From The Conversation.

The Australian Taxation Office (ATO) has released data for 2014-15 that paints a picture of how much Australians earn and what they claim in tax concessions. We asked our tax experts to tell us what the data says to them.

John Daley and Danielle Wood, The Grattan Institute

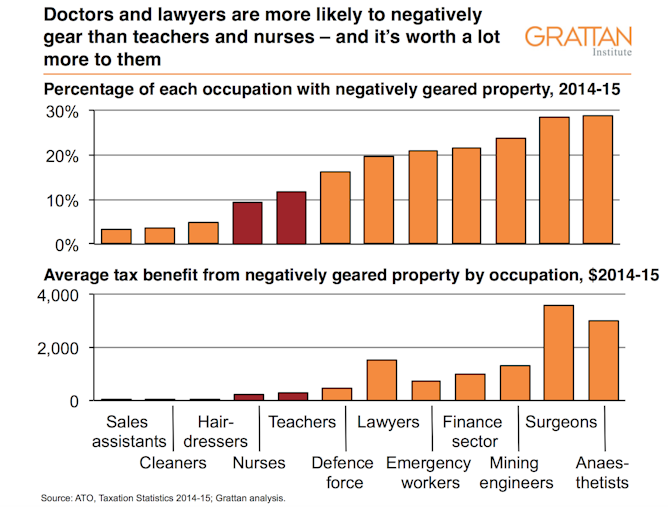

The latest data from the ATO is consistent with what we’ve seen in the past. It shows that people with high-income occupations – doctors, lawyers, and others – are more likely to use negative gearing than the nurses and teachers on whom Treasurer Scott Morrison focuses when he tries to justify retaining negative gearing. It also shows that negative gearing is typically worth four to five times more for doctors and lawyers than nurses and teachers.

