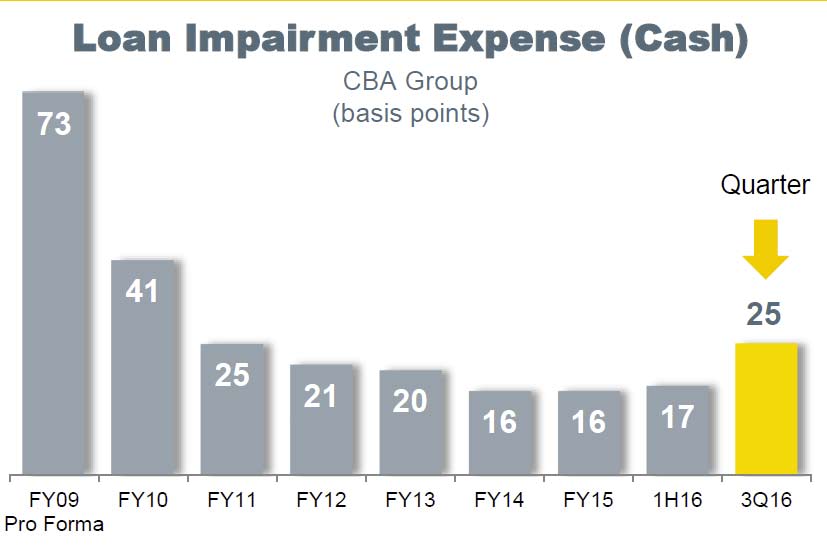

CBA has released its unaudited cash earnings for 3 months to 31st March 2016 of $2.3 billion and a statutory net profit on an unaudited basis of $2.4 billion. They reported that income growth and net interest margin was similar to 1H16. Costs were higher. Wealth Management funds under management fell, reflecting falling investment markets. Loan impairment expense was higher at $427m or 25 basis points, reflecting exposures in the institutional lending portfolio and consumer losses. Total provisions were higher at $3.9 billion.

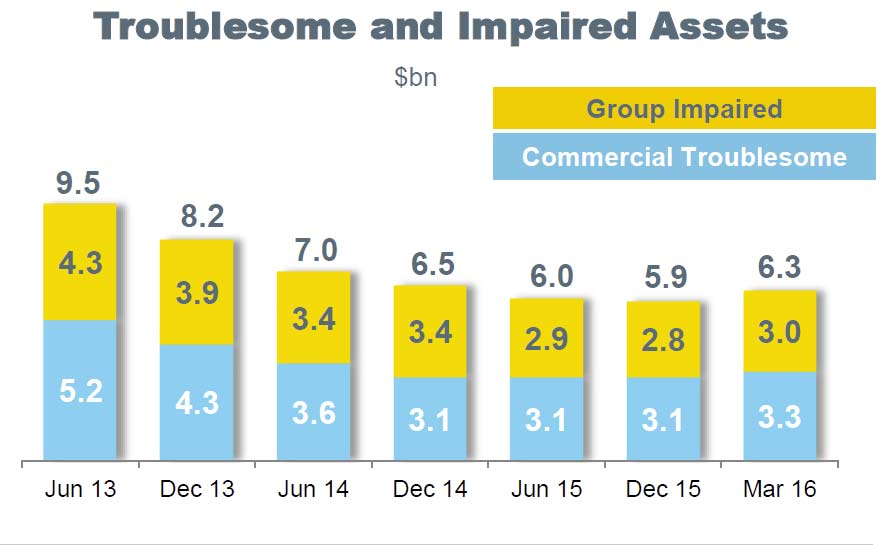

Group Troublesome and Impaired Assets was also up, at $6.3 billion.

Group Troublesome and Impaired Assets was also up, at $6.3 billion.

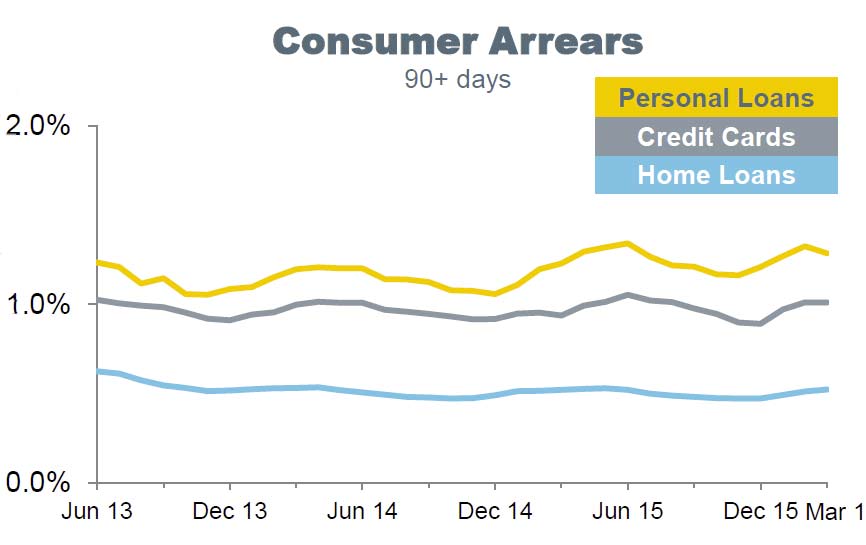

Consumer arrears were in line with expectations, despite higher home loan arrears in mining impacted areas of WA and QLD.

