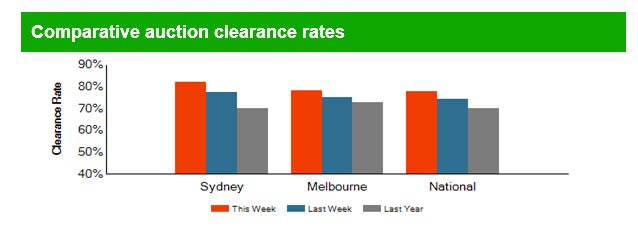

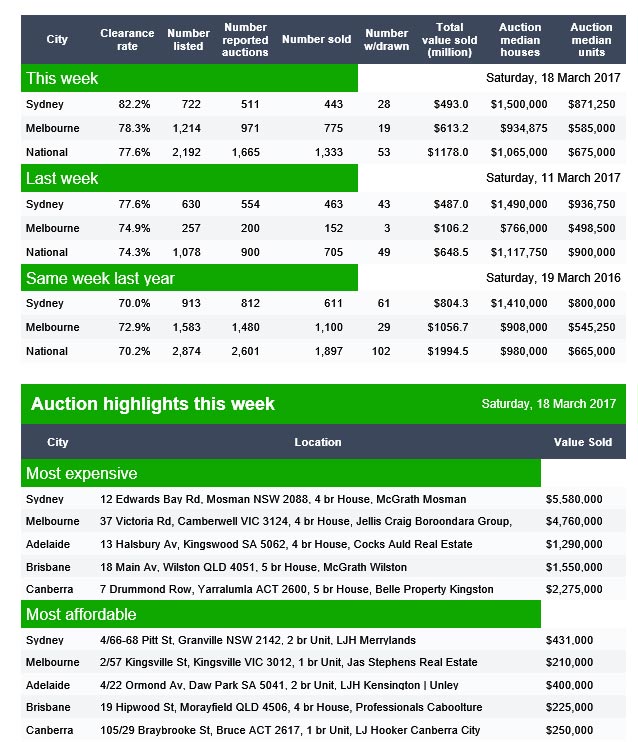

The preliminary results for today are in from Domain, and we see strong clearance rates in the main Sydney and Melbourne markets.

The national clearance rate was 77.6% compared with 74.3% last week, with 1,333 sold compared with 705 last week, and 1,897 last year. Sydney achieved 82.2% with 443 sales and Melbourne 775 compared with 152 last week (a holiday weekend). So high clearance rates, but on lower sales volumes.

Brisbane cleared 53% of 105 scheduled auctions, Adelaide 64% of 68 scheduled and Canberra 68% of 83 scheduled auctions.

The New South Wales government is considering increasing stamp duty paid by foreign investors to help first-home buyers get on the property ladder.

The news comes as figures reveal more than one in 10 residential properties sold in NSW are being snapped up by foreigners, with a third of them bought by Chinese nationals.

Data from the Office of State Revenue shows that in the three months from July to September 2016, foreign nationals accounted for 11 per cent — or 2995 — of residential property purchases in NSW compared with 7.51 per cent by first home buyers, according to NSW Labor.

Opposition leader Luke Foley is also pushing for the surcharge to be lifted from 4 per cent to 7 per cent for foreign investors on residential homes — to dampen the pressure they exert on housing prices.

“Evidence suggests a surcharge on foreign investors will take some pressure off house prices and go a way to levelling the playing field for first home buyers,” he said on Tuesday.

NSW Treasurer Dominic Perrottet was aware of the problem and would lift the surcharge in the June budget, according to News Corp.

Premier Gladys Berejiklian concedes more needs to be done to improve housing affordability in the state.

Doubts over what will help people into housing market

Deputy director of the Australia-China Relations Institute at the University of Technology, Professor James Laurenceson, has also questioned whether the move would improve affordability for Australians trying to get into the housing market.

“The housing prices particularly in Sydney are still going up and that gets at this point — even if the proportion of foreign buyers falls it doesn’t mean that house prices are going to fall,” he said.

