According to CoreLogic, the preliminary auction clearance rate was recorded at 69.1 per cent this week, having risen from 67.4 per cent last week. This week’s rise represents a further improvement from the recent low of 65.7 per cent over the weekend leading up to the Queen’s birthday public holiday. There were 2,189 auctions held across the combined capital cities this week, up from 2,183 over the previous week. Auction performance remains well below the comparable week last year when 76.9 per cent of the 2,249 auctions cleared. For the tenth week in a row, Sydney recorded a clearance rate that was in excess of 70 per cent.

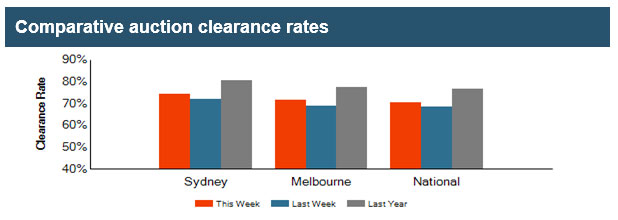

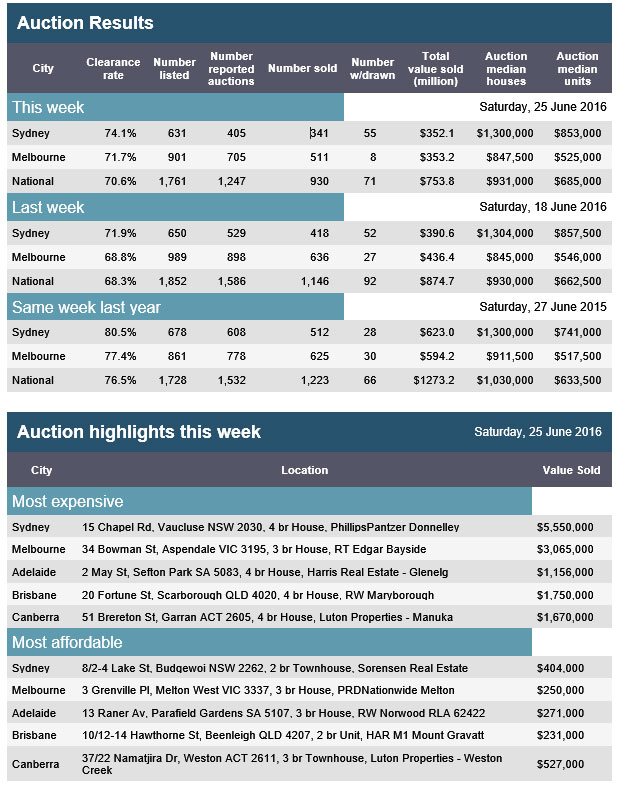

The results from APM Pricefinder for 25 June 2016 are out, and nationally, auction rates were 70.9%, up from 68.3% last week. Sydney cleared 341 sales at 74.1%, whilst Melbourne sold 511 at 71.7%. Results are still strong, though still a little lower than this time last year.