Consumer arrears were in line with expectations, despite higher home loan arrears in mining impacted areas of WA and QLD.

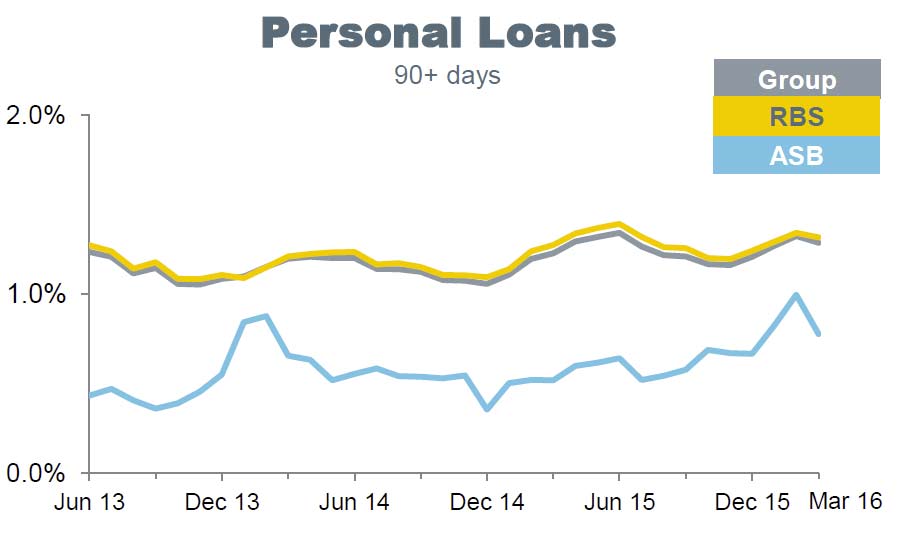

Personal loan arrears remained elevated.

Personal loan arrears remained elevated.

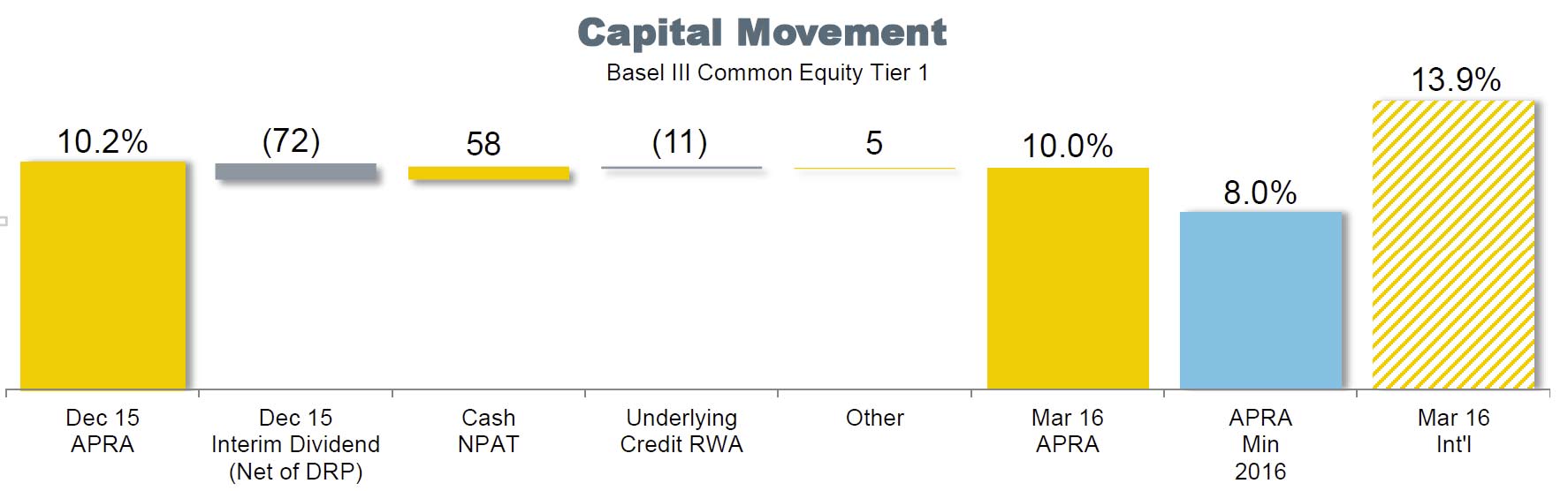

The Group’s Basel III CET1 APRA ratio was 10%, down from 10.2% in Dec 15. Comparable CET1 ratio at 31 March 2016 was 13.9%. The Group’s leverage ratio was 4.9% on an APRA basis and 5.5% on an international comparable basis.

The Group’s Basel III CET1 APRA ratio was 10%, down from 10.2% in Dec 15. Comparable CET1 ratio at 31 March 2016 was 13.9%. The Group’s leverage ratio was 4.9% on an APRA basis and 5.5% on an international comparable basis.

Customer deposits comprised 64% of funding (reflecting above system deposit growth) and the average tenor of wholesale funding was 4.2 years. The Group issues $13 billion of long term funding in the quarter.

Customer deposits comprised 64% of funding (reflecting above system deposit growth) and the average tenor of wholesale funding was 4.2 years. The Group issues $13 billion of long term funding in the quarter.