He said it was simply not true that foreign buyers, particularly those from China, were squeezing Australians out of the market.

“Foreign Chinese buyers only account [for] 3.6 per cent of demand in New South Wales — a lot of that demand is for new apartments, new houses, not existing houses,” he said.

Professor Laurenceson said 96.4 per cent of buyers were local, so it “was a bit rough to say ‘Chinese buyers are squeezing out local buyers’.”

“Something that the Reserve Bank of Australia has long talked about is the fact that the types of properties foreign investors are buying are not the types of properties first home buyers are buying,” he said.

The Berejiklian Government has made improving housing affordability a priority, and has identified increasing housing supply as a key means to achieve it.

Professor Laurenceson said a Senate Inquiry last year found that foreign investors increased housing supply in Australia.

“It’s basic economics, if you expand supply it’s going to restrain housing price growth, it’s certainly not going to put upward pressure on it.

“There’s lots of reasons why housing prices are going up —but laying the blame at the feet of Chinese buyers when they only account for 3.6 per cent of total housing demand is clearly a misleading narrative.”

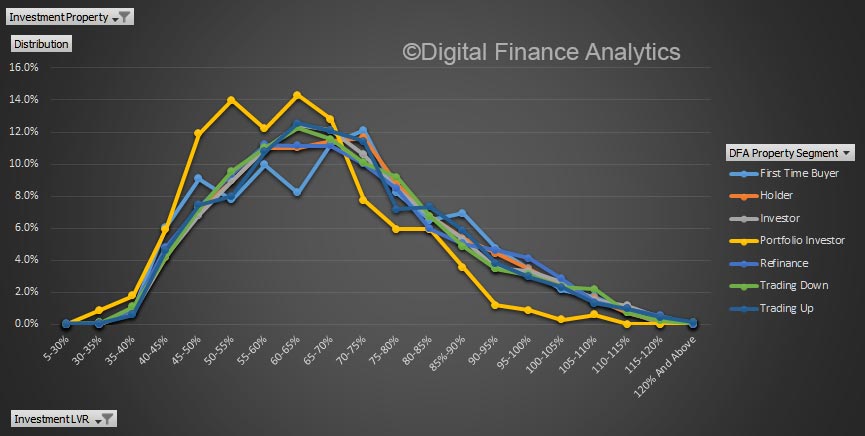

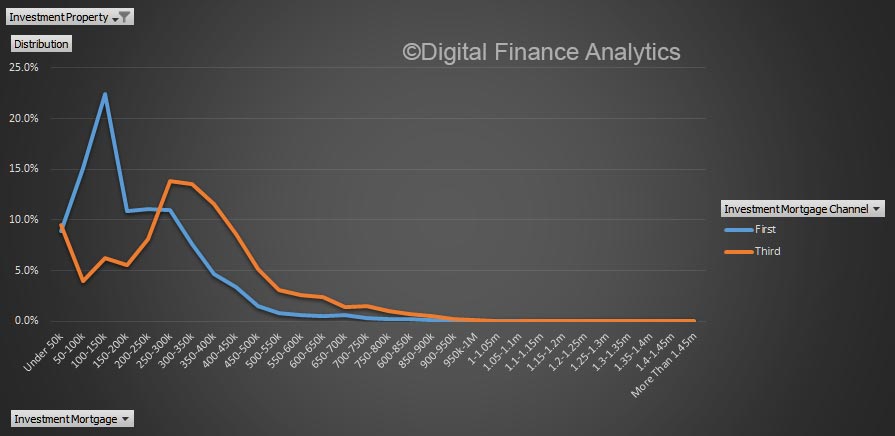

Using data from our household surveys, we can look at investor loans by our core master household segments. These segments allow us to explore some of the important differences across groups of borrowers. We believe granular analysis is required to see what is really going on.