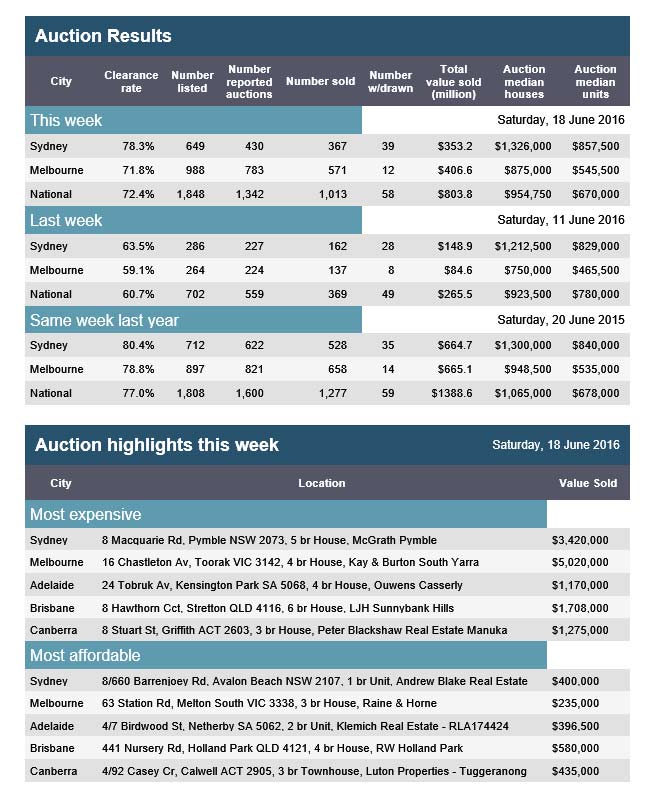

These results provide a leading indicator of property market activity based on a majority sample of auctions that take place every Saturday.

Banking regulator APRA Is “dialling up” the scrutiny on banks’ commercial real estate lending after double-digit loan growth.

Charles Littrell, APRA’s executive general manager for supervisory support said the regulator was turning up the pressure amid fears of an apartment oversupply.

According to a report in The Australian, with estimates of a national oversupply of 70,000 apartments, Littrell said it was “not a bad time to be seeing banks strengthen the equity position in their balance sheet”.

Speaking at a Centre for International Finance and Regulation event yesterday, Littrell said commercial property had historically been what “goes wrong” for the banking system. Plus, there is now the added risk of becoming “so systemically concentrated”.

“In 1990 the four major banks had 40% of the banking market; now they’ve got 80%,” he told the event, The Australian has reported.

“They’re all in the same business model, they’re all hugely exposed to each other … and we don’t quite know what would happen if that business model gets whacked by external stress all at once.

“So there is a lot of conventional work at our end – focusing on sound lending and in fact now we’re dialling up our systemic supervisory focus on commercial real estate.”

Luci Ellis, the Reserve Bank head of financial stability, echoed APRA’s concerns. She told the event that commercial property and development was one area that lacked research since the global financial crisis to draw on.

“The thing that has tended to be the causal agent in a banking crisis, even though you saw something go wrong in housing prices, it was the property developers, it was the commercial real estate, these are the vectors of distress,” she said, according to The Australian.

According to Credit Suisse, total bank commercial real estate lending has boomed in the past three years, with exposures growing 10% to $214bn for the year to March, the highest rate of growth since the GFC.

Over the last 25 years, home ownership rates have fallen sharply for young Australians. Between 1982 and 2011, the home ownership rate for young adults aged 25 to 34 years dropped from 56% to 34%. Growing concerns about their home ownership prospects have prompted those in Generation Y (defined as 18-35 years for the purposes of this article) to become increasingly vocal about the difficulties of achieving home ownership.

The vast majority (86%) of Gen Y households living in the private rental sector or with their parents aspire to own a home, although not necessarily in the short term. Of these households, 30% believed they would be able to buy a home in the next two to five years. One-quarter believed home ownership was five to ten years away. Only 6% did not believe they would ever be able to buy a home.

Although many are choosing to delay home ownership as a lifestyle choice, others are forced to delay because of a lack of affordable housing options. Across all age groups, home owners were more likely to perceive their housing as affordable.

The survey reported that those living in unaffordable housing were making significant sacrifices to meet their housing costs. And 55% said sustaining high housing costs was leading to mental health issues, with those most affected in the private rental sector. This highlights the importance of affordable housing.

The ‘bank of mum and dad’

The deposit gap is the biggest barrier to home ownership. The survey calculated the average gap between the deposit currently available to an individual and the amount the individual expected to need for home purchase. This gap was around A$50,000.

Among Gen Ys already in home ownership, 38% reported they had received financial assistance from their parents or grandparents. For those yet to enter home ownership, only 17% expected to receive some assistance to buy. A further 24% indicated help might be offered.

