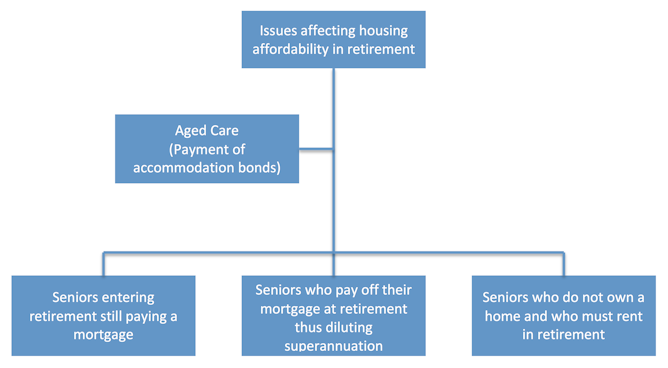

A recent report raised concerns about the erosion of retirement income by ongoing rental or mortgage payments.

The report by the Australian Institute of Superannuation Trustees is timely, given the Australian aged pension system is predicated on an assumption of outright home-ownership. Yet increasing numbers of people are still paying mortgages after retirement, use superannuation to pay off mortgage debt, or do not own a home and must rent.

Any significant decline in home ownership or equity in a home also has impacts on higher care needs. This is because older people will not have an asset to sell to fund the bonds required to enter aged care accommodation.

Author provided

These developments – and the increasing housing insecurity for older people – potentially undermine the sustainability of Australia’s retirement system and, in turn, public finances.

Addressing the problem

Social impact investment strategies could fund more affordable housing and aged care for seniors.

Social impact investments are:

… investments made into organisations, projects or funds with the intention of generating measurable social and environmental outcomes, alongside a financial return.

Impact investment in Australia may take a variety of different forms. It can be organised through direct equity investment, acquisition of units in a mutual fund, debt, venture capital, social impact bonds or other fixed income mechanisms, which might combine blended social impact and financial return.

The sources of investment are equally diverse. These may include philanthropists, funds, businesses, government, private investors, or a combination of two or more.

In Australia, social impact investing is a relatively recent phenomenon although it is developing rapidly in a variety of areas. Impact investing in Australia will be worth $A33 billion by 2022 and extends to a diverse range of investments.

In relation to housing support, examples include the Aspire Social Impact Bond, which targets people experiencing long-term homelessness, and Homeground, a not-for-profit real estate service.

In relation to housing developments, projects such as the innovative CapitalAsset partnerships instigated by ShelterSA. The project aims to collaborate with developers, landowners and investors to build affordable housing developments through a property unit trust.

Housing is likely to be a focus area of social impact investment partnerships between Social Ventures Australia and organisations such as HESTA and Macquarie.

Financing is the key to increasing stocks of affordable housing. It seems the federal government is likely to institute a bond aggregator model involving institutional investors and affordable housing providers.

Retirement housing issues have not been a focus for social impact investing in Australia or elsewhere. However, it is suggested this form of investing could tackle the problems outlined in the Australian Institute of Superannuation Trustees report in three ways.

(Almost) home owners

For those who must maintain a mortgage into retirement, or who want to avoid using most of their superannuation funds to pay off the mortgage, thought could be given to offering lower-cost loans or products akin to reverse mortgages at lower than commercial rates.

Alternatively, under a shared equity arrangement – where reduced payments are made until the sale of the property or the death of the owner/s – the property could be sold and the sale price shared by the older person to put towards care or the estate and the lender.

Social impact investment lenders could finance this in the same way as banks do but at reduced rates. There would still be a healthy return, and older people could live better in retirement with reduced payments but secure in the knowledge they do not have to leave or lose their home.

Regarding the older people who rent, again social impact investing could focus on ensuring that any housing projects developed have a certain percentage of the accommodation available for older people.

Models proposed for social impact investing in affordable housing could be applied to ensure this accommodation is suitable for older people.

Wrap-around services

In both cases, the financing models could be supported by social impact investing provided for support services.

For example, wrap-around services, such as those provided in the Newquay project in Britain, aim to keep older people in their homes and out of hospitals and aged care.

