Last Tuesday, low-cost fund provider Vanguard (unrated), announced its intention to enter the UK’s direct-to-consumer online investment market. Vanguard’s entry into the UK retail online investment market is credit negative for incumbent online platforms such as Hargreaves Lansdown (unrated) and FIL Ltd.’s (Baa1 stable) Fidelity FundsNetwork because it will likely trigger a price war that costs incumbents their profitability.

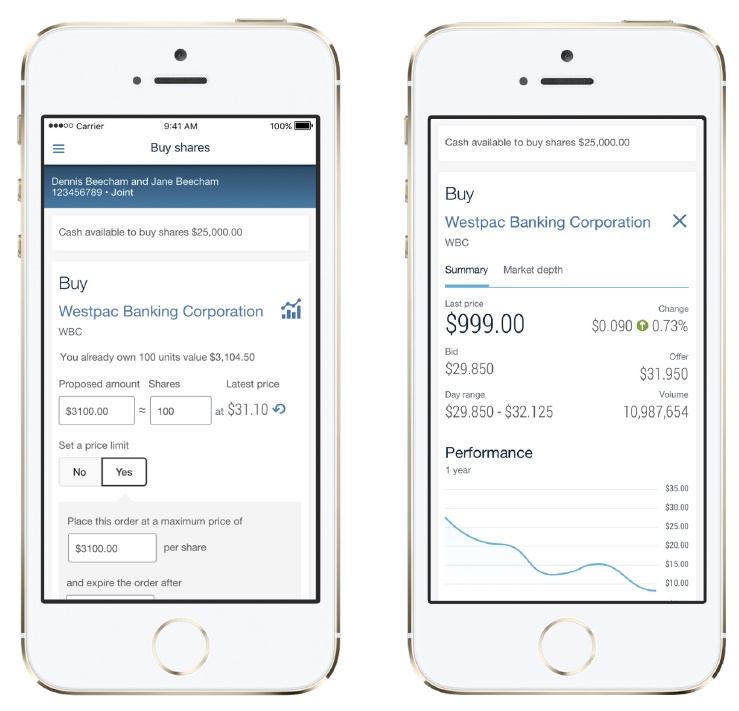

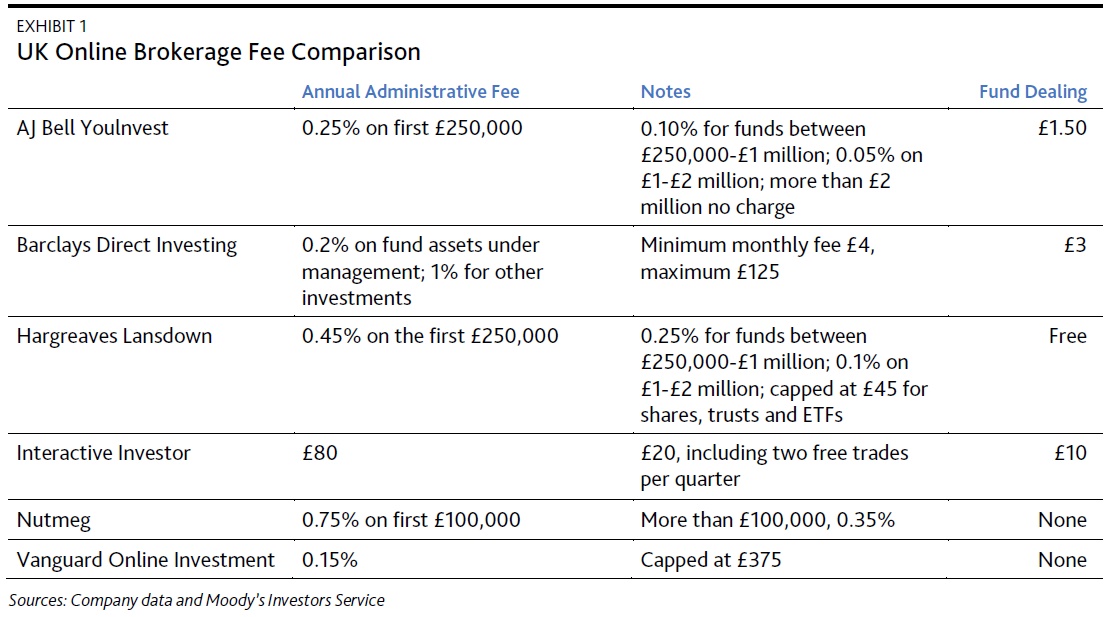

Vanguard’s online service, the Vanguardinvestor, lets UK retail investors directly access a wide range of Vanguard’s exchange-traded funds (ETFs) without using a broker or financial advisor. So far, most of Vanguard’s UK business has been sourced from brokerages and financial advisors, which typically require clients to have minimum account balances of at least £100,000. Using Vanguard’s online platform, retail investors will now be able to open an individual savings account with £500 or a monthly investment of £100. And, Vanguardinvestor will charge a flat administrative fee of 0.15% (capped at £375 per year), which is lower than the 0.45% fee that Hargreaves Lansdown, the UK’s largest online provider, charges (see Exhibit 1).