Author provided

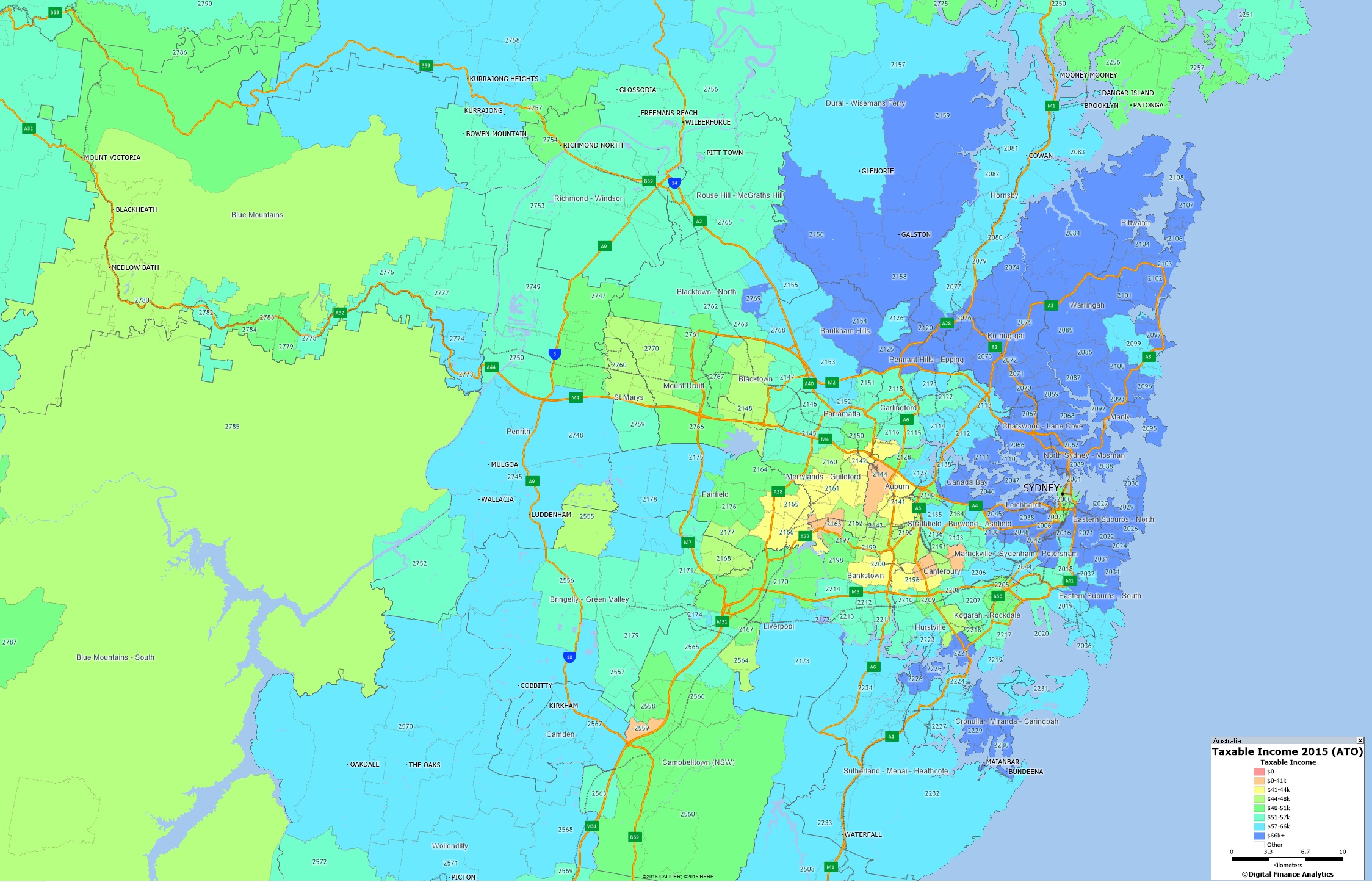

The tax data shows that with falling interest rates, fewer landlords are negatively geared, and the average loss is also falling. Overall the investor property market seems to be concentrating a little, with slightly fewer landlords but more investment properties per landlord.

Author provided

Negative gearing has lots of problems. It costs the budget a lot of money, distorts investment decisions, increases house prices, and reduces home ownership, while doing little to increase supply.

The government claims it should nevertheless be retained because it’s primarily an investment strategy for “mums and dads”. But the detailed tax data from previous years shows that about two-thirds of the benefit goes to the one-fifth of taxpayers with the highest income before the negative gearing deduction.

We will have to wait until later this month for the release of more detailed data to check that this is still true.

