage defaults and property price declines was geographically localised.

Borrowers who have the least amount of equity in their homes (typically the least wealthy, younger and newer entrants to housing market) are the hardest hit by falling property values. They are more likely to end up “underwater” – that is, owing more than the property is now worth – and face the prospect of a distressed sale. This in turn contributes to the downward spiral in house prices.

Australia has tighter lending criteria than regulators enforced before the global financial crisis in the United States. But concerns by regulators, including APRA, over current lending practices and potentially fraudulent activities raise questions over the real quality of mortgages and the ability of borrowers to repay them.

Government intervention failure and market repair

Professors of Economics, Jason Potts and Sinclair Davidson, RMIT

A combination of low interest rates and low growth in new housing stock drive up Australian housing prices, a situation compounded by poor policy choices by state and federal governments and high demand from foreign residential property investors.

As a result housing is misallocated in the Australian market, across demographic and especially age groups. This produces demographic pressures, as millennials delay leaving home, delay starting families. This leads to political pressure on governments – increases the urge to intervene.

The federal government intervenes, blaming the secondary drivers (particularly the non-voting group: foreign investors). They increase restrictions on foreign investment in residential housing stock.

The federal government also lobbies APRA to increase rules on financial products, while promoting a scheme to subsidise and promote first home ownership.

Because none of these previous measures from the federal government affect the primary drivers of the misallocation of housing, domestic interest rates don’t change, and state governments do not act to release new stock. As a result housing prices continue to grow.

Increasingly alarmed that house prices continue to rise, the federal government starts to panic, threatening ever further regulation and starts to blame the financial system. This triggers the RBA to finally act, raising interest rates.

As interest rates rise, this causes mortgage stress, resulting in default among investors with high amounts of debt, pushing these properties onto the market. These distressed sales finally cause prices to fall.

Global crisis

Timo Henckel, Research Associate, Centre for Applied Macroeconomic Analysis, ANU

International crisis (whether it be political, military, economic) leads to an increase in global risk premiums.

Borrowing costs for Australian banks rise because of this and supply of global capital falls, pushing up mortgage rates in Australia.

The most vulnerable mortgagees can no longer afford their mortgages and are forced to sell their homes.

House prices fall which, coupled with rising interest rates, adds further distress to households’ balance sheets, leading to more selling of houses and so on.

Authors: Jenni Henderson, Editor, Business and Economy, The Conversation; Wes Mountain, Deputy Multimedia Editor, The Conversation

Interviewed: Danika Wright, Lecturer in Finance, University of Sydney; Harry Scheule, Associate Professor, Finance, UTS Business School, University of Technology Sydney; Jason Potts, Professor of Economics, RMIT University; Sinclair Davidson, Professor of Institutional Economics, RMIT University; Timo Henckel, Lecturer, Research School of Economics, and Research Associate, Centre for Applied Macroeconomic Analysis, Australian National University.