If housing costs are a problem for people in retirement, that’s also going to hamper their ability to pay for care. shutterstock

If housing costs are a problem for people in retirement, that’s also going to hamper their ability to pay for care. shutterstock

Ripe for repair

Social impact investing could mobilise private capital to work with not-for-profits to attract investment funds. Grace Mutual has mooted such a project in Australia.

Furthermore, social impact investments could work in areas, such as rural and regional Australia, that are traditionally left to government because of low population and problems with profitability and economies of scale.

Sabina Lim recently suggested the services gap in health and aged care is ripe for social impact investing in Australia.

It’s time to bridge the gaps

Governments alone cannot bridge the gaps and support affordable housing for seniors.

Although government will certainly continue to play a significant role, impact investment should be encouraged as a way to resolve financing and development issues in meeting seniors’ needs for accommodation and care.

Such involvement can be fostered through partnerships between government, NGOs and private investors, together with taxation and other financial incentives. Legal, policy and planning impediments to financing and investment in seniors housing also need to be removed.

Importantly, we need other players in the market who are prepared to invest in affordable housing and aged care for Australians in retirement.

Authors: Eileen Webb, Associate Professor, Curtin Law School, Curtin University; Gill North, Professorial Research Fellow, Deakin University; Richard Heaney, Professor of Finance, University of Western Australia.