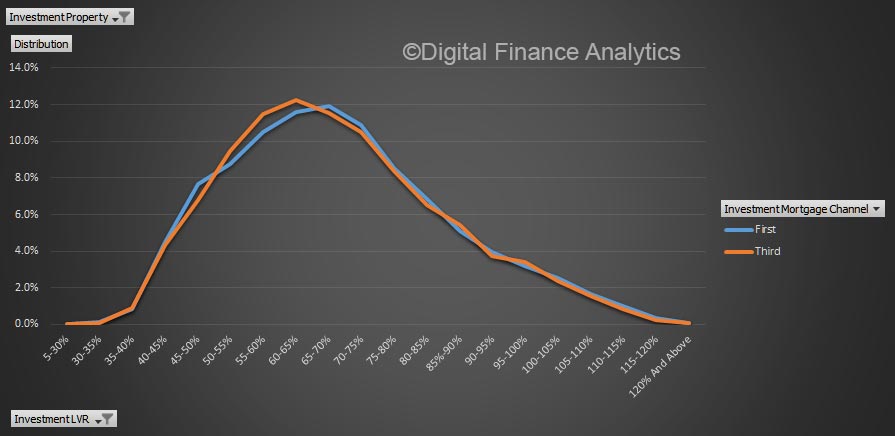

Today we look at the distribution of these segments by loan to value (LVR) and amount borrowed and also compare the footprint of loans via brokers, and by loan type.

Looking at LVR first, there is a consistent peak in the 60-70% LVR range, with portfolio investors (those with multiple investment properties) below the trend above 70%.

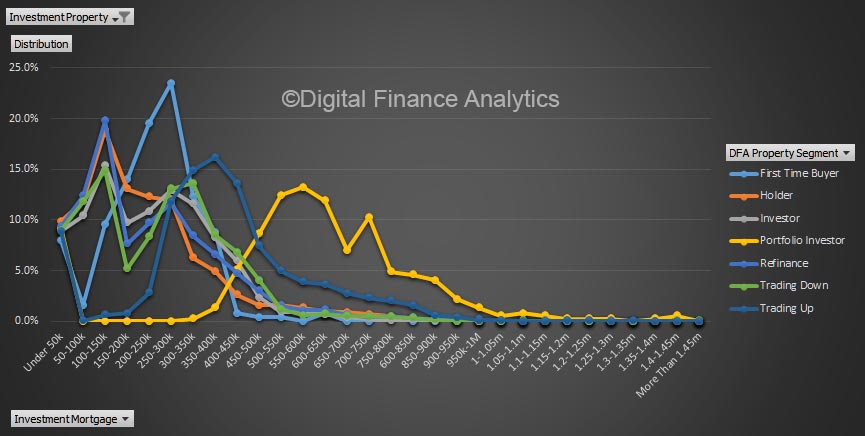

However, the plot of loan values shows that portfolio investors are on average borrowing much more, thanks to the multiple leverage across properties. A small number of portfolios are north of $1.4 million.

Investors who borrow with the help of a mortgage broker, on average is more likely to get a larger loan.

But there is very little difference in the relative LVR by channel.

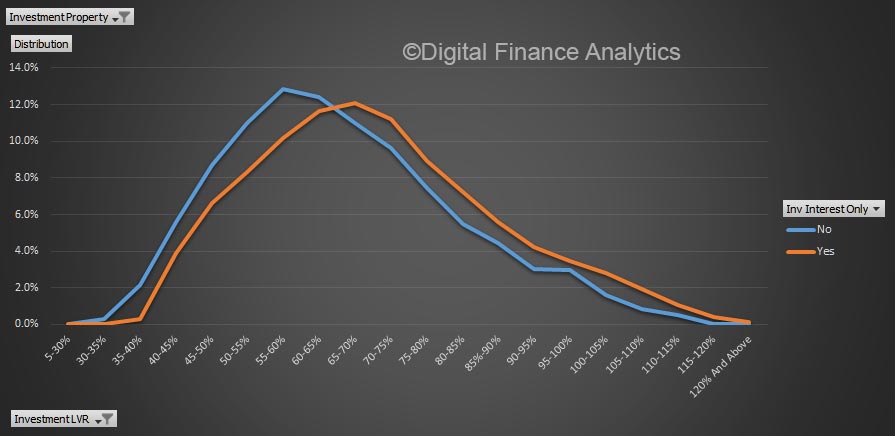

On the other hand, interest only loans will tend to be at a higher LVR.

