As the term enters our everyday vocabulary, HR professionals and employment law specialists like me now face the age-old question: What happens if people start saying “OK boomer” at work?

Evidence of discrimination

A lot of the internet fights over “OK boomer” revolve around whether

the phrase is offensive or not. But when you’re talking about the

workplace, offensiveness is not the primary problem. The bigger issue is

that the insult is age-related.

Workers aged 40 and older are protected by a federal statute called the Age Discrimination in Employment Act, which prohibits harassment and discrimination on the basis of age.

Comments that relate to a worker’s age are a problem because older

workers often face negative employment decisions, like a layoff or being

passed over for promotion. The only way to tell whether a decision like

that is tainted by age discrimination is the surrounding context:

comments and behavior by managers and coworkers.

If a manager said “OK boomer” to an older worker’s presentation at a

meeting, that would make management seem biased. Even if that manager

simply tolerated a joke made by someone else, it would suggest the boss

was in on it.

Companies also risk age-based harassment claims. Saying “OK boomer”

one time does not legally qualify as harassing behavior. But frequent

comments about someone’s age – for example, calling a colleague “old” and “slow”, “old fart” or even “pops” – can become harassment over time.

Gen Xers are covered too

And it doesn’t matter if the target isn’t even a boomer.

Gen Xers were born around 1965 to 1979. That makes them older than 40 and covered by federal age discrimination law.

Yes, I get that the comment is a retort to “unwoke” elders

who cannot be reasoned with. The problem is that the phrase is intended

as a put-down that is based, at least partly, on age. If you say it at

work, you’re essentially saying, “You’re old and therefore irrelevant.”

Lumping Gen Xers into a category with even older workers doesn’t make it better. Either way, you are commenting on their age.

A lot of them were quite funny, like the hairdresser imitating a

customer who criticized her tattoos as unprofessional. She responded,

“OK boomer,” while appearing to lop off a huge swath of the customer’s

hair.

When I was an employment lawyer, I heard tons of hilarious stories of

things people said in the workplace. But that’s the point: The story

ended with a lawyer on the other end of the phone.

One of the most famous

age-discrimination cases – which made its way all the way up to the

Supreme Court – involved a manager who described an employee as “so old

he must have come over on the Mayflower.”

In other words, “it was just a joke” is an awful legal defense.

Tit for tat

To millennials who have suffered through years of being called

“snowflakes” by their elders, protests of age discrimination can seem a

bit rich. Why didn’t HR ban all those millennial jokes about avocado toast?

The Age Discrimination in Employment Act only kicks in for workers

who are 40 or older, which means millennials aren’t covered. For now.

The oldest millennials will turn 40 later this year. So fear not, the

millennial jokes may eventually become a legal problem for companies as

these workers age.

Also, a few states, including New York,

ban age discrimination for all workers over 18, and employers in those

states probably should have done something about the millennial jokes.

Boomers might seem really powerful, and yes, they might be your boss’s boss’s boss.

But older workers are more vulnerable than they seem. Older workers

are expensive – by the time they’ve worked their way up the corporate

ladder, their generous salaries start to weigh on the balance sheet. And

management may have trouble

envisioning spectacular growth and innovative ideas from them years

into the future, even if they are ready and willing to deliver.

That’s why Congress thought it was important to extend protections to those workers. It wanted employers to treat them as individuals who shouldn’t be dismissed out of hand because of their age.

And in many ways, that’s what young people seem to want as well: a little respect for what they bring to the table. After all, that meme didn’t make itself.

Author: Elizabeth C. Tippett, Associate Professor, School of Law, University of Oregon

According to an article in the New Daily today by Samantha Maiden, “Families would be able to claim child care costs of up to $60,000 a year as a tax deduction under a proposal to be launched by Liberal MP David Sharma on Tuesday”.

However, the biggest benefits go to families with a combined income

of $280,000 a year or more who could slash their combined taxable income

to $220,000.

Under the proposal, a family that could afford to

pay a nanny $60,000 a year could split the cost 50:50 between two

working parents as a tax deduction.

Each parent would then be able to reduce their taxable income by $30,000.

The Productivity Commission has previously recommended against making child care costs tax deductible, on the basis that it is not an effective means of support for lower- and middle-income families.

The article also features modelling by Dr Ben Phillips.

He found the policy would leave more than 205,000 households better off, representing one in five of households with children.

The average couple with children would be $618 per annum better off.

“Although households in the top quintile of the income distribution benefit the most on average with an average benefit of $1080 per annum, those in the second quintile (the bottom 20 per cent to 40 per cent of the income distribution) are on average $626 per annum better off. This represents a 1.9 per cent increase in disposal income,” the report states.

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Contents

0:20 Introduction

1:05 Live Stream 19th Nov

1:30 US

2:00 US China Trade

2:50 US Economy

3:10 CASS Shipping

4:40 Fed Policy

5:20 US Markets

07:57 Hong Kong

8:25 UK

09:35 New Zealand

11:22 Australian Section

11:23 Employment

12:00 Wages

13:20 Sentiment

14:00 Home Prices

17:18 Auctions

17:50 Pay Day Research

19:10 Insolvencies

20:00 RBA on Mortgage Arrears

22:35 Australian Markets

November Live stream: https://youtu.be/dMaixx5Sf34

DFA provided data from our household surveys to inform an important report “The Debt Trap” released by more than 20 agencies helping consumers with their financial pressure. Our research, based on our rolling 52,000 households reveals that more households are using short term loans to try and manage their budgets, but many get trapped into debt. This is important given the rise in mortgage stress across the country.

The report also contains case studies which bring home the risks involved.

Worse, the recommendations from an earlier Government review are apparently in a holding pattern, and as a result more are being sucked in due to Government inaction.