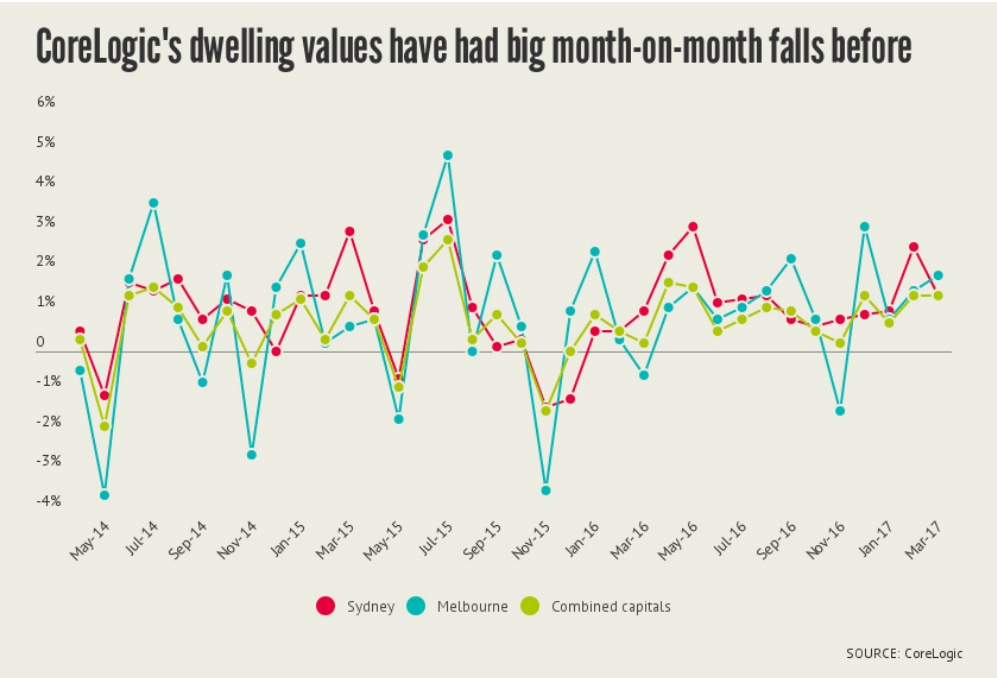

Experts have warned against predicting that property prices have peaked just yet.

A flurry of headlines this week generated by UBS analysts, Australian Financial Review columnists and others all warned that Sydney and possible Melbourne prices had peaked and we should brace for a correction.

Most were based on slower price growth in Sydney dwelling values and slight reductions in auction clearance rates compiled by CoreLogic, a property data firm.

However, CoreLogic director of research Tim Lawless cautioned against reading into the results (especially dwelling values, which are yet to be officially released for April) because April and May are generally weaker periods.

“Potentially there is some seasonality creeping into these numbers and that’s one of the reasons why I would probably suggest caution calling the peak right now before we see a few more months and see if the trend actually develops,” Mr Lawless told The New Daily.

“When we look at, say, a year ago or any sort of seasonality in the marketplace, yeah, we do generally see some easing in our reading around April and May.”

A further complication is that CoreLogic adjusted how it calculated dwelling values in May 2016 to account for seasonality. The result, according to Mr Lawless, is that “technically speaking, there are some challenges and complexities making a year-to-year comparison”, although he said the adjustments were “quite minor” and values could still be compared.

The change sparked a scandal last year, with the Reserve Bank ditching the company as its preferred data source after claiming it had overstated dwelling values in April and May.

Despite this, CoreLogic remains the most widely cited property data source because it reports dwelling values daily. But the most authoritative is the Australian Bureau Statistics, which has measured similar quarter-on-quarter falls in the past, especially between the December and June quarters. And yet, the trend has been ever upwards.

IFM chief economist Dr Alex Joiner agreed we shouldn’t jump to conclusions based on the latest statistics.

“I wouldn’t suggest that anyone looks at any month-to-month data in Australia and makes firm conclusions from it,” Dr Joiner told The New Daily.

“People might want to rush to call the top, but the trends are for gradually decelerating growth, and I think that’s about right.”

But if this is not the peak, the market is “very much approaching it” because the Reserve Bank and the banks are likely to lift interest rates even as wage growth stays low, Dr Joiner said.

“When that actually decelerates price growth, whether it’s this month or later in the year, I don’t know. But we’re certainly eeking out the very last stages of price growth in the property market.”

CoreLogic has revealed the property market has been largely flat during the month of April, ahead of the release of its end-of-month numbers on Monday.

CoreLogic’s hedonic home value index for Australia’s top five property markets held virtually steady in the first 27 days of the month, indicating that the current cycle could be moving through its peak.

Sydney prices recorded a “subtle” decline, according to CoreLogic, a dramatic though welcome turnaround from the blistering 18.8 per cent increase recorded in March. The five-city aggregate also recorded an exceptionally strong result in March, rising 12.9 per cent despite a 4.7 per cent decline in Perth prices.