Professor Fabrizio Carmignai, Griffith Business School

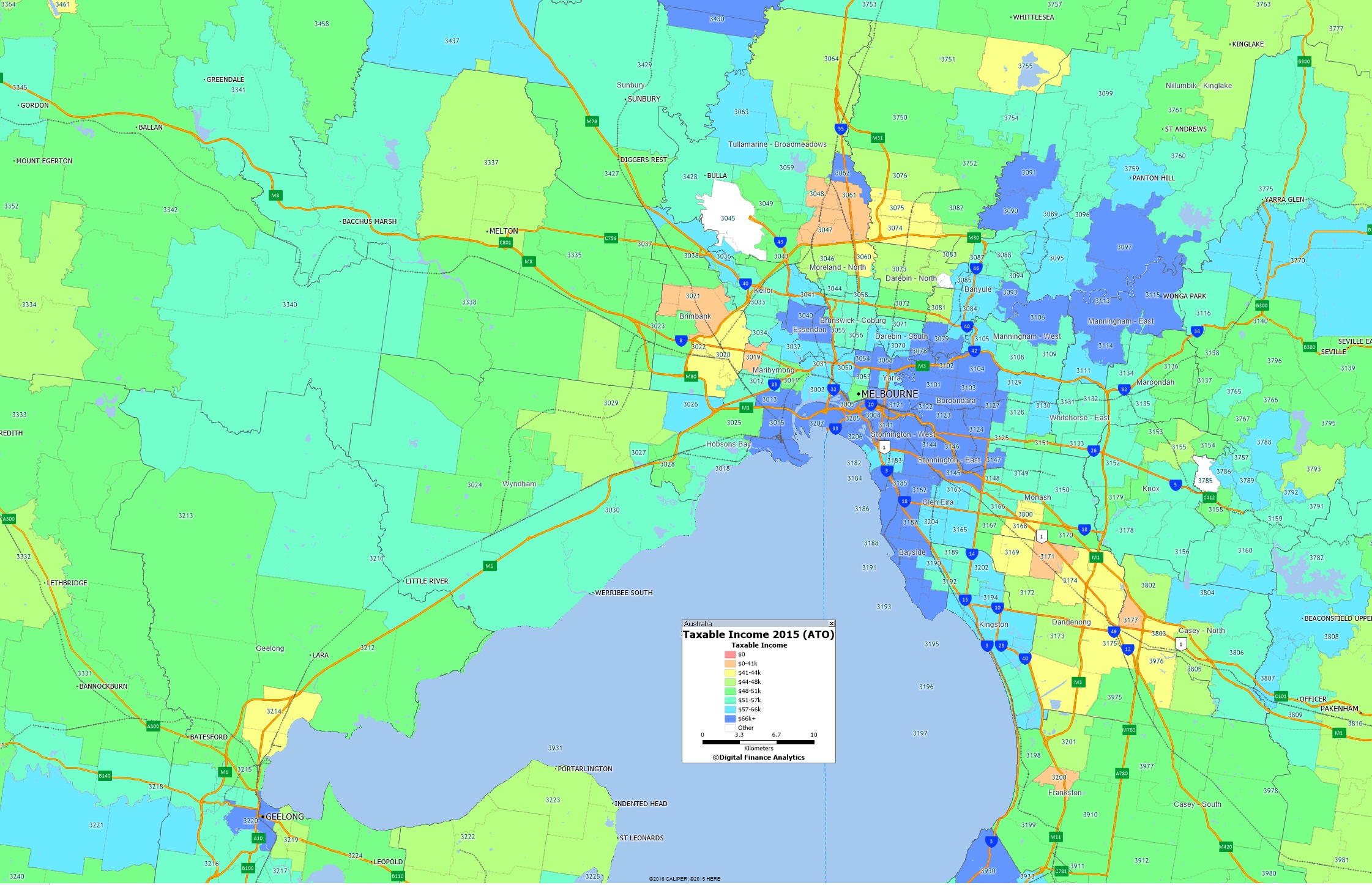

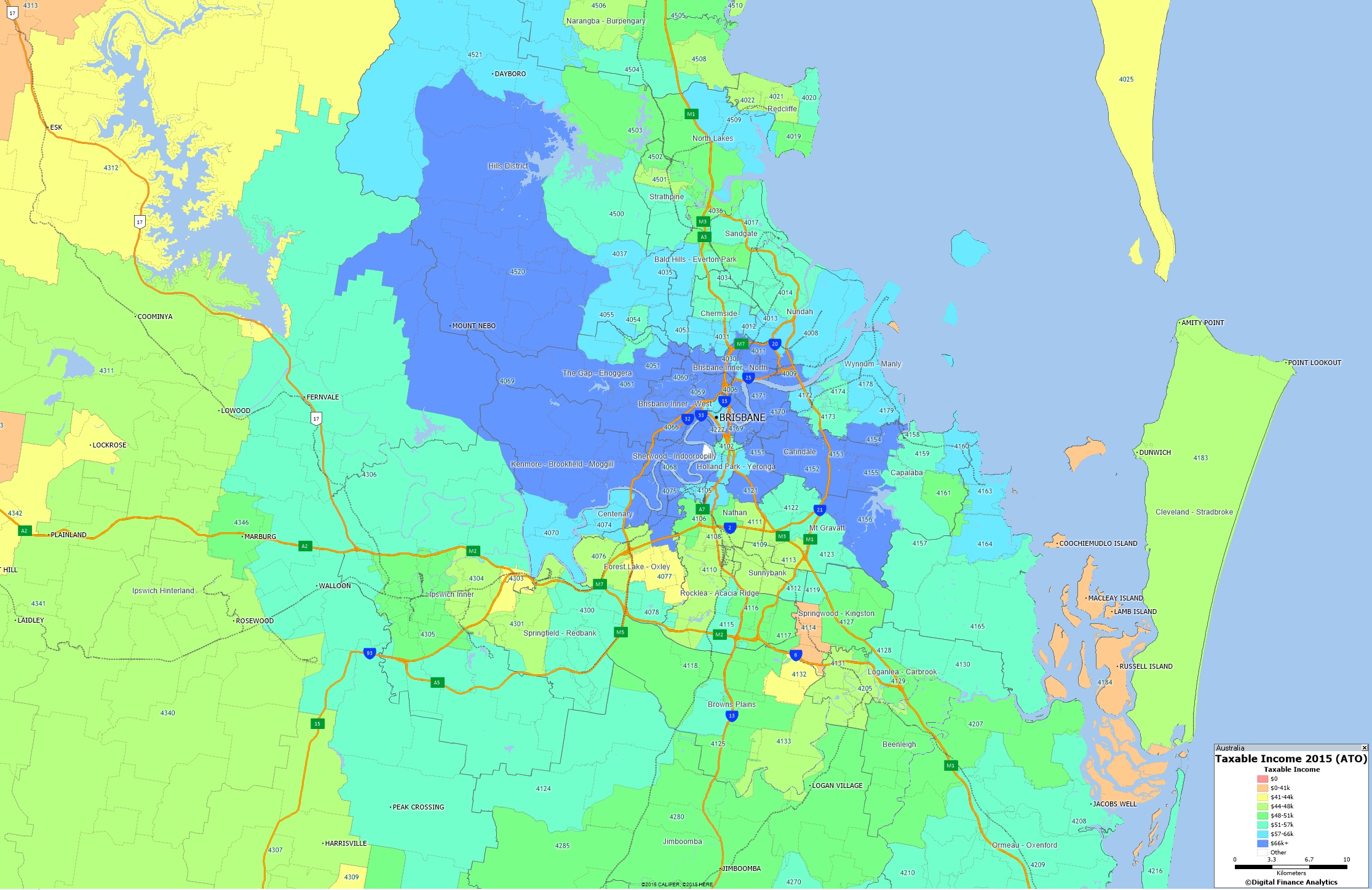