Finally, the rise of apps and online lenders is making is easier for desperate households to get caught up with high cost short term debt.

Here is the official release.

Over 20 consumer advocacy bodies from around the country have

released new data revealing that predatory payday lenders are profiting

from vulnerable Australians and trapping them in debt, as they call for

urgent law reforms.

The Debt Trap: How payday lending is costing Australians

projected that the gross amount of payday loans undertaken in Australia

will reach a staggering 1.7 billion by the end of 2019. It also found

that:

Over 4.7 million individual payday loans were taken on by around

1.77 million households between April 2016 and July 2019, worth

approximately $3.09 billion.

Victoria is the state leading the country with the highest number of new payday loans

Digital platforms are adding fuel to the fire, with payday loans that originate online expected to hit 85.8% by the end of 2019.

The number of women using payday loans has risen from 177,000 in

2016 to 287,000 in 2019, representing a rise to 23.13% of all borrowers.

Close of half are single mothers.

The report was released today by over 20 members of the Stop the

Debt Trap Alliance – a national coalition of consumer advocacy

organisations who see the harm caused by payday loans every day through

their advice and casework.

“The harm caused by payday loans is very real, and this newest data

shows that more Australian households risk falling into a debt spiral,”

says Consumer Action CEO and Alliance spokesperson, Gerard Brody.

“Meanwhile, predatory payday lenders are profiting from vulnerable

Australians to the tune of an estimated $550 million in net profit over

the past three years alone.”

Brody says that the Federal Government has been sitting on

legislative proposals that would make credit safer for over three years,

and that the community could not wait any longer.

“Prime Minister Scott Morrison and Treasurer Josh Frydenberg are

acting all tough when it comes to big banks and financial institutions,

following the Financial Services Royal Commission. Why are they letting

payday lenders escape legislative reform, when there is broad consensus

across the community that stronger consumer protections are needed?”

The Alliance is calling on the Federal Government to put people

before profits and pass the recommendations of the Small Amount Credit

Contract (SACC) review into law. This legislation will be critical to

making payday loans and consumer leases fair for all Australians. There

are only 10 sitting days left to get it done.

“The consultation period for this legislation has concluded. Now it’s

time for the Federal Government to do their part to protect Australians

from financial harm and introduce these changes to Parliament as a

matter of urgency.”