Leeanne Pilkington, deputy president of the Real Estate Institute of New South Wales, says the April decline in Sydney prices was only very slight, and will vary from suburb to suburb.

“None of my agents are telling me they’re worried about prices going down,” she said.

However, Pilkington said her agents are saying there a lower numbers at open houses, which means there could be less competition in the market between buyers.

“We’ve seen that [trend] with the lower clearance rate last week,” she said. Pilkington said clearance rates above 80 per cent were not sustainable, and that a modest decline in clearance rates would actually be desirable.

“We really want some stability in the market,” she said.

Pilkington said April was a holiday month, containing both Easter and ANZAC day, so the numbers for the month may not reflect the true state of the market. Auction clearance rates over the weekend will provide clearer guidance, she said.

Tim Lawless, head of research Asia Pacific with CoreLogic, attributes the flat overall result to recent regulatory changes which have led to higher mortgage rates and weaker investment demand, causing a “dampening” effect on the property market.

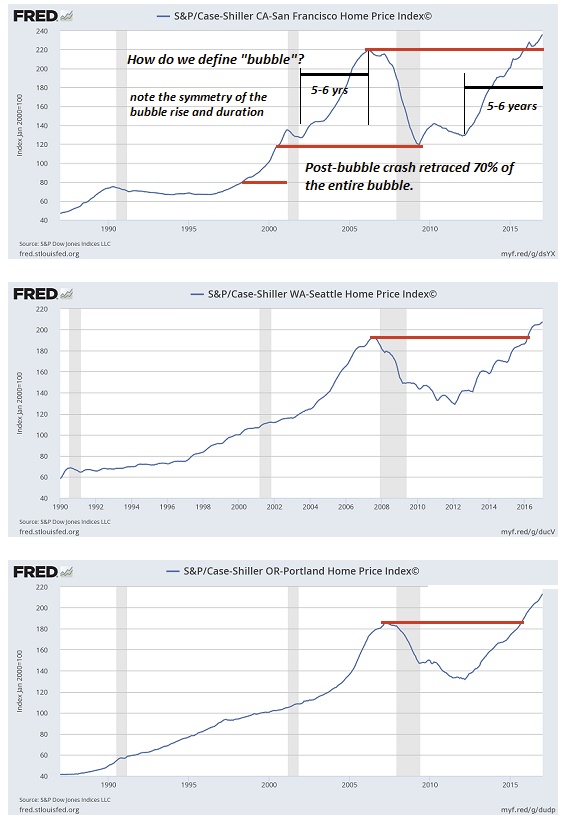

If you need some evidence that the echo-bubble in housing is global, take a look at this chart of Sweden’s housing bubble.

A funny thing often occurs after a mania-fueled asset bubble pops: an echo-bubble inflates a few years later, as monetary authorities and all the institutions that depend on rising asset valuations go all-in to reflate the crushed asset class.

Take a quick look at the Case-Shiller Home Price Index charts for San Francisco, Seattle and Portland, OR. Each now exceeds its previous Housing Bubble #1 peak:

Is an asset bubble merely in the eye of the beholder? This is what the multitudes of monetary authorities (central banks, realty industry analysts, etc.) are claiming: there’s no bubble here, just a “normal market” in action.

This self-serving justification–a bubble isn’t a bubble because we need soaring asset prices–ignores the tell-tale characteristics of bubbles. Even a cursory glance at these charts reveals various characteristics of bubbles: a steep, sustained lift-off, a defined peak, a sharp decline that retraces much or all of the bubble’s rise, and a symmetrical duration of the time needed to inflate and deflate the bubble extremes.

It seems housing bubbles take about 5 to 6 years to reach their bubble peaks, and about half that time to retrace much or all of the gains.

Bubbles have a habit of overshooting on the downside when they finally burst. The Federal Reserve acted quickly in 2009-10 to re-inflate the housing bubble by lowering interest rates to near-zero and buying over $1 trillion of mortgage-backed securities.