Therefore, almost 60% of Gen Ys surveyed are unlikely to receive the benefit of intergenerational assistance. This may prevent them from ever entering home ownership.

Parental assistance to purchase

Housing opportunities for ‘Generation Rent’

Assistance for home purchase is becoming more and more important for Gen Ys. They are being dubbed “Generation Rent” as the Great Australian Dream of home ownership moves further out of their reach.

Among Gen Y survey respondents, three-quarters rated the First Home Owner Grant and stamp duty relief as being important in helping them into home ownership. Even the scrapped first home saver accounts scheme was viewed as important. The generation is becoming increasingly reliant on these volatile demand-side incentives.

Importance of government assistance

So what can be done to help those who wish to enter home ownership but lack financial support? Government-backed low-deposit loans such as Keystart in Western Australia and Homestart in South Australia, which are designed for those on low to moderate incomes, have made a real difference to thousands of households. Although not without risk to government, these type of loans could be introduced in other states.

Shared ownership products enable the purchaser and a third party to share ownership of the dwelling, which reduces deposit requirements and monthly payments. These are successful in the UK, accounting for 18% of total housing stock, and are growing in popularity in Australia under the schemes noted above. There may be scope for community housing providers to step into this sector in partnership with private developers.

Discounted home ownership is another option. This option could be tied to developer contributions as part of inclusionary zoning requirements. However, it must be structured in a way that ensures any discount on the market price is retained in perpetuity.

The National Rental Affordability Scheme had its critics but at least provided a supply of affordable housing that reduced the rental burden for many households. That, in turn, increased their chances of saving for a deposit.

The rental sector is in dire need of a replacement scheme, which could possibly be enhanced using a model whereby investors offering new rental dwellings below market rents for a defined period are eligible for stamp duty relief. The argument will be raised that this will encourage demand from investors, raising prices.

It is more critical than ever for government to implement meaningful structural reforms that improve home purchase affordability for Generation Y. Otherwise, growing numbers of Gen Ys all over Australia face a lifetime of renting without the financial and emotional security of home ownership.

Authors: Steven Rowle, Director, Australian Housing and Urban Research Institute, Curtin Research Centre, Curtin University;Amity Jame, Senior Research Officer, Curtin Business School, Curtin University;Rachel On,Deputy Director, Bankwest Curtin Economics Centre, Curtin University