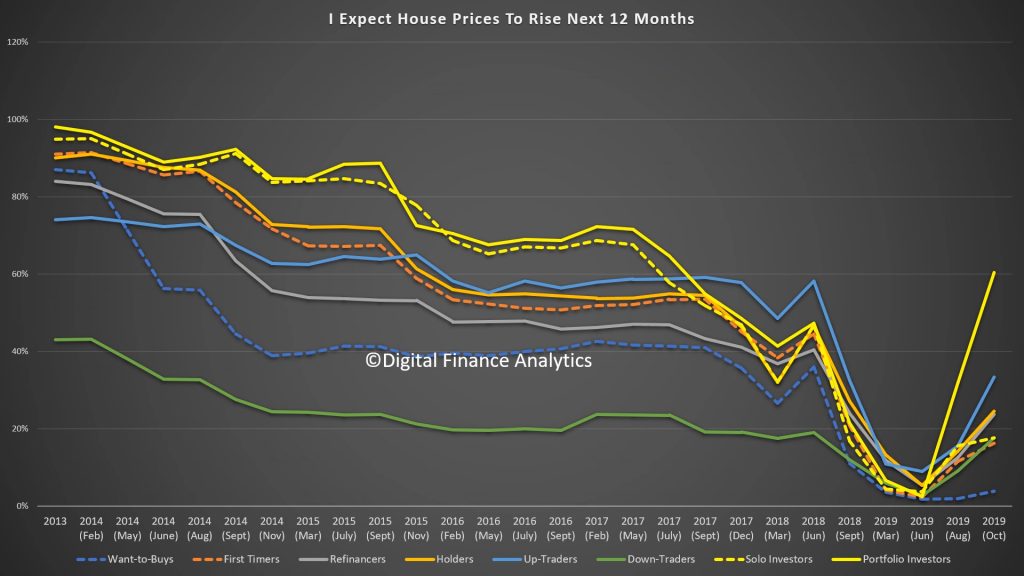

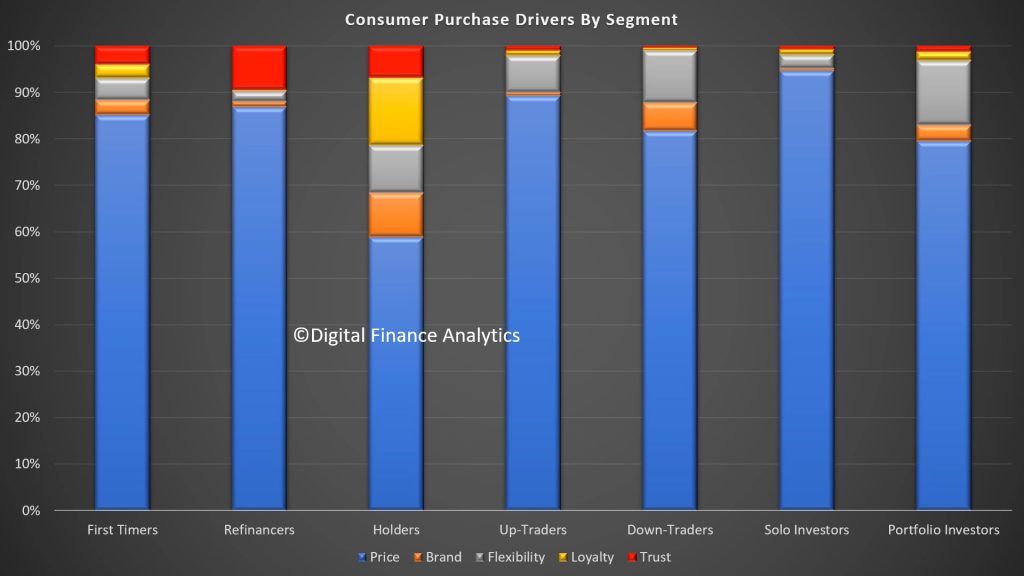

In the final part of our October 2019 Household Survey we look at the results through the lens of our segmentation models. What is clear is there is a disconnect between future home price expectations (much more positive) and proposed activity (lower demand for credit, and intentions to transact). This is at the heart of the weirdness in the market at the moment, and it helps to explain the low levels of listings and transactions (and hence the high auction clearance rates on those low volumes). There is nothing in the latest results however which flags significant momentum increases ahead.

We start with the cross-segment trends. First there is a significant hike in those expecting home prices to be higher in the next 12 months. It reached a low around the election, and has been rising since the cash rate cuts. Portfolio Investors (those with multiple investor properties are the most bullish). But the expectations are there across the board.

However, this does not necessarily translate into intention to transact. First Time Buyers and Down Traders (around 900k) are most likely to be in the market, the former aided by the extra incentives available and the latter by the need to pull equity from existing properties. Property investors remain largely on the sidelines. There is also a slight downward inflection in the past quarter.

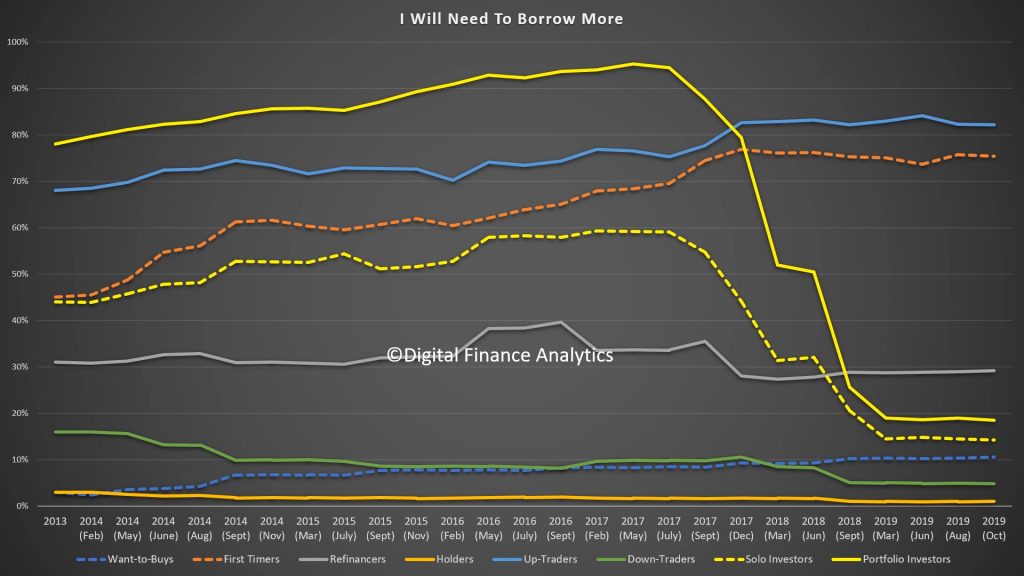

Another lens is demand for credit which shows stubborn resistance other than from First Time Buyers ~around 150k actively looking) and Up Traders (around 550k actively looking). Refinancing is tracking at levels we have seen for some time. This suggests that banks will have to compete hard for meager pickings, and refinancing and first time buyers will be the targets for special deals.

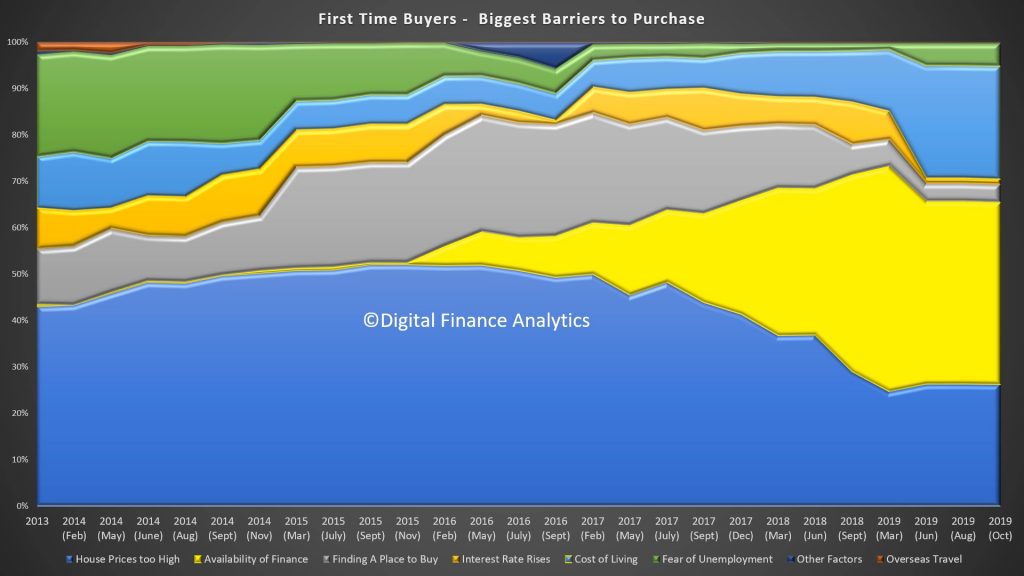

Those Wanting to Buy say that availability of finance (40%) and costs of living (30%) are the main barriers, although high home prices at 16% still registers. Interest rates and fear of unemployment are low relatively speaking.