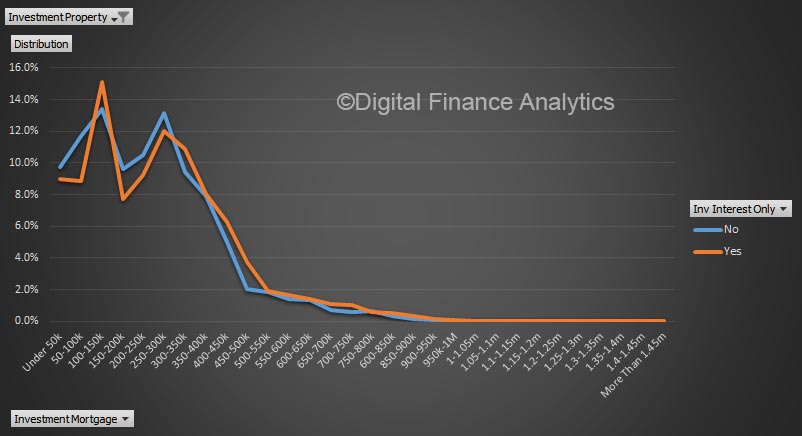

The average balance of interest only loans is also higher, especially in the $400-600k value range.

Microprudential analysis reveals interesting insights! The loan type and segment are better indicators of relative risk than LVR or origination channel.

This week 1,402 auctions were held across the combined capital cities, significantly lower than the 2,907 held last week and lower than one year ago (1,488). Four out of the eight states and territories have a public holiday this coming Monday which has been a key factor in the fall in auction volumes. The combined capital city clearance rate rose this week, up from 74.6 per cent last week to 80.8 per cent this week. The two largest auction markets, Melbourne and Sydney, saw their preliminary clearance rates rise, with Sydney at 83.1 per cent and Melbourne at 84.3 per cent, while the highest clearance rate was in Adelaide where 87.0 per cent of auctions cleared over the weekend. One year ago, the combined capital city clearance rate was a lower 64.9 per cent.