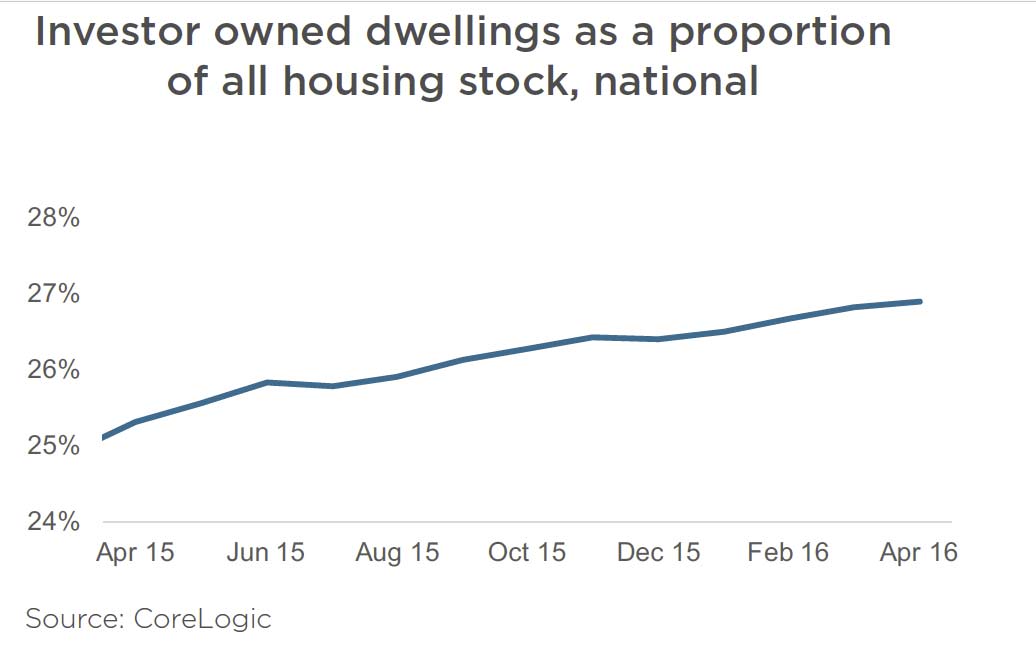

Nationally, investor owned dwellings comprise 26.9% of all housing stock, but 23.8% of the value of all housing stock, highlighting that investment in the housing market is generally across lower valuation segments compared with owner occupied homes.

At a national level investment is generally skewed towards the lower valuation brackets; 53.4% of investment-owned dwellings have a current estimated market value of less than $500,000, compared with 46.9% of owner occupied dwellings. Additionally, each capital city shows the large majority of investor -owned dwellings have an estimated market value that is lower than the capital city median value.

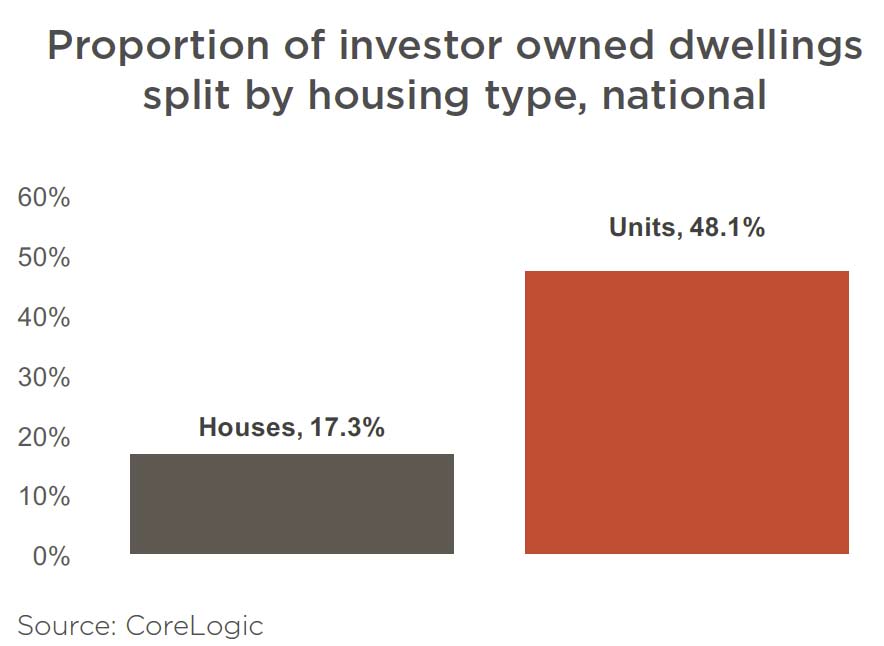

Across the broad product categories of houses versus units, investment is heavily concentrated within the unit sector, where investor owners comprise almost half (48%) of all attached housing.Conversely, detached housing ownership is more biased towards owner occupiers, with investors accounting for 17% of all detached housing stock.

CoreLogic estimates there are 2.6 million investor owned dwellings across Australia worth approximately $1.37 trillion. Based on the most recent taxation data, there are 2.03 million individuals who indicated they owned a residential rental property, implying a very low concentration of investment (approximately 1.28 investment properties per investor).

Actually, you need segment the investment sector, as we do, between Portfolio Investors, who have multiple investment properties (average number 8) and Property Investors who have one or two properties. Averaging across all property investors misses this important segmentation.

