A really mixed bag of news this week, with stronger business and employment data, lower mortgage defaults and yet weak wage growth, and more evidence of the pressure on households. We pick over the coals and try to make sense of what’s going on.

Welcome to the Property Imperative Weekly to 18 November 2017. Watch the video or read the transcript.

Welcome to the Property Imperative Weekly to 18 November 2017. Watch the video or read the transcript.

We start with some good news.

The latest National Australia Business (NAB) survey — a composite indicator that measures trading activity, profitability and employment — surged by a massive 7 points to +21, leaving it at the highest level since the survey began in 1997. On this measure, Australian businesses have not had it so good in at least two decades. There were enormous increases recorded in trading and profitability, suggesting that demand was rampant during October. However, beware, this included a massive unexplained jump in manufacturing and the survey’s lead indicators softened over the month, which, along with an unchanged reading on business confidence, raises questions as to whether the bounce in the conditions index can be sustained.

Deputy Governor Guy Debelle spoke at the UBS Australasia Conference on “Business Investment in Australia“. He argued that investment has been strong over the last decade, thanks to the mining sector. This is now easing back, and the question is will the non-mining sector start firing or not? Even if it does, they have huge boots to fill!

Luci Ellis RBA Assistant Governor (Economic) delivered the Stan Kelly Lecture on “Where is the Growth Going to Come From?“. An excellent question given the fading mining boom, and geared up households! But we really got few answers. Australia’s population is growing faster than in almost any other OECD economy. That has remained true over the past couple of years. The rate of natural increase is higher than many other countries, but most of the difference is the large contribution from immigration. Of course, just adding more people and growing the economy to keep pace wouldn’t boost our living standards. Next, employment participation has been rising recently. The increase has been concentrated amongst women and older workers and is linked with the increase in health and education employment. Finally, productivity can improve, especially if innovation can be leveraged, although she noted the rate of technology adoption has slowed down since the turn of the century. We wonder if this has something to do with the sluggish and underpowered NBN rollout currently underway.

The monthly trend unemployment rate remained at 5.5 per cent in October 2017, according to figures released by the Australian Bureau of Statistics. While the trend is down, it was not as strong as some analysts were expecting. The seasonally adjusted unemployment rate decreased by 0.1 percentage points to 5.4 per cent and the labour force participation rate decreased to 65.1 per cent.

The ABS released their analysis of individual state accounts to Jun 2017. This includes an estimate of average gross household disposable income per capita. The variations across states are significant and interesting. Of note is the astronomical value, and trajectory of individuals in the ACT, at more than $90,000. We saw a decline in gross incomes in WA (one reason why mortgage defaults are rising there) at around $50,000. NSW was also around $50,000 while VIC was around $45,000 and TAS was $40,000.

Wages rose 0.5 per cent in the September quarter 2017 and 2.0 per cent over the year, according to the ABS. This was below consensus expectation, and continues the slow grind in household income, for many falling below the costs of living. Those in the public sector continue to do better than those in the private sector. In original terms, wage growth to the September quarter 2017 ranged from 1.2 per cent for the Mining industry to 2.7 per cent for Health Care and Arts and recreation services. Western Australia recorded the lowest growth through the year of 1.3 per cent and Victoria, Queensland and Tasmania the highest of 2.2 per cent.

The legislation to tighten some aspects of investment property, and levy a charge on vacant foreign owned property has been passed in the Senate. The legislation prevents property investors from claiming travel expenses when travelling between properties, as well as tightening depreciation on plant and equipment tax deductions. Foreign owners will be charged a fee if they leave their properties vacant for at least six months in a 12-month period, in an attempt to release more property to ease supply. The latest Census showed that there are 200,000 more vacant homes across Australia than there were ten years ago.

Turning to the mortgage industry, Fitch Ratings says Australia’s RBMS mortgage arrears fell to 1.02% in 3Q17, a 15bp decrease from the previous quarter; consistent with the nine-year long seasonal trend where 30+ days arrears have eased in the third quarter. They say the curing of third-quarter arrears was helped by borrowers using tax return receipts to make repayments. The 30+ days arrears were 4bp lower than in 3Q16, reflecting Australia’s improved economic environment and lower standard variable interest rates for owner-occupied lending. They said the gap between investor lending and owner-occupied rates has widened, as banks respond to regulatory investment and interest-only limits on new loan origination. Historically, investors paid a 25bp-30bp premium over owner-occupied loans, but this widened to 60bp in September 2017.