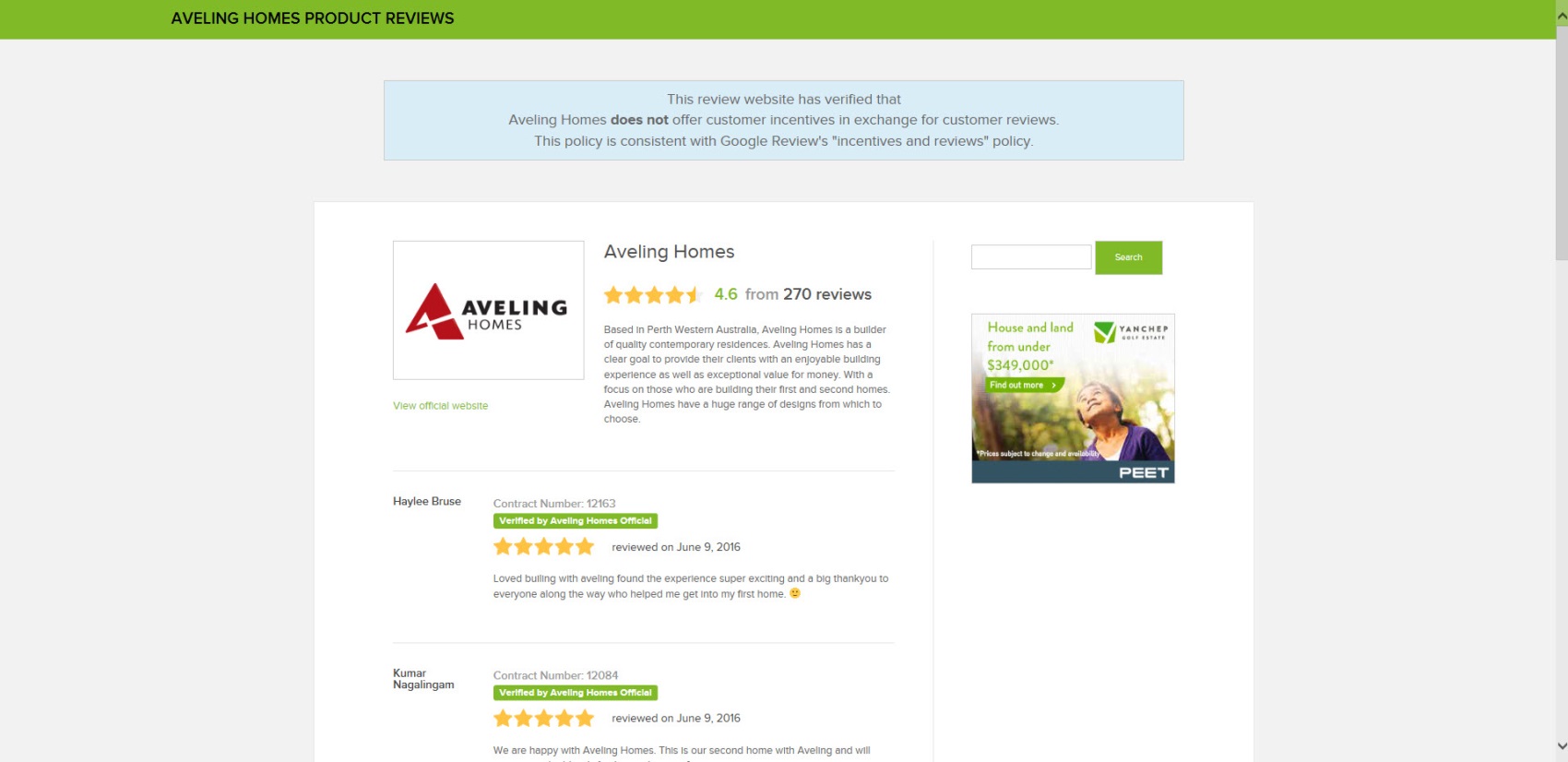

The Australian Competition and Consumer Commission says it has instituted proceedings in the Federal Court against Aveling Homes Pty Ltd (Aveling), a Perth-based home building company, for alleged misleading conduct and false or misleading representations.

The alleged conduct is in relation to review websites Aveling created for its businesses, Aveling Homes and the First Home Owner’s Centre.

The ACCC alleges that Aveling created review websites that represented they were independent of Aveling, and that the appearance, layout and features gave consumers the overall impression that they were affiliated with an independent third party consumer review website, Product Review, when this was not the case.

The ACCC also alleges that the review websites were deliberately managed by Aveling to ensure a favourable overall impression, by obscuring or removing unfavourable reviews.

“We believe the potential for harm from the conduct alleged in this case is significant, as buying or building a home is one of the biggest purchasing decisions for Australians,” ACCC Deputy Chair Dr Michael Schaper said.

“Online reviews are increasingly being relied on by consumers and they should be able to trust that those reviews are independent, unbiased and accurately reflect the range of consumer feedback received.”

The ACCC also alleges that Aveling’s marketing manager, Sean Quartermaine, was knowingly concerned in Aveling’s conduct.

The ACCC is seeking declarations, pecuniary penalties, injunctions, corrective notices, a compliance program, findings of fact and costs.

Background

Until 1 February 2017, Aveling also operated the brand ‘First Home Owners Centre’.