Vanguard will target investors from both the mass and mass-affluent markets – those with savings of £5,000-£50,000. These investors lost access to advice in 2013 with implementation of the UK’s Retail Distribution Review (RDR) and invest directly. In a November 2012 publication, Deloitte estimated that the RDR had created an advice gap population of as many as 5.5 million people.

Vanguard will target investors from both the mass and mass-affluent markets – those with savings of £5,000-£50,000. These investors lost access to advice in 2013 with implementation of the UK’s Retail Distribution Review (RDR) and invest directly. In a November 2012 publication, Deloitte estimated that the RDR had created an advice gap population of as many as 5.5 million people.

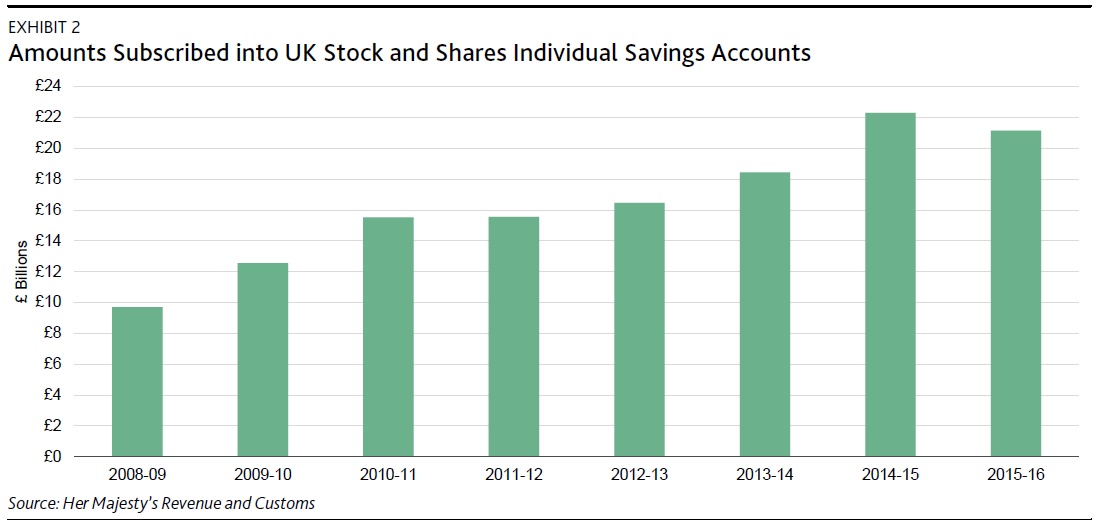

Gross inflows into stock and share individual savings accounts in 2015-16 totalled £21.1 billion, and this segment has been growing (see Exhibit 2), driven by the tax-free individual savings account allowance increase to £20,000 from £15,240 in April 2017 and new products. In addition to individual savings accounts and defined-contribution pensions, general investment accounts without any tax wrapper are benefiting from investor inflows as people become increasingly aware of their investment options. Vanguard announced plans to launch a self-invested personal pension in the future.

Vanguard’s online service also targets younger investors such as millennials, who are comfortable with online services and are not yet a target for financial advisors or wealth managers. As they evolve in their careers and garner higher incomes, this demographic will be accustomed to low-cost services and investment funds. Vanguard’s online service in the UK is so far limited, but we can see it evolving toward robo-advice as it has in the US with The Vanguard’s Personal Advisor Services.

Vanguard’s online service also targets younger investors such as millennials, who are comfortable with online services and are not yet a target for financial advisors or wealth managers. As they evolve in their careers and garner higher incomes, this demographic will be accustomed to low-cost services and investment funds. Vanguard’s online service in the UK is so far limited, but we can see it evolving toward robo-advice as it has in the US with The Vanguard’s Personal Advisor Services.

Incumbent platform providers will likely lower administrative fees and increase services to maintain market share, but this will compress their margins. Given the high and rising costs of running online services, smaller platforms with less price flexibility such as Interactive Investors (unrated) and Nutmeg (unrated) will be most challenged. Cheap online investment services will also accelerate the adoption of low-costs index trackers and ETFs among UK retail investors. Active managers such as Aberdeen, Henderson, Schroders, and FIL Ltd. Will face fee and margin pressure as a result.

In addition, the UK’s Financial Conduct Authority’s upcoming investment platform market study to improve competition between platforms and improve investor outcomes is likely to challenge most platform providers’ prices and Vanguard would be well positioned for any price war. As the best-selling fund manager in 2016 and second-largest asset manager globally, Vanguard has the scale, resources and brand necessary to disrupt the UK retail market, which was £872 billion as of year-end 2015. In the US, where Vanguard provides a similar online-value proposition, platform costs went down.