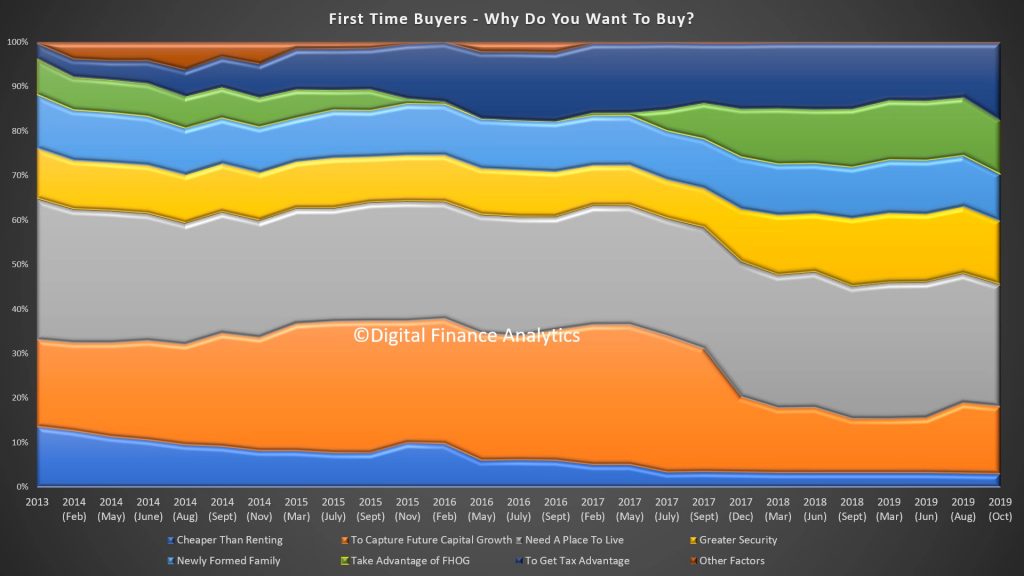

First time buyers are being driven by a range of factors including the need for shelter and a place to live (28%), greater security (14%), tax advantage (17%) and to take advantage of the FHOG (12%). But that said there are significant barriers as well.

Barriers include home prices too high (26%), availability of finance (39%) and costs of living (24%). On the other hand finding a place to buy and rising interest rates hardly registered.

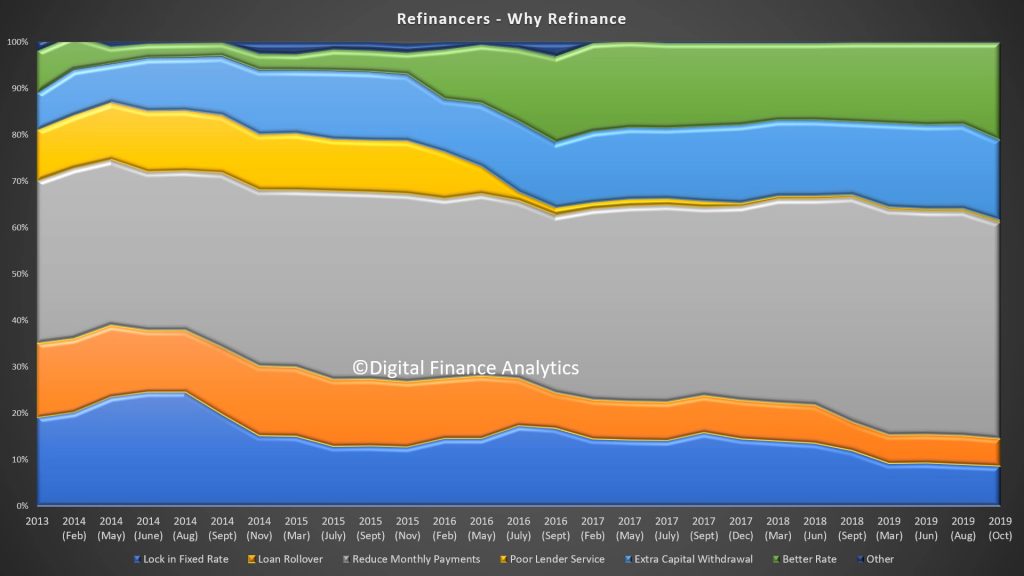

Household seeking to refinance are being driven by reducing monthly repayments (50%), for a better rate (22%) and extra capital withdrawal 20%.

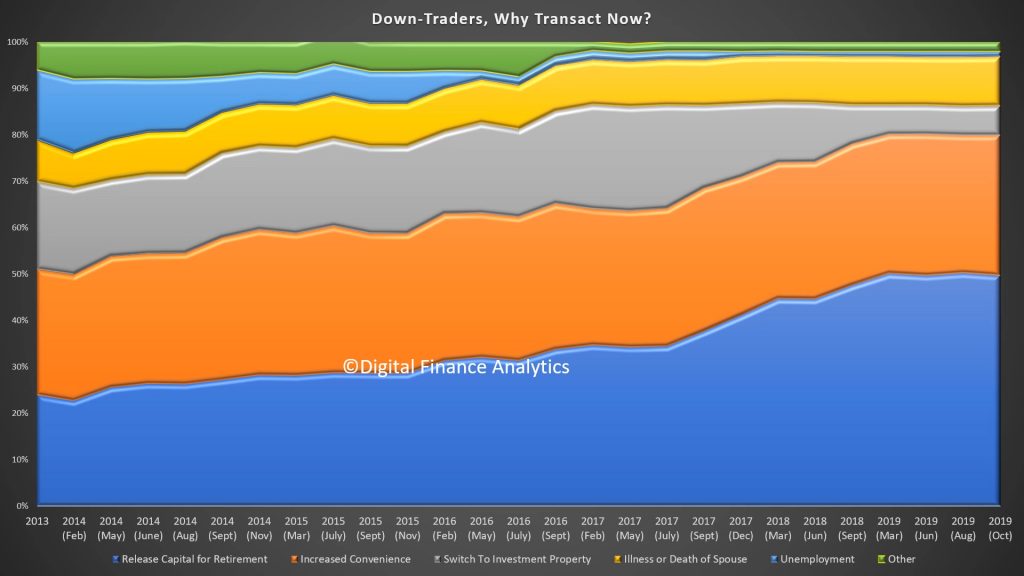

Down Traders are driven by the desire to release capital for retirement (50%), increased convenience (30%) and illness or death of spouse (11%). Interest in investment property has faded to 6%.

