The frenzied growth of the east coast market has prompted a series of warnings pointing to the contradiction between inflated house prices and the stagnant or declining incomes of working people, amid a slump across manufacturing and other industries.

Last week, Moody’s cautioned that Australia’s housing market was among four in the world most susceptible to a crash in the event of an economic shock or a renewed downturn. The international ratings agency drew attention to the mountain of debt upon which the property bubble has been built, stating: “Australian households stand out for lower financial buffers and higher leverage.”

Moody’s drew a parallel between debt-to-liquid asset ratios in Australia, and in Ireland before the collapse of the property market in 2007. It commented: “[I]n the event of a negative income shock, the scope for Australian households to draw down parts of their financial assets to maintain debt service and overall spending is more limited than elsewhere.”

Deloitte Access Economics likewise pointed to the buildup of debt this week, noting that household debt to income ratios are the second highest in the world after Sweden. National household debt currently stands at 185 percent of annual disposable income, up from around 70 percent in the early 1990s.

Deloitte has estimated that house prices are around 30 percent overvalued compared to national income, the highest margin in over three decades. The firm’s director, Chris Richardson warned that in “global terms our housing prices are asking for trouble.”

In comments to the National Press Club last week, Richardson warned of the vast implications of any slowdown of the Chinese economy for the Australian housing market and financial system. He predicted that a sharp crisis in China could result in the collapse of house prices by around 9 percent, as part of a broader downturn that could destroy almost $1 trillion of national wealth.

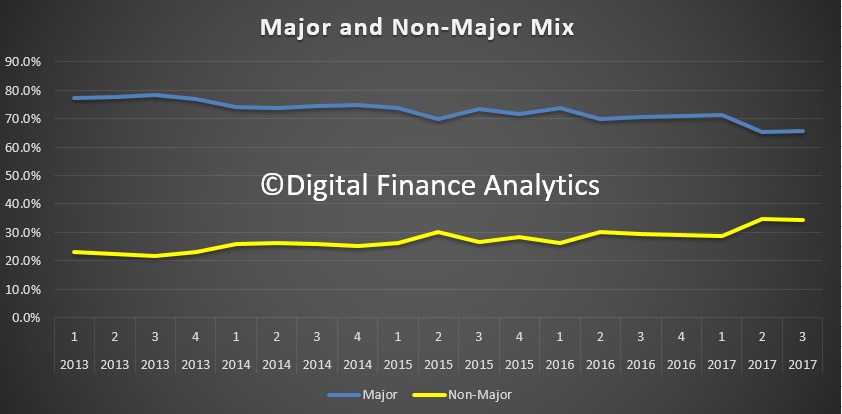

Martin North, of Digital Finance Analytics, drew parallels with the US subprime mortgage crisis that played a key role in precipitating the global financial crisis of 2007–08. He listed declining incomes, rapidly rising household debt and a growth in mortgage stress as features in common.

North told Fairfax Media: “This falling real income scenario is the thing that people haven’t got their heads around.” National wage growth across the private sector was just 1.8 percent last year, the lowest level since records began in 1969. Modelling by North has indicated that 669,000 families, or 22 percent of borrowing households, are already in mortgage stress.

Other reports have pointed to the mounting social crisis caused by the ongoing rise in house prices, prompting warnings of a rise in mortgage arrears and defaults.

In its Financial Stability Review released last week, the Reserve Bank reported that around one third of mortgaged households have not built up any substantial repayment buffer, or are a month or less ahead of mortgage repayments. In other words, they are vulnerable to economic fluctuations and any change in their circumstances.

An ALI Group survey last month showed that 41 percent of homeowners feared that they would be unable to keep up with mortgage repayments if they lost their job.

This finding tallied with figures late last year from financial management software company Moneysoft, which found that more than 25 percent of non-investor home loans were “unhealthy.” Loans were deemed to be in bad health if they had grown by at least 5 percent over the course of the loan. Another 25 percent were termed “neutral,” meaning that they had neither grown nor substantially fallen.