S&P Global Ratings said RMBS Mortgage arrears fell to 1.08% in September across Australian down from 1.10% in August 2017. They say mortgage arrears rose in both the Northern Territory and the ACT during September but fell elsewhere. The ACT mortgage arrears it is only at a low 0.64%, compared with Western Australia who has the highest arrears of 2.21%. However, while outstanding loan repayments on 30-to-60-day arrears also declined in most states between January and September, 90-day+ arrears rose in Western Australia and Queensland. This is the same as we saw recently in the bank reporting season. S&P expects arrears to rise over the coming months, as they “traditionally start to increase in November and continue through to March.”

There was more evidence of poor mortgage lending practice this week, following the recent UBS “Liar Loans” research study. A liar loan is a loan that is approved on the basis of unverified and possibly false information about income, assets or capacity to repay. This is important because mortgage delinquency and default may rise due to excessive risk taking in mortgage lending combined with deteriorating economic conditions; or due to falling income and rising unemployment during a housing downturn.

Connective remained brokers of their obligations, and pointed to findings from the 2016 Veda Cybercrime and Fraud Report, which recorded a 27 per cent year-on-year increase in falsifying personal information. “Falsified documentation — particularly documents that verify a customer’s income — is the most common type of fraud that a mortgage broker is likely to encounter,” the aggregator said. Back in June, Equifax informed brokers at a Pepper Money roadshow that 13 per cent of frauds reported were targeting home loans and there has been a 25 per cent year-on-year increase in frauds originating from the broker channel.

In the same vein, NAB has said it has commenced a remediation program for some of its customers, after a review identified their home loan may not have been established in accordance with NAB’s policies. NAB identified around 2,300 home loans since 2013 that may have been submitted without accurate customer information and/or documentation, or correct information in relation to NAB’s Introducer Program. As a result of NAB’s review, 20 bankers in New South Wales and Victoria had their employments terminated, or are no longer employed by NAB, and an additional 32 bankers had consequences applied including the reduction of remuneration. NAB has commenced writing to these customers – many of whom live overseas – asking them to participate in a detailed review of their loan, which may include verification of documents submitted at the time of their home loan application. Affected customers may be offered compensation as appropriate.

More evidence of the risks in the system came when The Reserve Bank in New Zealand said that Westpac New Zealand has had its minimum regulatory capital requirements increased after it failed to comply with regulatory obligations relating to its status as an internal models bank. Internal models banks are accredited by the Reserve Bank to use approved risk models to calculate how much regulatory capital they need to hold. Westpac used a number of models that had not been approved by the Reserve Bank, and materially failed to meet requirements around model governance, processes and documentation.

Still talking of risks, there was an interesting paper from the Federal Reserve Bank of Cleveland “Three Myths about Peer-to-Peer Loans” which suggested these platforms, which have experienced phenomenal growth in the past decade, resemble predatory loans in terms of the segment of the consumer market they serve and their impact on consumers’ finances and have a negative effect on individual borrowers’ financial stability. This is of course what triggered the 2007 financial crisis. There is no specific regulation in the US on the borrower side. Given that P2P lenders are not regulated or supervised for antipredatory laws, lawmakers and regulators may need to revisit their position on online lending marketplaces.

We published two research reports this week. First our Quiet Revolution Banking Channel and Innovation Report, which is available for free download. And second the impact of rising interest rates on households.

It seems that eventually mortgage rates will rise in Australia, as global forces exert external pressure on the RBA, and as the RBA tries to normalise rates (at say 2% higher than today). Timing is, of course, not certain. But it is worth considering the potential impact. While our mortgage stress analysis takes a cash flow view of household finances, our modelling can look at the problem another way. One algorithm we have developed is a rate sensitivity calculation, which takes a household’s mortgage outstanding, at current rates, and increments the interest rate to the point where household affordability “breaks”. We use data from our household survey to drive the analysis.