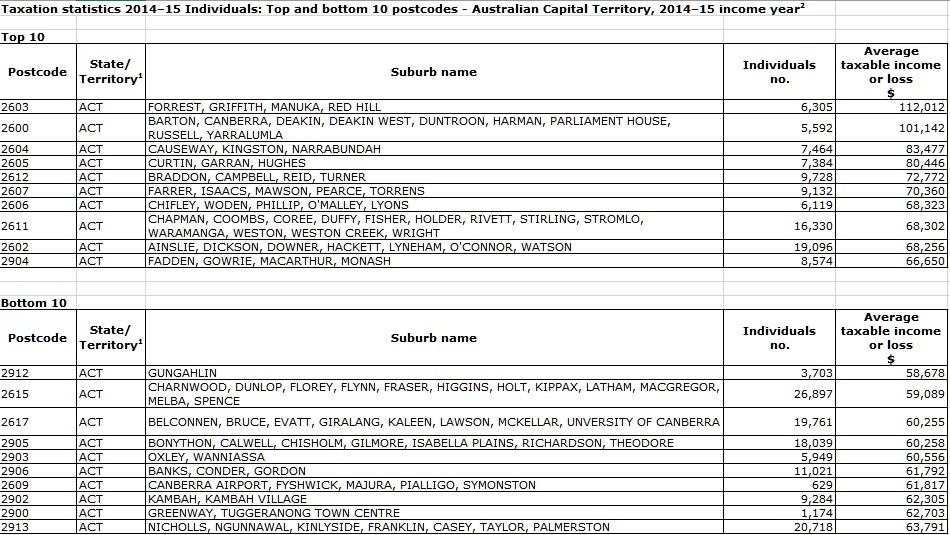

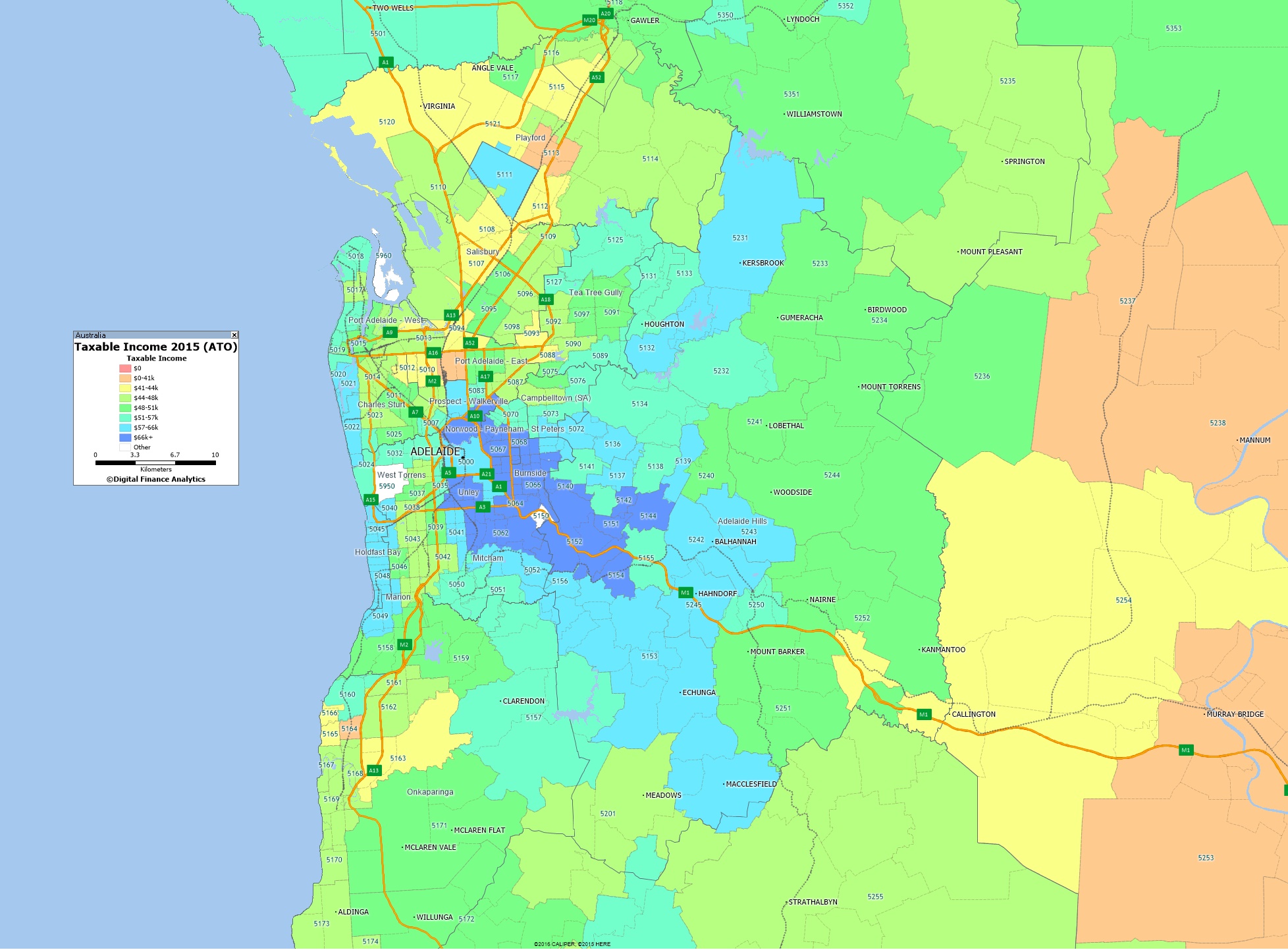

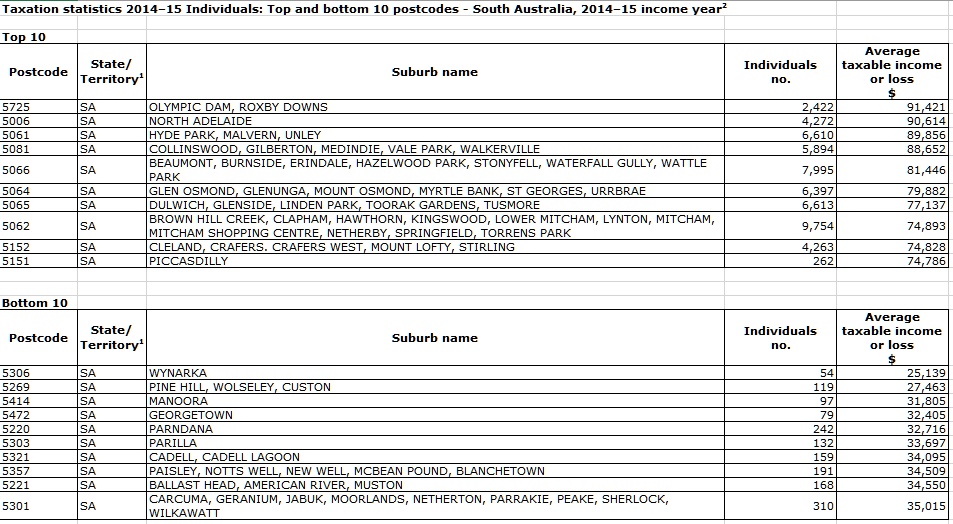