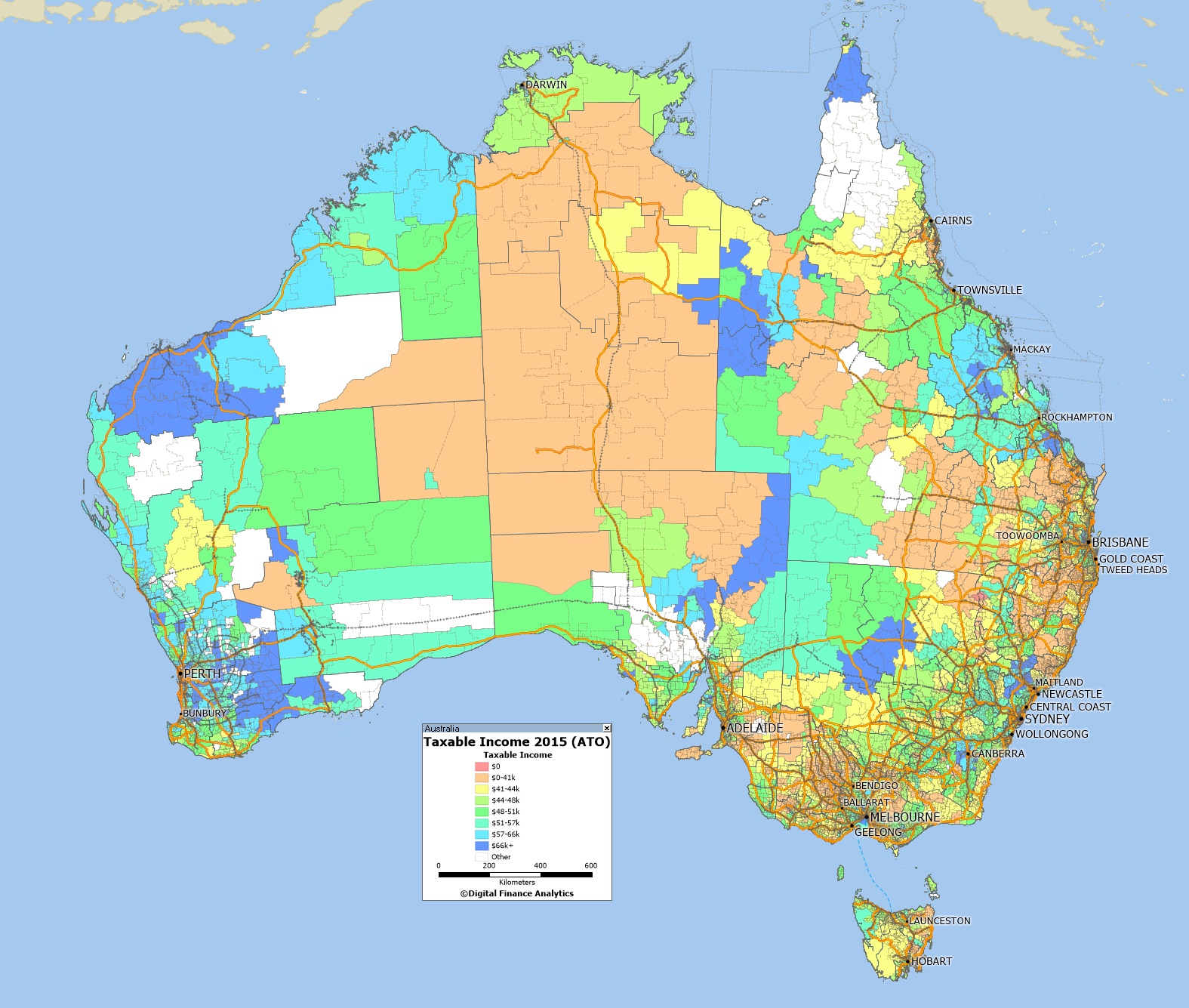

This data delivers a simple, probably not unexpected, but still concerning message: inequality in Australia is increasing.

We can see this in terms of the growing gap between the richest and the poorest suburbs, as well as an increase in dispersion across all suburbs.