When bubbles are followed by echo-bubbles, the bursting of the second bubble tends to signal the end of the speculative cycle in that asset class. There is no fundamental reason why housing could not round-trip to levels below the 2011 post-bubble #1 trough.

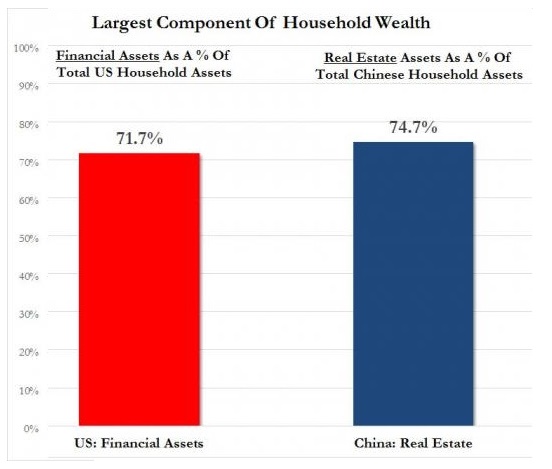

Consider the fundamentals of China’s remarkable housing bubble. The consensus view is: sure, China’s housing prices could fall modestly, but since Chinese households buy homes with cash or large down payments, this decline won’t trigger a banking crisis like America’s housing bubble did in 2008.

The problem isn’t a banking crisis; it’s a loss of household wealth, the reversal of the wealth effect and the decimation of local government budgets and the construction sector.

China is uniquely dependent on housing and real estate development. This makes it uniquely vulnerable to any slowdown in construction and sales of new housing.

About 15% of China’s GDP is housing-related. This is extraordinarily high. In the 2003-08 housing bubble, housing’s share of U.S. GDP barely cracked 5%.

Of even greater concern, local governments in China depend on land development sales for roughly 2/3 of their revenues. (These are not fee simple sales of land, but the sale of leasehold rights, as all land in China is owned by the state.)

There is no substitute source of revenue waiting in the wings should land sales and housing development grind to a halt. Local governments will lose a majority of their operating revenues, and there is no other source they can tap to replace this lost revenue.

Since China authorized private ownership of housing in the late 1990s, homeowners in China have only experienced rising prices and thus rising household wealth. The end of that “rising tide raises all ships” gravy train will dramatically alter China’s household wealth and local government income.If you need some evidence that the echo-bubble in housing is global, take a look at this chart of Sweden’s housing bubble. Oops, did I say bubble? I meant “normal market in action.”

Who is prepared for the inevitable bursting of the echo bubble in housing?Certainly not those who cling to the fantasy that there is no bubble in housing.

Australian house price growth will slow to 7 per cent in 2017 before it collapses to between zero and 3 per cent in 2018, predicts UBS.

In a new housing outlook report, UBS said it is “calling the top” for Australian residential housing activity despite a surprise rebound in February approvals to 228,000.

While the “historical trigger” for a housing downturn is missing (namely, RBA interest rate hikes), mortgage rates are rising and home buyer sentiment is at a near record low, said UBS.

“Hence, we are ‘calling the top’, but stick to our forecasts for commencements to ‘correct but not collapse’ to 200,000 in 2017 and 180,000 in 2018,” said the report.

House prices are rising four times faster than incomes, noted UBS, which is unsustainable and suggests that growth has peaked.

“We see a moderation to [approximately] 7 per cent in 2017 and 0-3 per cent in 2018, amid record supply and poor affordability, with the new buyer mortgage repayment share of income spiking to a decade high,” said UBS.

The report also pointed to the March 2017 Rider Levett Bucknall residential crane count, which has more than tripled since 2013 to a record 548, but is now flat year-on-year.

Housing affordability has gone from “bad to even worse”, said UBS, with the house price to income ratio soaring to a record 6.5.