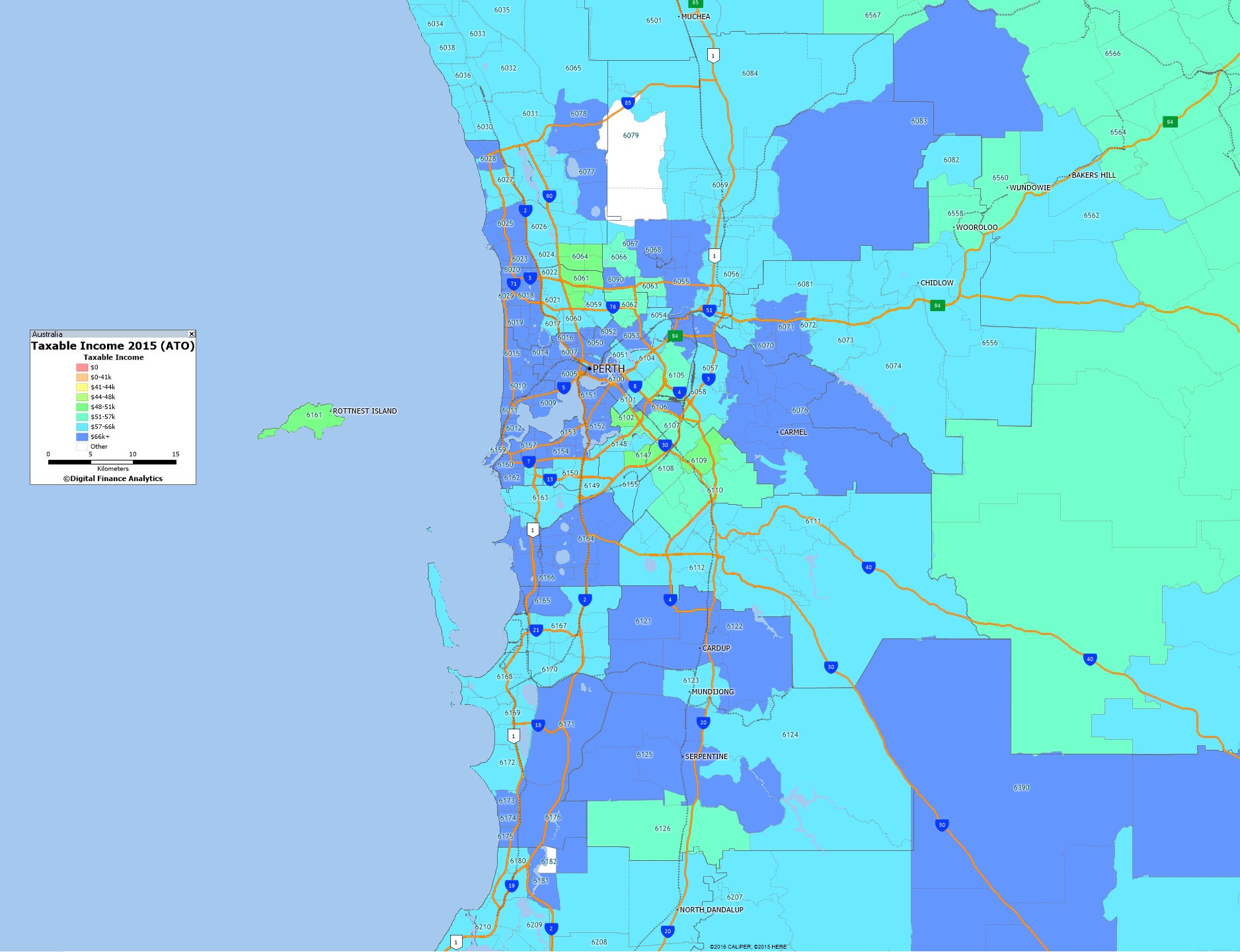

Here are the top and bottom 10 across the ACT.

Here are the top and bottom 10 across the ACT.