The precarious situation of many has contributed to a growth in delinquent housing loans. They rose from 1.15 percent of all housing loans last December, to 1.29 percent in January, according to Standard and Poor’s. In some states the figure is far higher, with Western Australia, which has been hit by the collapse of the mining boom, registering 2.33 percent.

These conditions have led to intensified calls for the Reserve Bank to raise its official interest rate from a historic low of 1.5 percent, and take other measures to rein in speculative loans, including interest-only loans that do not require the borrower to pay off any of the principal for fixed periods of up to seven years.

Minutes from the central bank’s April meeting stated that it “would consider further measures if needed,” but did not spell them out. Any rise in interest rates, however, could lead to a rapid fall in borrowing, along with a rise in mortgage defaults, potentially provoking a dramatic contraction of the entire market.

The soaring cost of housing, which has made it unaffordable for many young people, has intensified the crisis of the Liberal-National government of Malcolm Turnbull. Like its Labor Party predecessor, the government has maintained capital gains tax concessions, and other policies, such as negative tax gearing, which have provided a boon for property developers.

Amid reported divisions within the government, various proposals have been floated, including allowing first homebuyers to access their superannuation funds to purchase a house and making limited reductions in the 50 percent capital gains tax concessions.

The Labor Party has demagogically denounced negative gearing tax incentives for investors. Their posturing was punctured by reports this week that federal Labor politicians own some 72 investment properties in total. Their Liberal-National and Greens colleagues likewise have substantial material interests in the ongoing housing boom.

None of the measures being discussed by the government, or any section of the political establishment, will resolve the housing affordability crisis and the massive growth of property market speculation that has fuelled it.

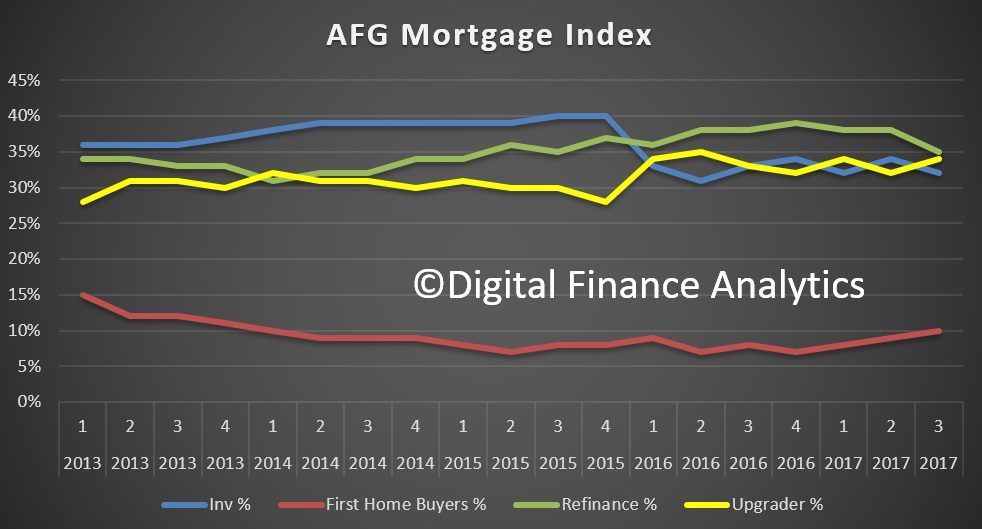

Loans to investors made up around 39 percent of all housing loans in January, with only 7 percent of loans for first homebuyers. The proportion of investors is higher in Sydney and Melbourne, the centres of the property boom.

According to the Australian Bureau of Statistics, investor loans grew by 27.5 percent on a seasonally adjusted basis, between January 2016 and 2017. The growth was well above the 10 percent annual limit placed on the banks by regulatory authorities.

The rise has coincided with an ongoing decline in productive investment. Corporate investment in new buildings, equipment and machinery fell in each quarter last year, with a decline of 2.1 percent in the December quarter alone.

As has happened around the world, the deepening crisis of global capitalism and the escalating slump in the real economy has seen the corporate elite turn to ever-more speculative financial operations. These do not produce real social wealth but inflate the value of existing assets, in this case, leading to a housing crisis for millions of working people.