“With record low rates, repayments haven’t yet reached historical tipping points where prices fell, but would if mortgage rates rose by only [approximately] 100 basis points,” said the report.

The gross rental yield for two-bedroom unit has fallen to a record-low of less than 4 per cent, said UBS, which is now below mortgage rates of 4.25-4.50 per cent.

UBS also pointed to Australia’s household debt to GDP ratio of 123 per cent, which is one of the highest in the world.

Although dwelling valuations in Australia are 5-15% above historical averages, the risk of a catastrophic collapse in the housing market is low, argues Merlon Capital Partners, a Sydney-based boutique fund manager.

In its latest paper, entitled Some Thoughts on Australian House Prices, Merlon acknowledged that the nation is currently at a cyclical high point, with “house prices, housing finance activity and building approvals … all at historically elevated levels.” At the same time, interest rates are at record lows and have begun to hike, particularly for investors.

“We think the housing market is 5-15% overvalued relative to ‘mid-cycle’ levels. Contrary to recent commentary, we do not find this over-valuation to be concentrated in the Sydney market,” said Hamish Carlisle, analyst at Merlon Capital Partners.

Carlisle doesn’t find the modest system-wide overvaluation to be particularly surprising at the current point in the economic cycle, and notes that the nation is a long way off from what are considered to be “mid-cycle” interest rates. “Rising interest rates – as we are currently experiencing – are likely to be a precursor to a turn in the cycle so it is likely we will enter into a phase of more subdued house price inflation.”

Favourable tax treatment of housing, coupled with historically low interest rates and favourable fundamentals (i.e. income and rental growth), mean that it’s highly unlikely that house prices will retrace to “mid-cycle” levels in the foreseeable future.

Carlisle further asserts that regulator concerns about house prices are “overblown”. Growing regulatory restrictions, which force banks to ration lending, particularly to property investors, are probably unnecessary and will achieve little other than improving the short-term profitability of banks via higher interest rates for borrowers.

“As with all our investing, we work on the basis that, over time, interest rates will revert back to long term levels as will aggregate housing valuation metrics. Against this, we think aggregate rents and household incomes will continue to grow which will cushion the overall impact on dwelling prices and that the exposure of the household sector to higher interest rates means that the time frame over which interest rates will rise could be quite protracted. As such, we think the risk of a catastrophic collapse in the housing market is low,” he said.

The Reserve Bank of Australia under governor Philip Lowe has backed the concerns of regulators about bank lending standards, seizing on the rising number of households who are a month away from missing a mortgage payment in his first major review of the financial system.

Dr Lowe has zeroed in on a rise in the percentage of households who have a buffer of less than one month’s mortgage payments, in contrast with the last review conducted under his predecessor which saw risks abating.

The RBA has put the spotlight firmly bank on the banks in its twice yearly report by noting “one-third of borrowers have either no accrued buffer or a buffer of less than one month’s payments”.

This latest study of the financial architecture adds more detail to the worrying picture emerging about the unbalanced housing market. It follows concerns from the Australian Securities and Investments Commission and the Australian Prudential Regulation Authority about a build up of risks and warnings from credit ratings agencies that the property market could face an orderly unwinding of prices.

The RBA also noted that these risks would have consequences for the banks themselves, pointing to the prospect of additional losses on mortgage portfolios for banks with exposures to the mining sector.

Significant pivot

The focus on households and the state of their balance sheets marks a significant pivot from the previous Financial Stability Review released one month before Dr Lowe was made governor and found that risks to households had lessened.

Founder of boutique research house Digital Finance Analytics Martin North said it was about time the Reserve Bank woke up to the risks posed by higher levels of household debt and stagnant incomes.

“This situation hasn’t fundamentally worsened in six months so it stands to reason what has changed is the RBA’s perception of the world,” Mr North said.

Statistics from Digital Finance Analytics show the percentage of Australian households that are cutting back expenditure, dipping into savings or using credit facilities to meet mortgage payments has risen to 22 per cent following a series of out-of-cycle rate rises from the banks.