According to the ABS, the total value of Australia’s 9.7 million residential dwellings increased $15.4 billion to $5.9 trillion. The mean price of dwellings in Australia is now $613,900. CoreLogic, on the other hand, says property is worth an estimated $6.5 trillion across 9.6 million dwellings, with an average price of $677,000!

In any event, they are right to say “the housing asset class is worth more than three times the value of Australian superannuation funds ($2.0 trillion) and more than four times the value of Australian listed stocks ($1.5 trillion)”.

CoreLogic RP Data says their preliminary results show that 67.8 per cent of reported auction results were sold this week, increasing from the dip to 65.7 per cent last week when auction volumes were lower. Data from APM on Saturday also showed an increase, though their mix of results are different.

CoreLogic says this week 2,139 capital city auctions were held, up from 1,100 last week and a similar volume compared to one year ago (2,268). At the same time last year, 77.3 per cent of auctions cleared. The trend in auction clearance rates has nudged lower over the last few weeks; across the quieter auction market last week, three cities recorded a clearance rate in excess of 70 per cent: Adelaide, Canberra and Sydney, while this week, Sydney is the only city where clearance rates are tracking above 70 per cent.

The opening quarter of 2016 was not the greatest three months for Brisbane’s property market and one member of the real estate industry believes the end of the current growth cycle in the city and the wider south east Queensland region is already in sight.

Figures released this week by the Real Estate Institute of Queensland (REIQ) show the median house price in the Greater Brisbane area fell 4% over the March quarter to $480,000, while in the Brisbane Local Government Area, which encompasses the city’s inner suburbs, the median house price fell 2.4% to $620,000.

Speaking to Australian Broker‘s sister publication,Your Investment Property, REIQ chief executive officer Antonia Mercorella said the March quarter was a “slow” one for Brisbane, but she believes there isn’t too much cause for concern.

“Both of those markets, which had been performing consistently well slipped a little bit in the quarter. But that is only one quarter so we do need to be careful not to draw too much from that or sound the alarm bells at this stage,” Mercorella told Your Investment Property.

“Both the LGA and Greater Brisbane have been performing consistently well and if you look at the broader data they’re still tracking nicely,”

According to the REIQ’s figures, the Greater Brisbane median house price has grown 2.1% growth over 12 months to March and 7.8% over the past five years, while in the Brisbane LGA the median house price is up 6.1% over the 12 months to March and 17.9% over the past five years.

Mercorella said figures from the June quarter may too show a softening in Brisbane’s performance due to the impact of the ongoing Federal Election campaign; however she predicts the market will bounce back relatively quickly after the campaign is completed.

While Mercorella believes Brisbane still has plenty of fuel in the tank, Scott Northcott, director of Queensland based Real Property Advice, believes the peak of the current cycle is steadily drawing closer for the Queensland capital.

For Northcott, one of the factors that had breathed life into the south east corner of Queensland will also be its undoing as he predicts a post-Commonwealth Games slump.

“Brisbane will always follow Sydney and Melbourne and precede places like Adelaide, Perth and Darwin, that’s just the order things happen,” he told Your Investment Property.

“In our on the ground experience we have seen very strong price growth activity over the last 24 months and even a bit longer.

“I think we’ve got 18 more months for decent activity and I think after the Commonwealth Games at the end of 2018 we’re going to see quite an abrupt slowdown starting from the Gold Coast area. The Gold Coast will sort of infect upwards from there.”

The REIQ’s figures show over the March quarter that the median house price on the Gold Coast increased 0.5% to $557,500 and is 5.8% higher than 12 months ago and 10.2% higher than five years ago and Mercorella doesn’t believe the end of the Commonwealth Games activity will bring the Gold Coast and surrounding regions to a halt.

“I don’t think that’s going to be the case. Obviously there’s a lot of new construction going on there at the moment and other things because of the Commonwealth Games, but we were already sort of seeing the gold coast bounce back from the GFC anyway,” she said.