Up Traders are being driven by the desire for more space (41%), job change (16%), property investment (22%) and life-style changes 20%).

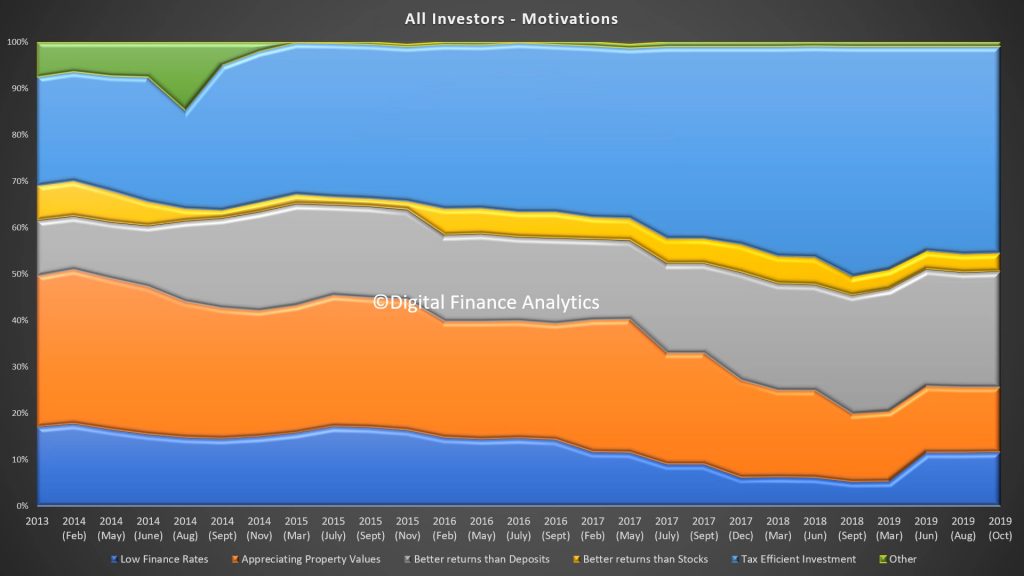

Turning to investors 45% are driven by tax benefits, better returns than deposits (25%) and appreciating property values (14%).

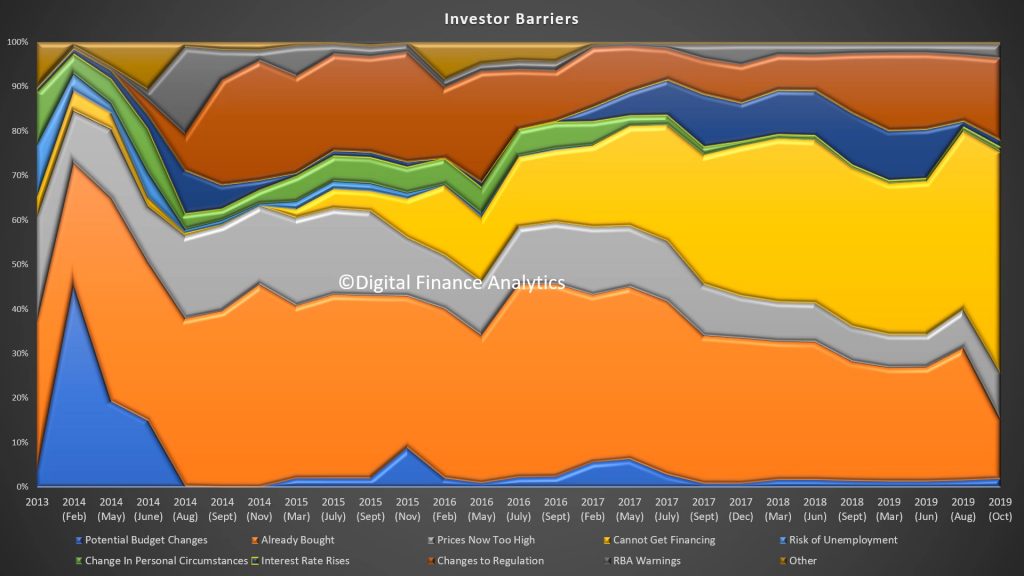

On the other hand, investors face a number of barriers including cannot getting finance (49%), and they have already bought (13%).

And finally across the segments the prime selection point is price, although it varies, and loyalty is not seen as significant or rewarded.

Standing back, it appears that property sector momentum is likely to remain patchy at best, with more action at the more expensive end of the value spectrum, and first time buyers remaining as the primary “canon fodder” with regards to new transactions. It will be interesting to see how the Government scheme due in January changes the picture.

Australians in dispute with their

bank, insurance provider, super fund, or other financial firms have lodged

73,000 complaints with the financial sector’s new ombudsman and have been

awarded $185 million in compensation, in the first 12 months of its operation.

The Australian Financial Complaints Authority (AFCA) is celebrating 12 months since it opened its doors as the nation’s one-stop-shop for complaints about financial firms, replacing three former external dispute resolution schemes.