The ACCC’s allegations concern conduct and representations made on four Aveling websites:

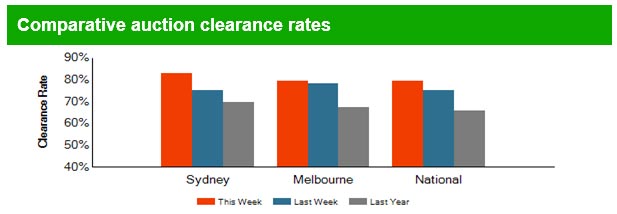

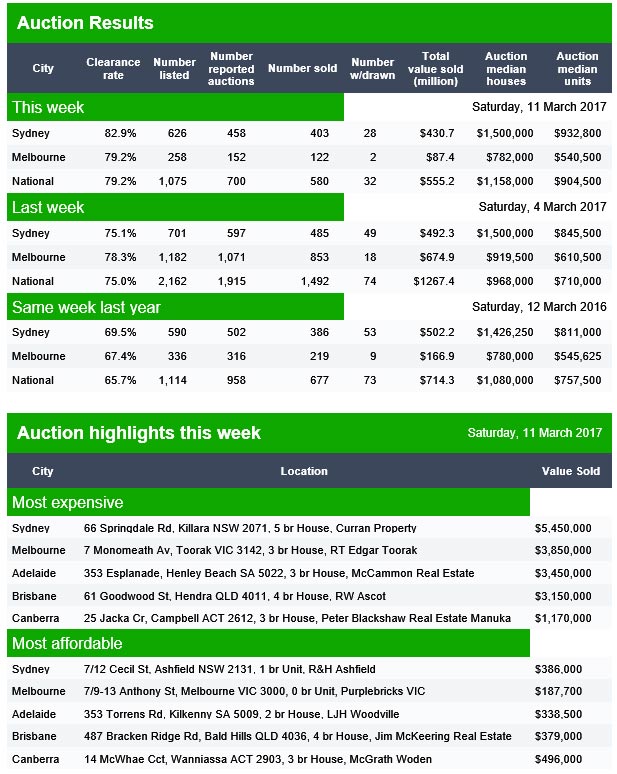

The preliminary auction clearance results from Domain, for today, on first blush looks strong, but below the surface, volumes were down.

Sydney clearance rates were at 82.9%, compared with 75.1% last week, and 69.5% a year ago. But the number of auctions were down, 458, compared with 597 last week and 502 this week last year.

In Melbourne (over a long weekend) clearances were 79.2%, compared with 78.3% last week and 67.4% this time last week. However, reported auctions were 152, compared with 1,071 last week and 316 last year.

Nationally, the clearance rate was 79.2%, compared with 75% last week and 65.7% last year. But reported auctions were just 700 compared with 1,915 last week and 958 last year.

Brisbane scheduled 113 auctions and achieved 52% clearance, Adelaide 56 scheduled auctions with a clearance of 66% and Canberra 22 auctions with 77% clearance.

So overall a mixed picture. Lets see if volume comes back next week, of whether this is a sign of some slowing in momentum.

Politicians and the powerful property lobby continue to argue that building more houses is the solution to Australia’s chronic affordability problems.

But a “supply-side solution” – as propounded by NSW Premier Gladys Berejiklian as well as Prime Minister Malcolm Turnbull and Treasurer Scott Morrison – will only work if affordability is just a supply-side problem. Evidence suggests this is not the case. In fact, our analysis shows that Australia is almost a world leader in rates of new housing production.

How Australia compares

One way to assess Australia’s supply performance is to compare it with other developed countries. The graph below compares the number of dwelling completions per 1,000 persons across 13 countries, for the years 2010 and 2015. On this measure, Australia’s new housing production is second only to South Korea’s.

Australia delivers two-thirds more homes per 1,000 persons than the US and four times more than the UK. When we measure supply as a proportion of existing stock, Australia again ranks second with a rate double that of the US.

OECD questionnaire on affordable and social housing; World Bank population growth and total population figures, Author provided

A slightly different approach takes into account population growth. This involves measuring dwelling completions per head of new population. Here Australia’s performance sits in the middle of the pack.