“I don’t think it’s going to be this situation that after the games we’re going to be left with this glut of stock and people are going to leave the Gold Coast.”

But Northcott’s outlook for the region is much grimmer, likening the current state of the Gold Coast to that of areas that went from boom to bust during the resource boom of recent years.

“People are chasing the Commonwealth Games boom.

“The big issue is that there’s a whole lot of stuff being built and sold and everybody thinks it’s all rosy, but when investors, both international and local, want to get out post Commonwealth Games they’ll simply dump their stock.

“Twelve to 18 months after the games there will be a bad taste in people’s mouths and then from mid-2020 to 2001 we’ll power on again.”

According to the APM Home Price Guide Auction results for 18th June 2016, the national clearance rate was 72.4%, up from 60.7% last week. Sydney led the way with a 78.3% sold, but Melbourne had the largest number of sales. Whilst the results are a little down on last year, its still looking pretty hot at the moment.

APM publishes auction activity results for the Sydney, Melbourne,Brisbane and Adelaide capital cities every Saturday evening, providing a snapshot of how demand and supply in the auction market is behaving and as a leading indicator for the overall property market. (Auction activity for the other capital cities is also monitored and made available by mid week). You can read about their methodology here.

Housing affordability and tax reform have shaped up to be two of the defining issues this election. The Property Council of Australia – which describes itself as “the Voice of Leadership” – has helped frame the debate on behalf of its 2200 company members.

The council began as the Building Owners and Managers’ Association of Australia (BOMA) in 1969, and was renamed the Property Council of Australia in 1996, with advocacy a core focus. The Residential Development Council and International and Capital Markets division were formed in 2001 and the Retirement Living Council in 2015.

With a board of directors drawn from Australia’s largest residential and commercial developers, the Property Council’s considerable annual revenue (A$27.3 million in 2015) is drawn primarily from membership fees and services.

The financial stakes are high when it comes to lobbying for regulatory settings which favour property development and investment. The Property Council’s healthy budget for advocacy and communication ($6.4 million and $1 million in 2015 alone) has generated a voluminous amount of reports, advertising campaigns and government submissions on taxation and planning reform. Another $7.2 million for “networking” ensures that this information is disseminated where it counts.

These deep coffers have funded the Council’s high profile television campaign to preserve negative gearing and capital gains tax discounts in response to mooted changes early this year. Likening the housing market to a fragile house of cards on the brink of collapse, the ad (released on 22 February) carried a menacing warning, “don’t play with property.”

The government has got the message. The Treasurer, Scott Morrison, who served as National Policy and Research Manager for the Council between 1989-1995 ruled out changes to negative gearing in the lead up to the 2016 Budget. Despite speaking out against negative gearing prior to becoming Prime Minister, Malcom Turnbull also changed his tune recently, rejecting “reckless” changes to existing arrangements and suggesting that aspiring home buyers hit up their parents for help.

While the campaign to retain negative gearing is the Property Council’s most visible, behind the scenes the council has been busy meeting with government and writing submissions. In 2015 alone, the NSW division wrote 55 submissions and attended an extraordinary 230 government meetings. Its 2016 election brochure presents a number of “solutions” to “grow the economy through property”. Here are some highlights.

Negative gearing and the CGT

The council wants to retain negative gearing (which allow interest rates and other expenses associated with housing investment to be offset against total income) and capital gains tax discounts on investment properties. This is despite substantial evidence that these bonuses stimulate demand for housing, pushing up prices and leaving first home buyers unable to compete. But by framing housing affordability problems as a symptom of supply side pressures rather than demand side incentives, the council shifts the affordability debate to planning reform.

Housing and planning reform

Current incentives for property investment (such as negative gearing) don’t target new housing supply – only a small proportion of investor loans finance new dwellings. So the Council argues that Commonwealth payments to the states for “micro economic reform” should incentivise planning system changes needed to “turbocharge housing supply pipelines and deliver innovative affordable housing solutions.”