People made 73,272 complaints to

AFCA between 1 November 2018 and 31 October 2019. This represents a 40 percent

increase in complaints received compared to AFCA’s predecessor schemes, which

in the 2017/18 financial year received a combined total of 52,232 complaints.

Of the complaints made, 56,420 have

been resolved with the majority resolved in 60 days or less.

Research conducted in July this

year showed that just three percent of Australians knew about AFCA. Yet,

despite the need to raise awareness, Australians are making nearly 200

complaints a day.

AFCA Chief Executive Officer and

Chief Ombudsman David Locke said AFCA was a fair, free and independent service

that was fast becoming valued by the public and its members for its approach to

dispute resolution.

“Every day we continue to hear from

people who are dissatisfied with the way their financial firm has handled their

complaint. These matters have not been resolved internally by financial firms

and so the individual then brings their complaint to AFCA,” Mr Locke said.

“We take our commitment to fairness

and independence very seriously, and where possible we encourage the financial

firm and complainant to resolve the matter among themselves. The statistics

show that this happened with 70 percent of all claims resolved in the past 12

months.

“Still, the increase in complaint

numbers we are witnessing at AFCA indicates that there is still work to be done

by firms to improve their practices and restore public faith in financial

firms. AFCA will continue to focus on member engagement to help firms to

enhance their own internal dispute resolution procedures.”

Mr Locke said he was proud of the

significant milestones that AFCA and its people had achieved in its first year

of operation.

“Establishing AFCA as a new

organisation and handling a 40 percent increase in complaints was never going

to be easy and we are still improving the way we operate,” he said.

“I am very proud of the AFCA team

and what has been achieved so far. I am fortunate to work with a great team of

people who are professional, passionate about fairness and independence, and

who care about our customers.

“AFCA has also been in a major growth

phase of staff to meet demand and has launched the first leg of a national

roadshow to promote its service across the country.

“The Financial Fairness Roadshow

has been a great success. So far we’ve been to 26 locations across Tasmania,

Victoria, the ACT and regional New South Wales, where we’ve spoken with more

than 7,000 people.

“We plan to tour the rest of the

country in the first half of 2020.”

Mr Locke said AFCA had also hosted

forums for small business, consumer advocates and AFCA members in 10 locations

coinciding with the Roadshow’s itinerary.

There have been some interesting developments in the short-term lending market in the UK recently. The Financial Conduct Authority in the UK recently published data on the so called high-cost short-term credit (HCSTC) market. HCSTC loans are unsecured loans with an annual percentage interest rate (APR) of 100% or more and where the credit is due to be repaid, or substantially repaid, within 12 months. In January 2015, The FCA introduced rules capping charges for HCSTC loans.

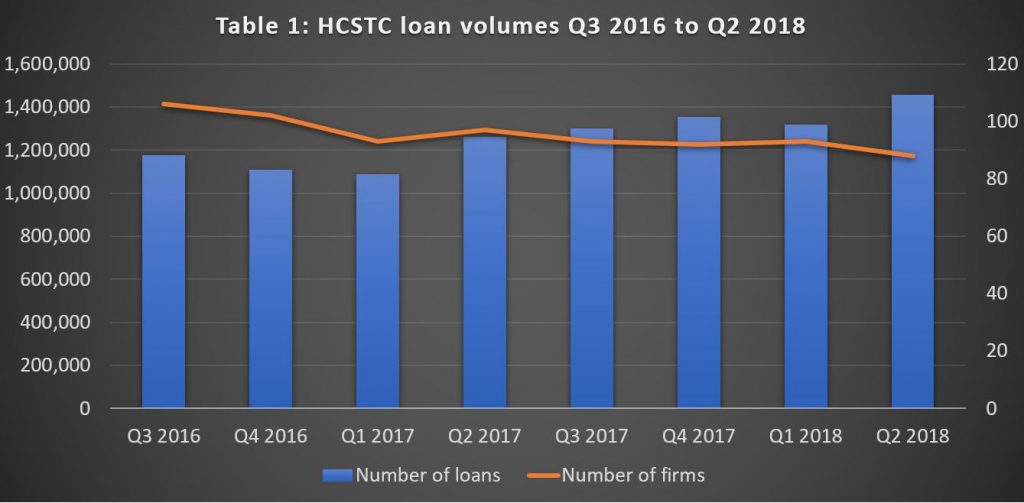

Just over 5.4 million loans originated in the year to 30

June 2018, and that lending volumes have been on an upward trend over the last

2 years. Despite some recovery, current lending volumes remain well down on the

previous peak for this market. Lending volumes in 2013, before FCA regulation,

were estimated at around 10 million per year.

These data reflect the aggregate number of loans made in a

period but not the number of borrowers, as a borrower may take out more than

one loan. They estimate that for the year to 30 June 2018 there were around 1.7

million borrowers (taking out 5.4 million loans).

The market is concentrated with 10 firms accounting for

around 85% of new loans. Many of the remaining firms carry out a small amount

of business – two thirds of the firms reported making fewer than 1,000 loans

each in Q2 2018.