We are delivering just over 0.5 dwellings per head of new population compared to more than 2 in South Korea. This rate is, however, still ahead of the UK and comparable to the US. Again, that suggests inadequate supply is not the major cause of the affordability crisis.

OECD questionnaire on affordable and social housing, World Bank population growth and total population figures, Author provided

State comparisons of supply

At a national level, supply seems pretty healthy. But there are significant state variations. This might, on the surface, be used to explain different patterns of price growth.

The table below shows that New South Wales has produced fewer new homes per 1,000 people than Australia overall over a 30-year period. The difference was particularly marked between 2005 and 2015.

State comparisons of new housing supply.ABS building activity Australia cat. 8152; ABS Australian Demographic statistics Cat 3101, Author provided

However, higher supply output in the other states has certainly not created affordable markets. In NSW, the last two years have delivered significant supply growth yet prices have continued to rise just as fast. So why do prices rise with supply growth?

Demand drives supply

In a market-driven housing system, price stimulates new housing supply. In Australia new supply has responded relatively quickly to price rises (despite the continuous rhetoric from the property lobby about planning).

But there is always some lag due to the time it takes to secure necessary approvals and physically construct property. There is no such lag with demand meaning there is often a sustained mismatch between the two – positive or negative.

In a rising market, development becomes more profitable and land values rise, meaning greater returns for all concerned. Potential future capital gains stimulate investment activity. Price rises also allow owner-occupiers to trade up as the equity in their own dwelling increases.

In such circumstances, increased levels of housing supply do little to satiate demand created by population growth and the appetite of investors.

Western Australia has had an incredible level of housing completions over the last 30 years, as shown in the table, with 2014 and 2015 particularly strong. In the last 12 months, dwelling commencements have collapsed by more than 25%. Prices have been falling slowly for almost three years driven by the contraction in the resources sector and strong levels of new supply.

However, even under these conditions, WA housing affordability shows little sign of improving for those on low incomes. The market still cannot deliver housing for those at the bottom end of the market.

The housing market is simply unable to deliver housing that is affordable to those on lower (and, increasingly, moderate) incomes because there is a minimum cost of delivering housing that meets minimum community standards. This is made up of the land price, the physical construction costs of the dwelling, and the profit required for taking on the development risk.

This is why market intervention and subsidy are essential to deliver options for those on low incomes.

Targeted interventions are needed

Two strategies are needed to deliver affordable housing to the lower end of the market.

First, demand-side measures need to be better targeted to stimulate investment in new supply, particularly affordable rental housing, rather than simply fuelling demand.

Second, any government serious about improving affordability needs to put more resources into the community housing sector. This could be funded in two ways: partly by taxing the windfall gains from development and partly by reallocating existing demand-side subsidies.

The community housing sector can operate counter-cyclically. This means it can maintain housing supply even when house prices stagnate or fall – which is good for the economy.

Targeting supply to deliver housing for those on low incomes and reining in demand-side incentives that fuel prices will make some difference to affordability for those most affected.

There was some encouragement over the weekend. Scott Morrison discussed the rental market and social housing as part of the affordability solution. This was a welcome change from trotting out the tired old supply arguments and threatening to fuel demand through more home ownership incentives.

Let’s hope the treasurer follows through and delivers some much-needed “whole of housing market” thinking in the May budget.

Authors: Steven Rowley, Director, Australian Housing and Urban Research Institute, Curtin Research Centre, Curtin University; Nicole Gurran, Professor – Urban and Regional Planning, University of Sydney; Peter Phibbs, Chair of Urban Planning and Policy, University of Sydney

Auction results continue their strong run into March, with Sydney and Melbourne recording an 80% clearance rate over the first week of the month, according to CoreLogic.