This is a tired argument which ignores the years of planning reform already undertaken by the states and territories, while levels of new housing production are currently at their highest in decades. This supply has done little to dampen price inflation in a market awash with domestic and foreign investors.

While the Property Council always bangs on about bottlenecks in housing supply (which it argues are caused by planning system constraints), such arguments miss the obvious issue that prices are a result of an interaction of supply and demand. What the combination of negative gearing and capital gains tax do is to drive demand so hard in boom times that even with sharp increases in supply, prices keep on rising, especially in today’s low interest environment.

The chart below shows this problem with respect to Sydney. It shows dwelling completions falling slowly when prices flatlined after the 1996-2004 boom, but rising in line with price inflation from mid 2011 on.

Prices: Department of Family and Community Services, Rent and Sales Report.Source: Completions. NSW Department of Planning, CC BY-SA

The Council’s election platform does call for institutional investment in affordable and social housing, and this is one idea worth taking up.

Cities and Infrastructure

The Property Council support long term infrastructure planning and delivery, coordinated by Infrastructure Australia. Who doesn’t?

But the problem is how to assign the costs and benefits. Land value rises due to investments in public infrastructure – such as a new rail line or road – are typically pocketed by landowners and developers.

Commonwealth and state governments are now canvassing value capture arrangements which would use some of this uplift to offset costs of provision. The council oppose this model, instead suggesting Tax Increment Financing (TIF), which leverages increases to commercial rates in defined districts.

While popular in some parts of the US, it has not been proven effective for larger schemes. It would be difficult to implement in Australia because our recurrent property charges are much lower than the US.

The Property Council also wants existing development contributions towards basic facilities like open space, local roads, and footpaths to be wound back, along with stamp duties on property transactions.

The idea of removing stamp duty has some merit (at least for domestic purchasers), since taxes on property transactions can discourage mobility, deterring retirees from moving to a smaller home, for example. But experts think stamp duty should be replaced by land taxes, to encourage more efficient use of land.

This would also provide a mechanism for capturing back values arising from public infrastructure investment. Not surprisingly, the Property Council thinks otherwise, calling instead for a higher GST.

While the Property Council complains about unfair tax burdens on its members, they seem content to spend a lot of money on their advocacy and networking activities. Described by economists as “premium seeking expenditure”, lobbying for more generous regulatory and financial settings clearly promises a high return for the property sector.

But it’s important to remember that despite their size, the Property Council only represents a portion of the development, construction, and real estate industry – they don’t really cover many smaller suburban developers or house builders. The question is whether the “Voice of Leadership” will dominate the agenda or whether wider perspectives on housing and cities will be heard.

Authors: Nicole Gurra, Professor – Urban and Regional Planning, University of Sydney; Peter Phibb, Chair of Urban Planning and Policy, University of Sydney

We see their spokespeople quoted in the papers and their ads on TV, but beyond that we know very little about how Australia’s lobby groups get what they want. This The Conversation series shines a light on the strategies, political alignment and policy platforms of eight lobby groups that can influence this election.

Excellent post from Cameron Kusher, CoreLogic RP Data, discussing the impact of the higher tax being imposed by several states on foreign investors in the context of state tax raising – they are highly dependent on stamp duty to support their coffers. He concludes that ultimately these changes may deter some foreign investment but these changes are not going to scare off all foreigners from investing in housing market. At the same time it will raise much needed revenue for these governments. If state governments are looking at taxes on property, they should move away from stamp duty to a more efficient land tax.

The state governments of New South Wales, Victoria and Queensland are all now charging additional tax on foreign investment in residential property. In New South Wales foreign buyers are being charged a 4% stamp duty surcharge from June 21. In Victoria, foreign buyers are charged a 7% tax and in Queensland foreign buyers are being charged a 3% surcharge. All three of these taxes are specifically targeted on transactions of property by foreign buyers.