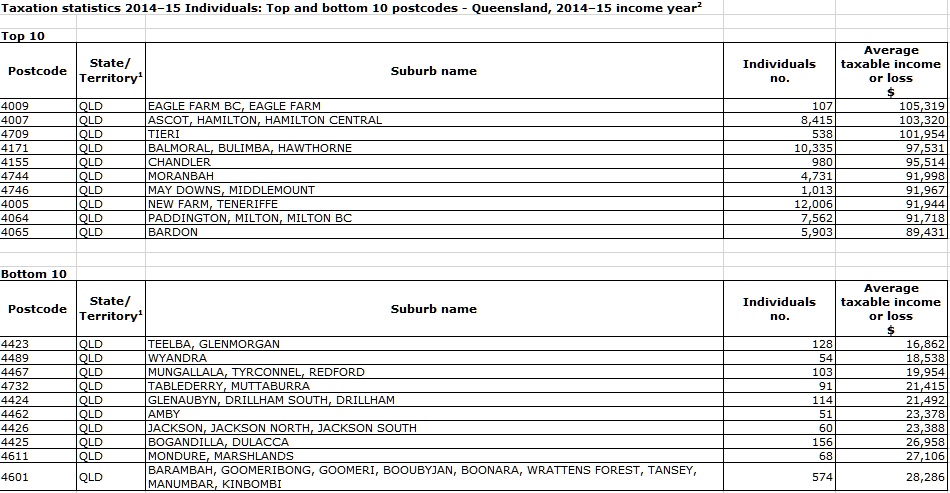

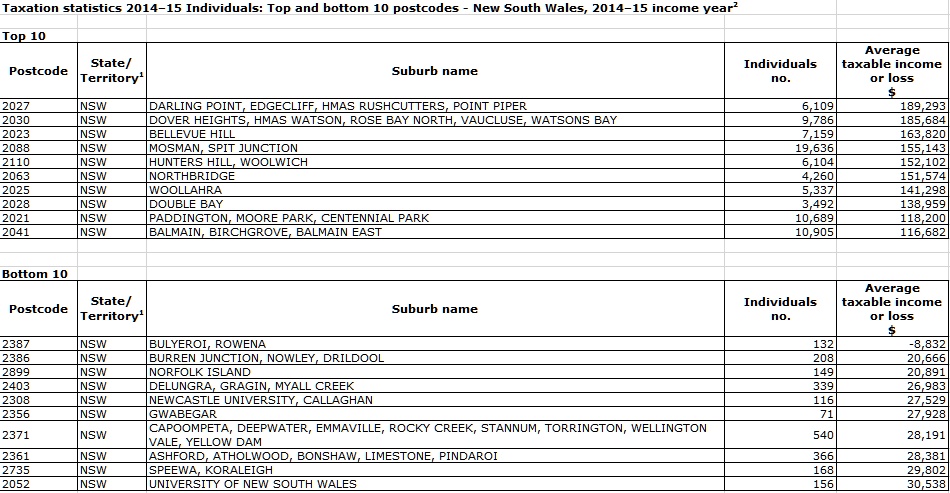

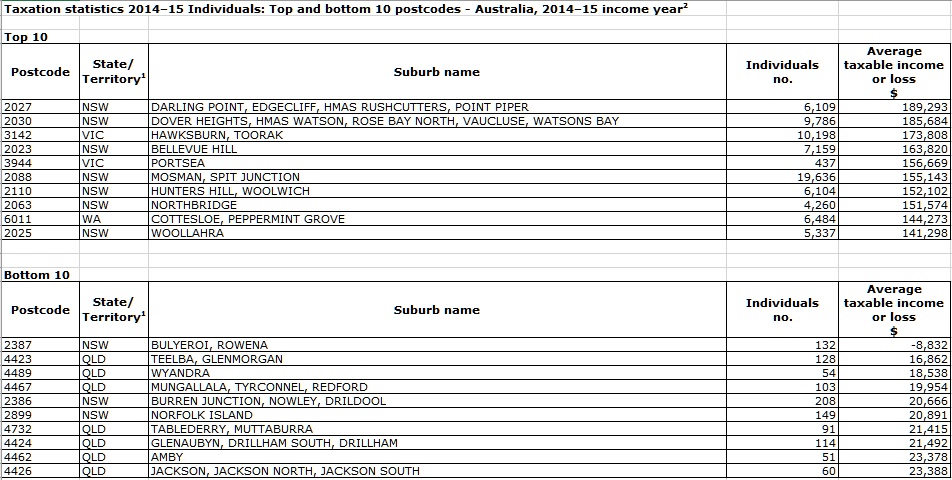

For example, the data published yesterday indicates that average taxable income in the ten poorest postcodes was only 11% of the average taxable income in the ten richest postcodes. A decade ago, in 2004-05, income in the ten poorest postcodes was 21% of income in the richest postcodes.

In fact, while the average income at the top of the distribution has grown by 30% in a decade, average income at the bottom has actually declined by 33%. If we look at the overall dispersion of incomes by postcode, we can see that this has gone up by approximately 25% in ten years.

Whichever way we look at it, the conclusion is that there is more income inequality today than ten years ago.

The other interesting aspect to the data is that the richest postcodes today are more or less the same as ten years ago. Indeed, seven of the top ten postcodes in 2014-15 were already in the top ten in 2004-05. But this same trend is not observed at the bottom: none of the ten poorest postcodes today were in bottom ten in 2004-05.

And there is some bad news for Queensland in particular: the proportion of the state’s postcodes in the bottom ten has increased considerably, from three out of ten in 2004-05 to seven out of ten in the latest data. This data might be indicative of a growing poverty problem in this state.

Associate Professor Helen Hodgson, Curtin Law School

The ATO’s data clearly shows that the self-managed superannuation fund (SMSF) sector is not only continuing to grow, but is used primarily by people with the ability to make higher contributions; either high income earners or those late in their careers.

Members of self-managed superannuation funds made significantly higher contributions and have higher balances than members of Australian Prudential Regulatory Authority (APRA) regulated funds.

The data shows that on an individual basis, the median contribution to a SMSF was A$20,000. Meanwhile, members of APRA funds made median contributions of A$4,507.

Similarly, the super balances of members of SMSFs are significantly higher than APRA funds. SMSF members have median balances of A$289,483, compared to just A$32,734 for those in APRA regulated funds. The data also shows that a small proportion of people have very high balances, which is reflected in the difference between the median and mean balances in the statistics.

Two of the forthcoming changes to superannuation will limit contributions and impose a cap on balances, which should impact higher earners. Most people who made contributions in excess of A$25,000 are over 45 and earned more than A$180,000.