After recording the strongest result since June 2015 last week, the preliminary clearance rate across the combined capital cities fell slightly this week, from 78.4 per cent to 77.8 per cent, based on preliminary results. The number of auctions held across the capitals this week was lower, with 2,714 held, compared to 3,301 over the previous week which was a record high for February. In comparison, over the corresponding week last year, both the combined capital city clearance rate and the number of auctions were lower, with 2,304 auctions held and 68.6 per cent reported as successful. Sydney saw the clearance rate remain above 80 per cent for the 4th week in a row, and Melbourne for the 2nd week in a row, while across the remaining cities; week-on-week results show a fall in clearance rates with the exception of Perth where results improved, and Tasmania, which remained unchanged over the week.

House prices will increase thanks to a Victorian government decision to scrap stamp duty on some properties, according to experts who warn the move would benefit owners – not first home buyers – if rolled out across the country.

Victorian Premier Daniel Andrews on Sunday announced first home buyers would be exempt from paying stamp duty on properties under $600,000.

Tax discounts will also be rolled out on new and existing homes worth between $600,000 and $750,000 from July 1 under the plan to tackle housing affordability.

It estimated the stamp duty exemptions would benefit 25,000 first home buyers, who would save up to $15,000 – or an average of $8000 – on new purchases.

The move comes as NSW Premier Gladys Berejiklian and the Turnbull government face calls to address skyrocketing house prices in Australia’s south-east.

Prices rose 18.4 per cent in Sydney and 13.1 per cent in Melbourne in the 12 months to February, according to CoreLogic data.

Changes benefit owners

Despite Mr Andrews saying the reforms would place “downward pressure on prices” by creating more housing stock, experts warned buyers should expect to pay more for a home following the changes.

Leading Australian economist Saul Eslake said the only benefit for new buyers was that it “may reshuffle the queue of would-be house buyers”.

“This decision would be welcomed by owners and vendors of existing properties. It will allow those who have properties for sale to sell them at higher prices than they would otherwise get,” he told The New Daily.

“It will do nothing to assist those who want to join them as owners of one property.”

The stamp duty cuts form part of a series of recent housing reforms in Victoria, with the government doubling the first home buyer’s grant in regional areas and making changes to planning laws in Melbourne’s outer suburbs.

Mr Eslake, who advocated replacing stamp duty with a broad-based land tax, warned other states against following Victoria’s lead on stamp duty.

“If it were adopted by other states, the result would be to enrich those who already own properties to the detriment of those who don’t,” he said.

Grattan Institute chief executive John Daley said the Andrews government’s changes may help new buyers in areas where they were competing with investors.

“If you take places where most of the buyers are investors or second home buyers, it will genuinely help first home buyers. It will push up the prices a little but not very much,” he said.

“However, for areas where most of the purchasers are first home buyers, such as the areas on the city fringes, essentially most of the benefit will be passed on to the sellers.

“This will be a huge windfall for the large development companies who do developments on the edge of our cities.”

As the NSW Government mull its own plans to tackle rising house prices, Mr Daley urged the Premier to prioritise changes to planning rules, particularly Sydney’s middle-ring suburbs, to boost housing supply.

“Everyone agrees that’s the right answer, as long as it’s in the suburb next to theirs,” he said.

“Any government that is going to be serious about this, needs to make the public and political case.”

On Sunday, NSW Premier Gladys Berejiklian, who has declared house prices a top priority, said the government was keeping its options open.

“We know in the past governments have had made decisions which unfortunately have had the opposite effect,” she said.

“We don’t want to be in that situation; we want to make sure every decision we take on this important issue has the desired effect.”

Last month, CoreLogic data showed median house prices had reached $970,00 in Sydney and $711,000 in Melbourne.

In our latest video blog we walk though some of the most important numbers in the mortgage and property market, including the latest findings from our household surveys.

Some of the questions we answer are:

How big is the mortgage market?

How many borrowing households are there?

What is the average mortgage size?

How many households are excluded from the market?

What will happen if mortgage rates rise by 3%?

Where is mortgage stress worst?

How does the Bank of Mum and Dad in Australia compare with the UK?