Property (both residential and non-residential) is already the largest source of taxation revenue for state and local government. These additional charges to foreign investors in the three most populous states will probably raise additional revenue (as long as the higher cost of doing business doesn’t result in a downturn in demand from overseas buyers). For each government there is a benefit in these changes outside of additional revenue, foreigners don’t vote so politically it is likely to be a fairly popular decision. Especially in New South Wales and Victoria where housing affordability is a growing problem and there is a perception that foreign investors are bidding up prices and contributing to locking first home buyers out of the market.

In New South Wales, state and local governments collected $14.705 billion in property taxes over the 2014-15 financial year. Property tax revenue increased by 12.8% over the year and has increased by 80.5% over the decade to 2014-15. Property taxes accounted for 48.5% of total taxation revenue to New South Wales state and local government in 2014-15.

In Victoria, state and local governments collected $12.246 billion in property taxes over the 2014-15 financial year which accounted for 53.1% of total taxation revenue. Property tax revenue increased by 10.7% over the 2014-15 financial year to be 109.9% higher over the past decade.

Queensland property tax revenue increased by 12.6% over the 2014-15 financial year to be 80.7% higher over the decade. Over the 2014-15 financial year Queensland state and local governments collected $8.267 billion in property tax revenue which accounted for 51.5% of total state and local government tax revenue.

Over the decade to June 2015, property taxes have increased by 80.5% in New South Wales, 109.9% in Victoria and 80.7% in Queensland, over the same timeframe inflation has increased by 30.1% which is significantly lower than growth in property taxation.

Given the importance of property tax revenue to state and local governments it is no wonder that the three largest states have decided to increase taxes on foreign investment. These changes don’t impact on voters and they collect additional much needed revenue.

My concern is that it shows that none of these states have any intention of moving away from transactional taxes on property to more efficient land taxes. Keep in mind that in a typical year only around 5% to 7% of residential properties are transacting so you are only collecting stamp duty from a small proportion of the housing market that are deciding to move. When transactions and values slow or fall, stamp duty revenue is also susceptible to large declines.

In New South Wales and Victoria, governments are gaining substantial revenue from stamp duty as property values and transactions rise. In New South Wales, stamp duty collection rose 22.2% in 2014-15, in Victoria it rose by 18.9% and in Queensland it was 12.3% higher. Over the past decade, the total increase in stamp duty revenue has been recorded at: 125.1% in New South Wales, 116.8% in Victoria and 56.1% in Queensland.

Some of the commentary around the increases in tax have been around the fact that without foreign investors many of the new housing (particularly unit) projects would never have even commenced construction. To me, this is really the crux of the problem. As the resource investment boom has faded to some extent housing construction has helped to fill the void. If a projects viability is totally dependent on foreign demand, to me that suggests that it is not really a viable project. The reality is that the current home value growth phase has now been running for four years and new housing construction and unit construction in particular has hit record highs. Foreign investment has increased quite significantly over this time however, many of these purchasers are buying units which many locals wouldn’t purchase due to the size, location and price of these properties. Furthermore, anecdotally many of these properties don’t actually create additional housing because they are left empty and not made available for rent.

I believe that these additional charges will provide some deterrent for foreign buyers investing as the costs continue to add up with FIRB application fees and now these additional charges. Of course, while these changes may deter some investors other will just see it as a cost of doing business and it shouldn’t impact them too much if they are investing for the long-term. If fewer foreign investors results in some new housing projects not going ahead, that is not necessarily a problem either in light of the fact that housing supply has increased dramatically over recent years and will continue to do so over the coming years given the housing currently under construction. Finally if it means that certain developers decide to rotate their offering away from one catering to foreign buyers and towards one which is more palatable to a local market, I believe that is a good thing.

Ultimately these changes may deter some foreign investment but these changes are not going to scare off all foreigners from investing in housing market. At the same time it will raise much needed revenue for these governments. If state governments are looking at taxes on property I would once again call on them to look for a way to move away from stamp duty to a more efficient land tax.