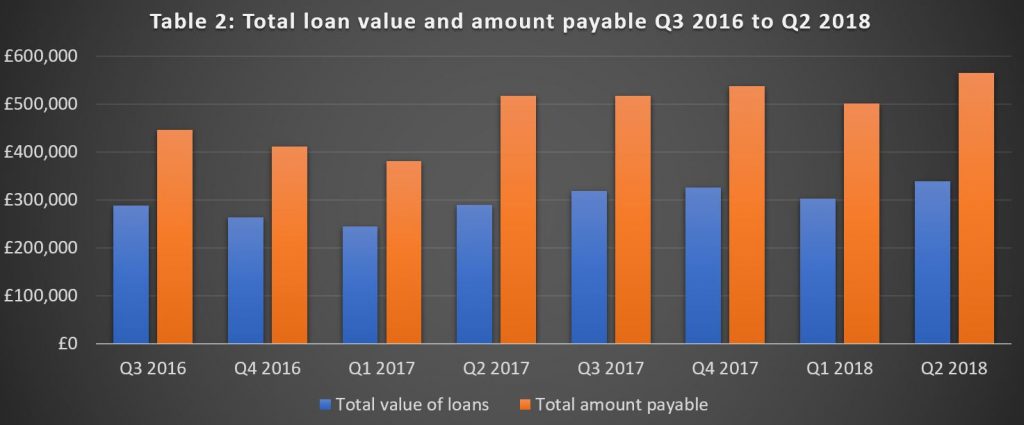

For the year to 30 June 2018, the total value of loans

originated was just under £1.3 billion and the total amount payable was £2.1

billion. Figure 2 shows that the Q2 2018 loan value and amount payable mirrored

the jump in the volume of loans with loan value up by 12% and amount payable

13% on Q1 2018.

The average loan value in the year to 30 June 2018 was £250.

The average amount payable was £413 which is 1.65 times the average amount

borrowed. This ratio has been fairly stable over the past 2 years. A price cap

introduced in 2015 stipulates that the amount repaid by the borrower (including

all charges) should not exceed twice the amount borrowed.

Over the past 2 years the average Annual Percentage Rate (APR) charged for HCSTC has been consistent, hovering around 1,250% (mean value). The median APR value is slightly higher at around 1,300%. Within this there will be variations of APR depending on the features of the loan. For example, the loans repayable by installments over a longer period may typically have lower APRs than single installment payday loans.

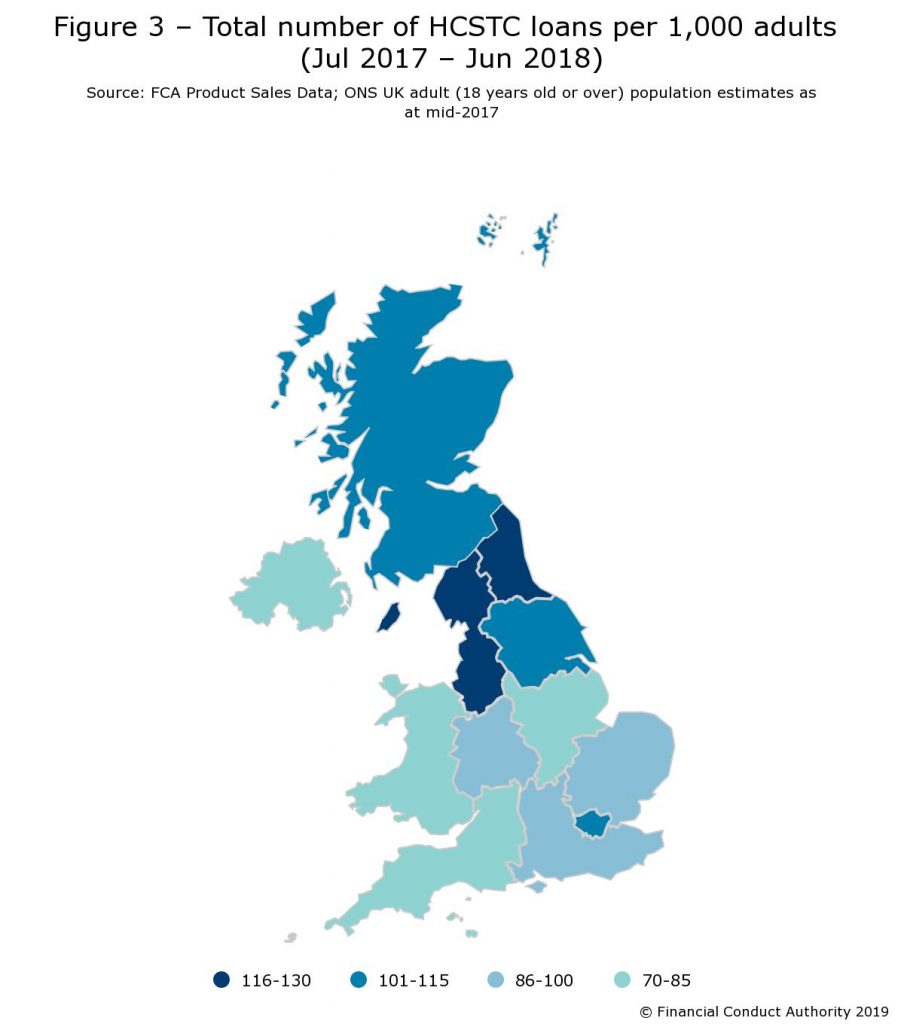

In the UK, the North West has the largest number of loans

originated per 1,000 adult population (125 loans), followed by the North East

(118 loans). In contrast, Northern Ireland has the lowest (74 loans).