But the changes to the superannuation system will not take effect until July 2017, so it is too soon to know how that will impact superannuation funds. However the division between the self-managed and APRA regulated funds is clear.

Authors:Jenni Henderson, Editor, Business and Economy, The Conversation; Josh Nicholas, Deputy Editor Business & Economy, The Conversation; Interviewed: Danielle Wood, Fellow, Australian Perspectives, Grattan Institute; Fabrizio Carmignani, Professor, Griffith Business School, Griffith University; Helen Hodgson, Associate Professor, Curtin Law School and Curtin Business School, Curtin University; John Daley, Chief Executive Officer, Grattan Institute.

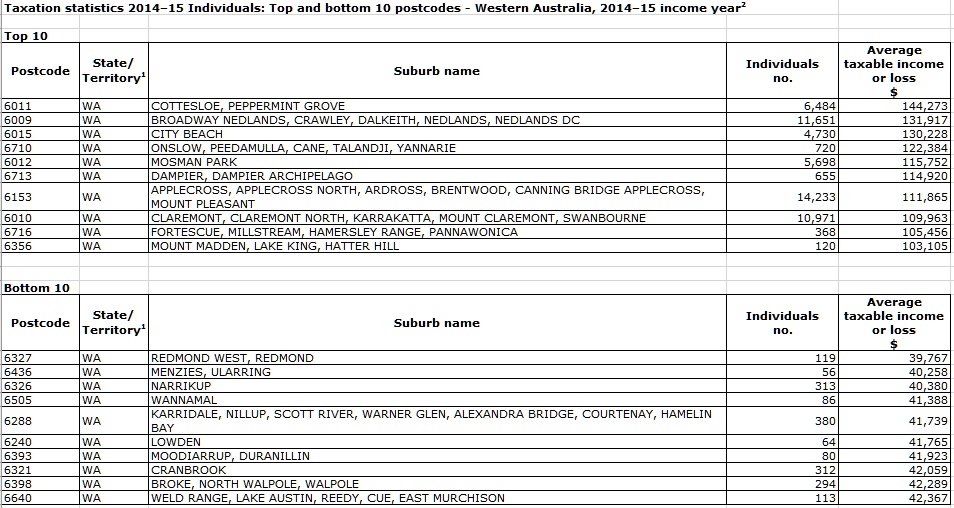

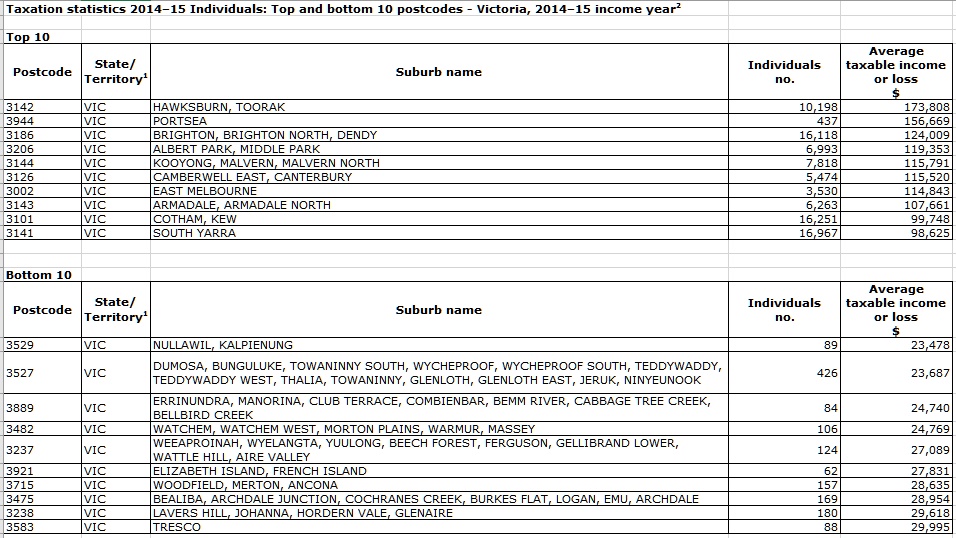

Here are the top and bottom 10 across WA.

Here are the top and bottom 10 across WA.