Data published by the big four banks supports the warning from the RBA with anywhere between 20 and 40 per cent of big four bank mortgage holders just a misstep away from missing a mortgage payment.

ANZ and NAB, which measure the percentage of mortgage holders who do not have buffers of one month or more, count 61 per cent and 27.7 per cent of their customers respectively in the non-buffer bracket.

Commonwealth Bank and Westpac, which use a less stringent buffer measure to include any additional repayment and factor in offset accounts, put 23 per cent and 28 per cent of customers in the RBA’s danger zone.

Annual result data from the banks shows that the percentage of customers who do not have sufficient buffers have worsened by between 2 per cent and 3 per cent over the last 12 months alone.

The worsening position of households has been attributed to rising healthcare and energy costs combined with out-of-cycle rate rises and flat incomes.

Mr North noted that much of the data on households was predicated on the HILDA data which had a lag of several years.

“We have always had households that struggle to make mortgage payments,” Mr North said. “So the intriguing question for me is why have they woken up now? It could be that the governor has taken a different view on household debt.”

Deloitte Access Economics’ quarterly business outlook, released today, predicts the official cash rate of 1.5 per cent will climb slowly in 2018 and 2019 to reach 3 per cent in the early 2020s.

The Reserve Bank was well aware “interest rates are now a massively more potent weapon for slowing the Australian economy than they’ve ever been before”, the forecaster said.

It noted Australian families have overtaken the Danish in recent months to become the world’s second most indebted households after the Swiss, relative to income – a consequence of “dangerously dumb” house prices.

Director Chris Richardson told Fairfax Media a crisis could be averted if, as he predicted, interest rates rose slowly and steadily. But cheap credit and high leverage still posed risks.

“In global terms our housing prices are asking for trouble,” Mr Richardson said, arguing many workers have found their homes make more money each day than they do. “That’s kind of God’s way of saying: this thing’s gonna blow.”

Sydneysiders were particularly vulnerable, Deloitte found, having benefited enormously from low interest rates but now witnessing “silly prices” that continued to grow – a “rather worrying development” in Deloitte’s eyes.

“The seeds of future slowdown are already well and truly sown. The better that NSW looks now, the greater the troubles that this state is storing up for the future,” the outlook warned.

“The joy of rising wealth eventually gives way to the pain of servicing gargantuan mortgages. Interest rates are beginning to rise around the world and although official interest rates in Australia may not follow suit until 2018, that augurs badly for the disposable incomes of Sydneysiders.”

Martin North, principal of Digital Finance Analytics, expressed concern Australia could be heading for a version of the US sub-prime mortgage crisis that preceded the Global Financial Crisis.

The parallels involve spiralling household debt, stalled incomes, rising levels of mortgage stress and interest rates that are on the way up.

Mr North’s modelling shows 669,000 families (or 22 per cent of borrowing households) are in mortgage stress. That would rise to 1 million households, or one third of borrowers, if interest rates rose by 3 percentage points.

But the main factors in Mr North’s reckoning are the static nature of wages and the rising tide of under-employment.

“This falling real income scenario is the thing that people haven’t got their heads around,” he told Fairfax Media.

“Unless we see incomes rising ahead of inflation and under-utilisation dropping, any increase in interest rates is going to have a severe impact on [people’s] wallets and therefore in discretionary spending and therefore on growth.

“I have a feeling we are meandering our way, perhaps a little bit blindly, into a rather similar scenario to the US.”

Mr North said mortgage stress was not only an issue for battlers and people on the urban fringe, but increasingly affected more affluent, highly leveraged households.

He dismissed the possible solutions put forth by Treasurer Scott Morrison as “political theatre” and invoked former prime minister Paul Keating by arguing Australia may be heading for “the correction we have to have”.

“I’m not sure that there are other levers that are available,” he said.

Source: Deloitte Access Economics

Source: Deloitte Access Economics