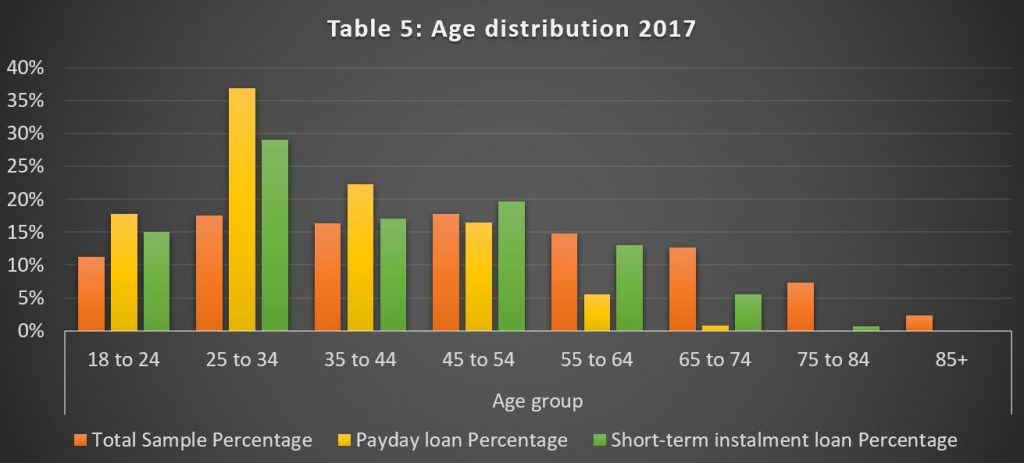

Borrowers between 25 to 34 years old holding HCSTC loans (33.4%) were particularly over-represented compared to the UK adults within that age range (17.5%). Similarly, borrowers over 55 years old were significantly less likely to have HCSTC loans (12.2%) compared to the UK population within that age group (34.8%). The survey also found that 60% of payday loan borrowers and 45% for short-term installment loans were female, compared with 51% of the UK population being female.

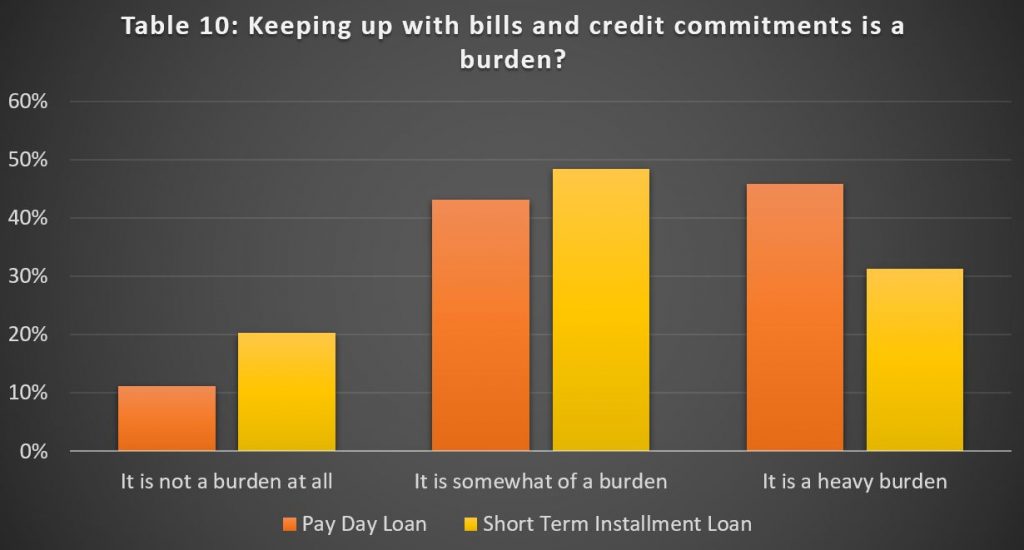

61% of consumers with a payday loan and 41% of borrowers with a short-term installment loan have low confidence in managing their money, compared with 24% of all UK adults. In addition, 56% of consumers with a payday loan and 48% of borrowers with a short-term installment loan rated themselves as having low levels of knowledge about financial matters. These compare with 46% of all UK adults reporting similar levels of knowledge about financial matters.

But now the top PayDay lenders are out of business. In August 2018, Wonga, once the biggest payday lender in the UK collapsed and now administrators for the lender have revealed that 389,621 eligible claims have been made since Wonga’s demise. Despite being vilified for its high-cost, short-term loans, seen as targeting the vulnerable, it became a household name and was enormously successful until stricter regulation curtailed its, and other payday loan companies’, lending.

It collapsed in the UK following a surge in compensation

claims from claims management companies acting on behalf of people who felt

they should never have been given these loans. So far, the compensation bill is

£460m, with the average claim £1,181.

Another lender, The Money shop closed earlier this year.

Now QuickQuid, UK’s largest payday lending firm is to close with thousands of complaints about its lending still unresolved. QuickQuid’s owner, US-based Enova, says it will leave the UK market “due to regulatory uncertainty”.

QuickQuid is one of the brand names of CashEuroNet UK, which

also runs On Stride – a provider of longer-term, larger loans and previously

known as Pounds to Pocket. The UK’s Financial Ombudsman Service said that it

had received 3,165 cases against CashEuroNet in the first half of the year. It

was the second most-complained about company in the banking and credit sector

during that six months.

Back in 2015, CashEuroNet UK LLC, trading as QuickQuid and

Pounds to Pocket, agreed to redress almost 4,000 customers to the tune of £1.7m

after the regulator raised concerns about the firm’s lending criteria.

More than 2,500 customers had their existing loan balance

written off and more almost 460 also received a cash refund. (The regulator had

said at the time that the firm had also made changes to its lending criteria.)

“Over the past several months, we worked with our UK

regulator to agree upon a sustainable solution to the elevated complaints to

the UK Financial Ombudsman, which would enable us to continue providing access

to credit,” said Enova boss David Fisher.

“While we are disappointed that we could not ultimately

find a path forward, the decision to exit the UK market is the right one for

Enova and our shareholders.”

So this could be the twilight of the PayDay industry in the

UK, as better education, and other lending options, plus tighter regulation

bite.

Given the pressures on households here, we are concerned that

more will reach for short term loans to tide them over, despite the high costs

and risks from repeat borrowing, all made easier still via the proliferation of

online portals. The debt burden on households is high and rising.