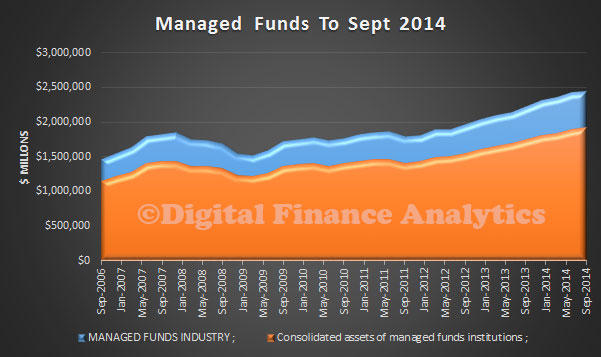

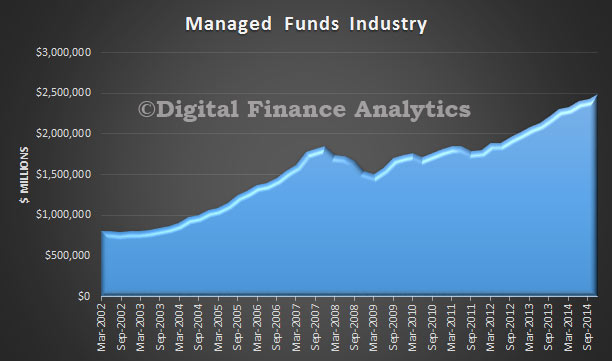

ABS released their funds management data to December 2014. The managed funds industry had $2,489.9b funds under management (including some changes to the data capture and revisions), an increase of $57.6b (2%) on the September quarter 2014 figure of $2,432.3b. The main valuation effects that occurred during the December quarter 2014 were:

- the S&P/ASX 200 increased 2.2%

- the price of foreign shares, as represented by the MSCI World Index excluding Australia, increased 0.8%

- A$ depreciated 6.7% against the US$.

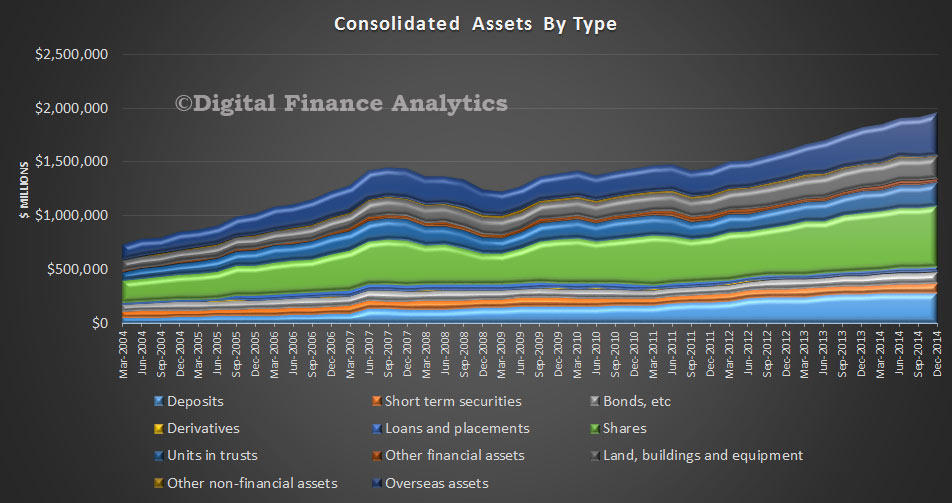

At 31 December 2014, the consolidated assets of managed funds institutions were $1,958.5b, an increase of $48.8b (3%) on the September quarter 2014 figure of $1,909.7b. The asset types that increased were:

At 31 December 2014, the consolidated assets of managed funds institutions were $1,958.5b, an increase of $48.8b (3%) on the September quarter 2014 figure of $1,909.7b. The asset types that increased were:

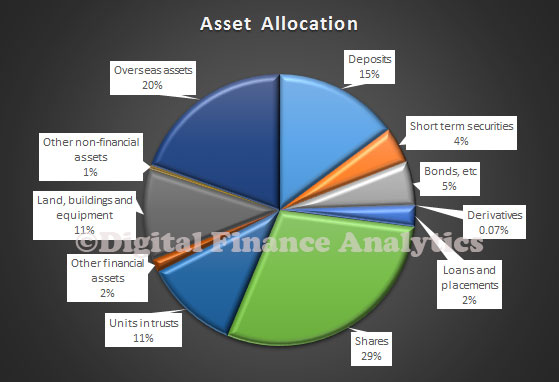

- overseas assets, $29.6b (8%)

- shares, $14.6b (3%)

- short term securities, $8.6b (10%)

- bonds, etc., $4.3b (4%)

- derivatives, $0.8b (65%)

- other non-financial assets, $0.2b (2%).

These were partially offset by decreases in:

- other financial assets, $3.4b (11%)

- deposits, $3.2b (1%)

- land, buildings and equipment, $1.5b (1%)

- loans and placements, $1.0b (2%)

- and units in trusts, $0.2b (0%).

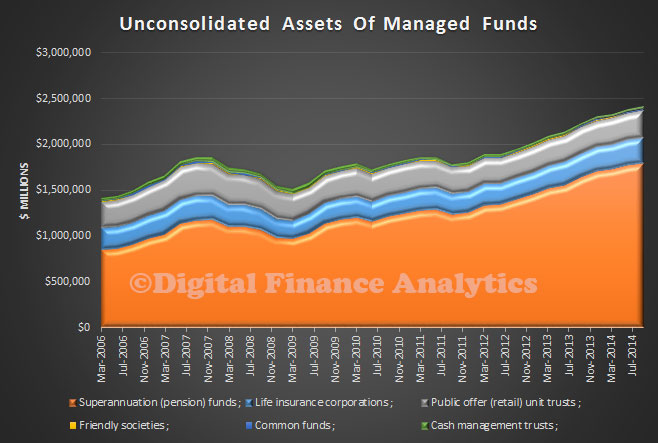

At 31 December 2014, there were $503.9b of assets cross invested between managed funds institutions whilst the unconsolidated assets of superannuation (pension) funds increased $54.4b (3%), public offer (retail) unit trusts increased $4.5b (2%), life insurance corporations increased $4.3b (2%), cash management trusts increased $0.8b (3%), and common funds increased $0.2b (2%). Friendly societies were flat.

At 31 December 2014, there were $503.9b of assets cross invested between managed funds institutions whilst the unconsolidated assets of superannuation (pension) funds increased $54.4b (3%), public offer (retail) unit trusts increased $4.5b (2%), life insurance corporations increased $4.3b (2%), cash management trusts increased $0.8b (3%), and common funds increased $0.2b (2%). Friendly societies were flat.