From The Real Estate Conversation.

The Reserve Bank has left interest rates at historic lows as economic conditions improve, but the property industry says other measures are required to improve housing affordability.

The Reserve Bank of Australia left interest rates on hold at its first meeting of 2017, with rates held at a record low of 1.50 per cent.

Governor Philip Lowe noted in his statement that growth in China was stronger in the second half of 2016, that global business and consumer confidence is improving, and that global inflation is rising. He also said recent rises in commodity prices are increasing Australia’s national income.

Lowe said the RBA expects Australian economic growth in the final quarter of 2016 to firm, and re-affirmed the RBA is forecasting growth to pick up to “around 3% over the next couple years”. Lowe said Australian inflation is heading back towards the target range.

In his November 2016 statement, Lowe said cutting rates further may not be in the “public interest” if it further increased household debt.

Real Estate Institute of New South Wales President John Cunningham said the central bank’s decision was no surprise, but said he expects housing affordability to be “hotly debated” this year.

“An emphasis will again be placed on first homebuyers and there will be much debate this year on ways to improve their plight,” he said.

“A review of stamp duty is urgently required and should focus on first homebuyers and older Australians,” said Cunningham.

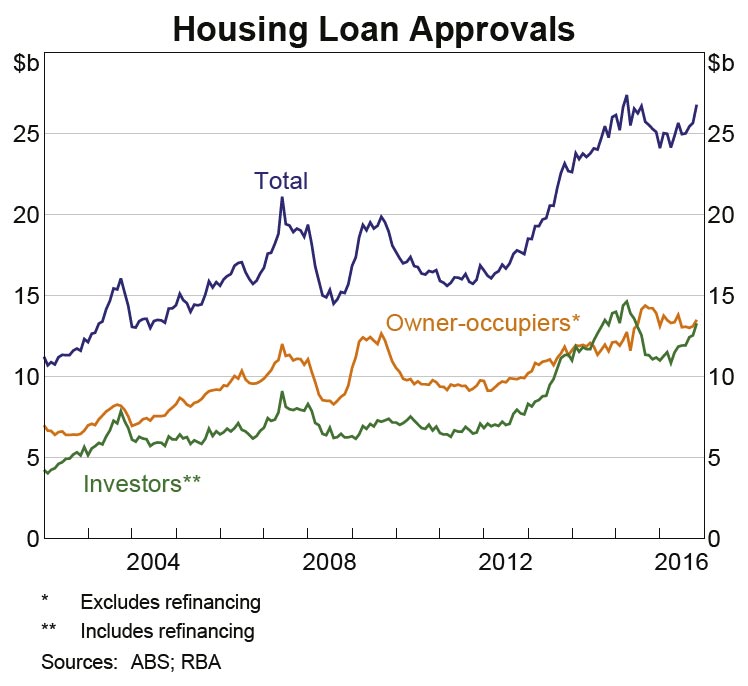

The RBA cut interest rates twice in 2016, first in May and then in August. However, banks are independently increasing interest rates for investors as increased global economic uncertainty raises their borrowing costs.

Laing+Simmons managing director and REINSW president-elect Leanne Pilkington echoed Cunningham’s sentiment, saying rate cuts are not the answer to improving housing affordability. Further rate cuts are not required in the current housing cycle, she said.

“Obtaining housing finance at attractive terms is already possible for those with the means,” said Pilkington.

“It’s those without the means – stuck in the rental cycle or unable to accumulate a suitable deposit – that face the greatest challenge in the market,” Pilkington said.

“Further rate cuts are not a solution to the problem. Between government and the industry, we need to table some alternative solutions to help people buy their first home,” she said.

“From a housing industry perspective,” said Pilkington, “rates are already low and have been for some time, so that piece of the affordability puzzle is in place.”

Like Cunningham, Pilkington believes changes to stamp duty are necessary to address housing affordability problems. “It’s through other avenues like stamp duty reform that improvements in affordability need to be addressed,” she said.

Pilkington also said making downsizing more viable for older Australians, introducing a Government-backed savings scheme to help people save for a deposit, and minimising the cost of mortgage insurance could all alleviate housing affordability problems in Australia.

The Property Council of Australia welcomed the statement by Lowe on interest rates, saying it was a sober assessment of housing markets.

The governor’s statement said “conditions in the housing market vary considerably around the country”.

Ken Morrison, chief executive of the Property Council of Australia, said the statement confirms the current situation of “prudent lending practices and the best environment for renters in a generation with consistent low rental growth.”

“The deterioration in housing affordability is a serious problem in a number of our major cities, but is not an Australia-wide problem,” said Morrison.

1300 HomeLoan managing director John Kolenda said the RBA will remain on the sidelines until uncertainty about the economic impact of US president Trump becomes clearer.

“The RBA will stay on the sidelines and assess the impact on the global economy although our domestic economy appears stable with no need to adjust interest rates,” said Kolenda.

Kolenda said while the RBA’s cash rate is unlikely to change in the short term, confusion could arise from varying mortgage rates, and reinforced his recommendation to use a mortgage broker.

Source: Roy Morgan Research Single Source: Mortgage holders 12 months to October 2015 (n=11,249); 12 months to October 2016 (n=10,655).

Source: Roy Morgan Research Single Source: Mortgage holders 12 months to October 2015 (n=11,249); 12 months to October 2016 (n=10,655). Source: Roy Morgan Research Single Source; Mortgage holders 12 months to October 2016 (n=10,655).

Source: Roy Morgan Research Single Source; Mortgage holders 12 months to October 2016 (n=10,655). The Treasurer’s media release said

The Treasurer’s media release said