So we start with the average across the country. We find that around 10% of households would run into affordability issues with less a 0.5% hike in mortgage rates, and around another 8% would be hit if rates rose 0.5%, and a larger number would be added to the “in pain” pile, giving us a total of around 25% of households across the country in difficulty if rates went 1% higher. [Note that the calculation does not phase the rate increases in]. Around 40% of households would be fine even if rates when more than 7% higher. At a state level we found that around 40% of households in NSW would have a problem, compared with 27% in VIC and 24% in WA. We can also take the analysis further, to a regional view across the states. This reveals that the worst impacted areas would be, in order, Greater Sydney, Central Coast, Curtain and Greater Melbourne. These are all areas where home prices relative to income are significantly extended, thus households are highly leveraged.

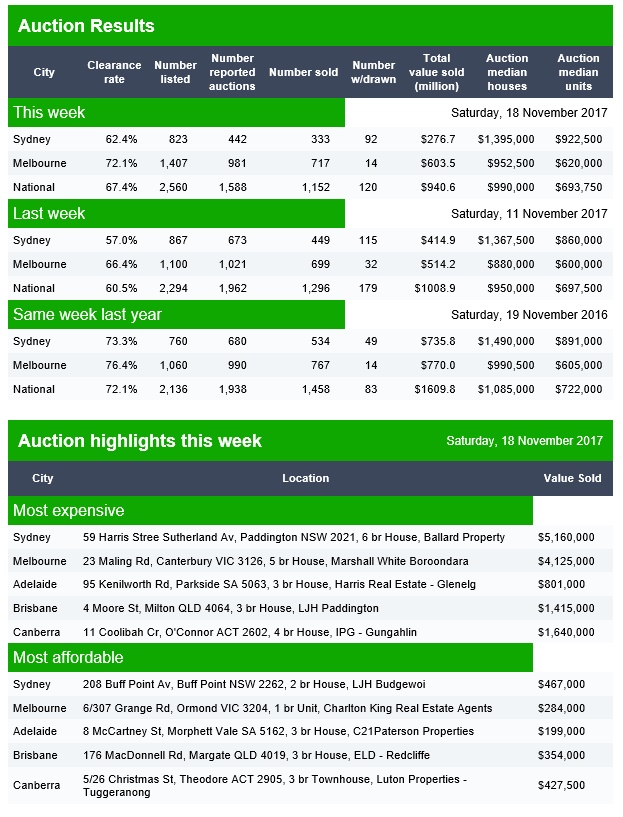

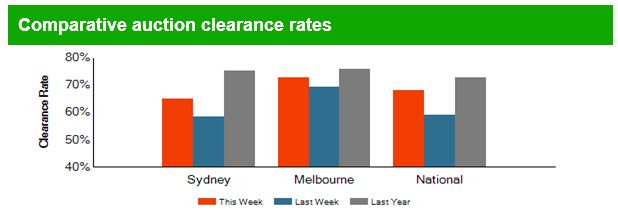

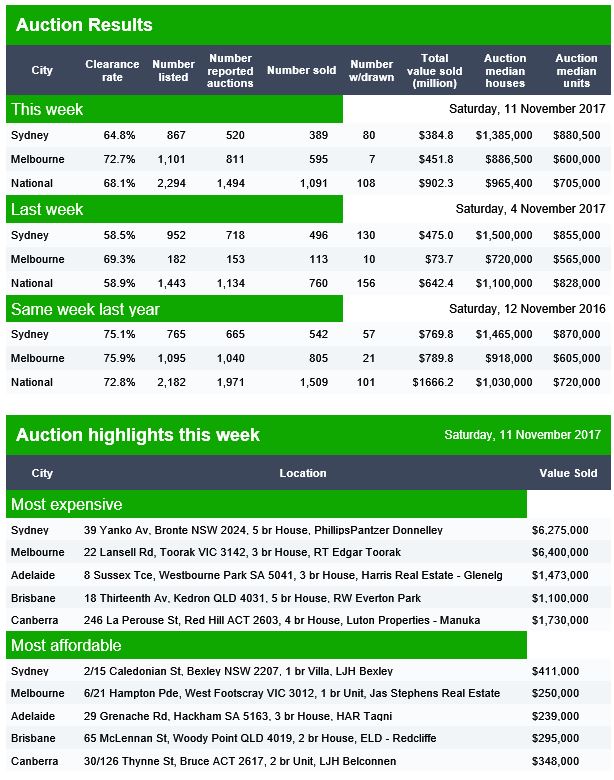

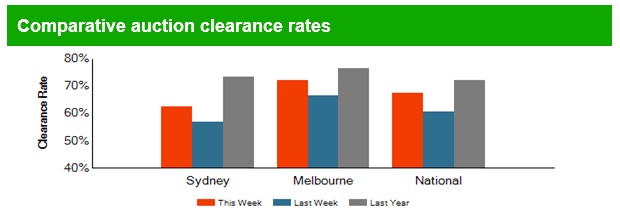

CoreLogic said Mortgage clearance rates have continued to track below 70 per cent since June the year; this is a considerably softer trend than what was seen over the same period last year when clearance rates were tracking around the mid 70 per cent range for most of the second half 2016. Results across each of the individual markets were varied this week, with Canberra recording the highest preliminary auction clearance rate of 72.9 per cent, while in Brisbane only 45.7 per cent of auctions cleared.

So to, two important reports.

According to the eighth edition of the Credit Suisse Research Institute’s Global Wealth Report, in the year to mid-2017, total global wealth rose at a rate of 6.4%, the fastest pace since 2012 and reached USD 280 trillion. But wealth distribution has become more uneven. This reflected widespread gains in equity markets matched by similar rises in non-financial assets (home prices), which moved above the pre-crisis year 2007’s level. Household wealth in Australia grew at an average annual growth rate of 12%, with about half the rise due to exchange-rate appreciation against the US dollar. Australia’s wealth per adult in 2017 is USD 402,600, the second highest in the world after Switzerland.

However, the composition of household wealth in Australia is heavily skewed towards non-financial assets, which average USD 303,200, and form 60% of gross assets. The high level of real assets partly reflects a large endowment of land and natural resources relative to population, but also results from high property prices in the largest cities.

