Australia is building an extraordinary number of high rise apartments right now. Everywhere you look, there seems to be a new development under construction, especially in Australia’s southeastern capitals.

And, going off recent building approvals data, it seems that there are a whole lot more coming.

Like a number of other commentators, Bill Evans, chief economist at Westpac, is uneasy about Australia’s high rise construction boom, stating in a research note released today that “huge uncertainty prevails in this market”.

The source of this uncertainty, says Evans, is the heavy involvement of Chinese buyers in the market, something that has helped propel the building boom in recent years along with the increased prevalence of housing investors.

“The number of high rise apartments currently under construction in March this year (ABS latest) has surged to 110,000 – including 44,000 in New South Wales; 34,000 in Victoria; and 23,000 in Queensland,” says Evans.

“However, a significant proportion of the buyers are offshore based, so called FIRB buyers,” he adds.

According to a recent survey conducted by ANZ in consultation with the Australian Property Council, foreign investors accounted for 23.9% of all property sales in Australia during the June quarter of 2016. The proportion of sales in Victoria and New South Wales were the highest in the country, accounting for 30.8% and 25.4% of all sales over the same period.

With so many apartments being sold to foreigners, many of them to Chinese, it is clear that much of the residential building boom, and beyond that the outlook for prices, is determinant on the continued involvement of foreign investors.

According to Evans, this creates heightened risks for the sector should the buying start to dry up.

He suggests that recent moves from Chinese policymakers to stymie capital outflows from the country not only heighten risks for apartment prices and settlement on newly constructed apartments, but are also a crucial cog in Australia’s economic transition, the booming residential construction sector.

“At some point, the Chinese authorities, who appear to have stabilised last year’s spectacular near USD 1 trillion loss in foreign reserves, may decide to slow this leakage,” says Evans.

“Certainly we have seen marked evidence of a tightening of capital controls, particularly for the non-corporate sector. That tightening of capital controls might also impact the construction boom.”

Adding to the uncertainty, Evans says that Australian banks have stopped funding FIRB buyers, suggesting that this presents “risks to local developers who may have sold more than 50% of their stock to these buyers”.

“It is generally accepted that apartment buyers in the Melbourne CBD have incurred some capital losses, while Sydney purchasers are seeing their profits squeezed,” he says. “These liquidity and capital loss prospects may discourage foreign buyers, with the result of sharply slowing the apartment construction cycle.”

Evans, like others, is unsure how it will all play out, noting that possible outcomes range “from ongoing spectacular momentum to a sudden liquidity driven slowdown”.

In the case of the latter, he says “one part of the recent boost to Australia’s growth story might fade quickly”.

The sentiment expressed by Evans is similar to that communicated by a growing number of analysts.

In a research note released in early September, Ivan Colhoun, chief markets economist at the National Australia Bank, suggested that the presence of a large numbers of foreign investors in these markets complicates not only the outlook for prices but also settlement risks.

“Recent trends and reports suggest there has been a modest increase in delays in settlement rather than outright non-settlement. And it is typically foreign buyers that are now finding it somewhat harder to access finance and/or expatriate finance (the latter largely from China),” he wrote.

Cameron Kusher, research analyst at CoreLogic, suggested in May that tighter restrictions on overseas buyers from Australian banks was a factor that could amplify settlement risks for newly built apartments in the years ahead.

“Mortgage lenders have recently tightened their lending criteria, subsequently some people who have committed to off-the-plan units may not be able to borrow as much as they could at the time of signing the contract,” said Kusher.

As a result, Kusher noted that there was a clear risk that some properties may be be worth less than the price they were purchased for, heightening settlement risks.

“Many of the units are coming up for settlement in similar locations and will compete with existing unit stock,” he said.

“With so much stock coming online at once there is an increasing concern as to whether settlement valuations will actually meet the contract price of these units.”

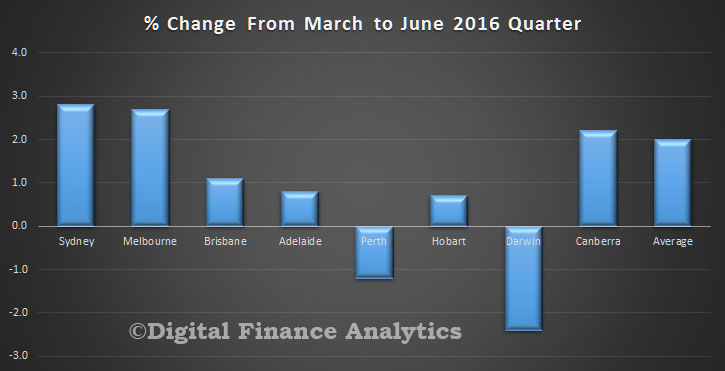

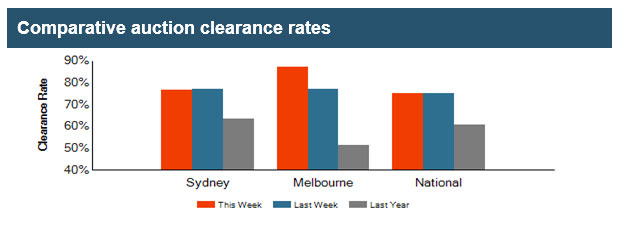

So, we really cannot drawn many conclusions from this set of results.

So, we really cannot drawn many conclusions from this set of results.