Finally, Industry Super Australia, published an excellent discussion paper on “Assisting Housing Affordability” which endeavours to identify the underlying causes of affordability issues, and considers some useful policy responses in the current and historical context. They rightly consider both supply and demand related issues.

They call out specifically the impact of incoming migration, especially around university suburbs in the major centres as one major factor.

More broadly, they articulate the problem facing many, in that access to affordable housing – a basic need – is now more difficult than ever and the issue is affecting household spending decisions:

- Key workers like police officers, teachers and nurses can’t afford to live near the communities they serve.

- Children are staying at home for longer, marrying later and taking longer to save for a home deposit.

- Many older Australians are locked into big houses that no longer suit their needs while a greater number of near retirees are renting or paying off a mortgage.

- Commuters spend too much time on congested roads and trains which are now the norm in certain Australian cities.

- More Australians are renting.

The report is worth reading because it knits together the complex web of issues, and confirms the complexity which is housing affordability, and that there are no simple single point solutions.

And that’s the point. Sure, employment looks strong, but the nature of that employment is favouring lower wage occupations. Business confidence is strong, because business profits are up, but this is not translating into higher wages. As a result, wealth distribution is becoming more skewed, as home prices and stock prices rise. But the risks remain. Property is overvalued, and we lack joined up thinking to address the fundamental structural issues which exist. So meantime we muddle on, hoping that wage growth will start to rise before home prices fall too far and mortgage rates rise. Don’t look down, we are walking a tightrope!

So that’s the Property Imperative weekly to 18th November 2017. If you found this useful, do leave a comment below, subscribe to receive future updates, and check back next time. Thanks for watching.

Brisbane cleared 33% of 136 listed, Adelaide 62% of 98 listed and Canberra 69% of 96 listed.

Brisbane cleared 33% of 136 listed, Adelaide 62% of 98 listed and Canberra 69% of 96 listed.