From The Burning Platform Blog.

It is fascinating to me no one seems all that worried about the systematically dangerous levels of global debt supporting essentially bankrupt governments, banks and consumers. Global debt stood at $142 trillion at the end of 2007, just prior to a worldwide financial meltdown, caused by too much bad debt in the financial system.

To “fix” this problem, central bankers around the globe ramped up their electronic printing presses to hyper-drive and created another $57 trillion of debt by mid-2014. They haven’t taken their foot off the gas since. Today, global debt most certainly exceeds $225 trillion and has surpassed 300% of global GDP. Rogoff and Reinhart made a pretty strong case that when debt to GDP exceeds 90%, disaster will follow.

Global debt issuance reached a record $6.6 trillion in 2016, with corporations accounting for $3.6 trillion – most of which was used to buy back their stock at all-time highs. What could possibly go wrong? The level of normalcy bias amongst financial “experts”, the intelligentsia, and the common man is breathtaking to behold. We are in the midst of the mother of all bubbles, never witnessed in the history of mankind, and we pretend everything is normal, with no consequences for our reckless disregard for honesty, rational thinking, or simple math.

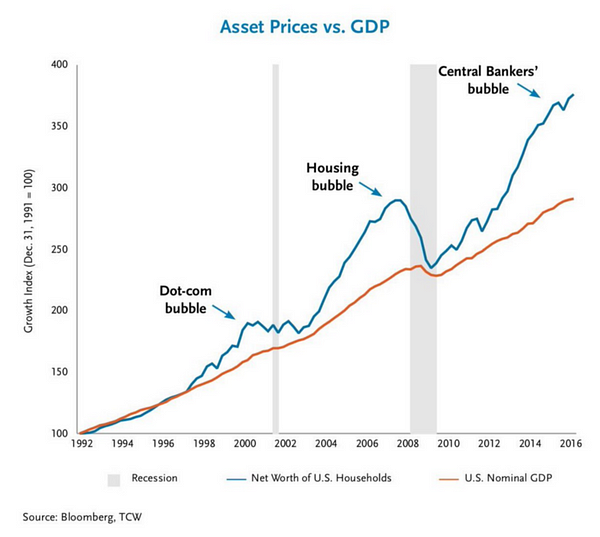

The 2000 dot.com bubble and the 2008 housing bubble were one dimensional. This mother of all bubbles required the global coordination and unprecedented irresponsible intervention of the US Federal Reserve, the European Central Bank (ECB), the Bank of Japan (BOJ), the Bank of England (BOE) and the Swiss National Bank (SNB) to lead the world to the brink of monetary disaster. The highly educated theorists running these central banks have created tens of trillions in unpayable debt while suppressing interest rates to zero or below at the behest of their Deep State masters.

The result is simultaneous bubbles in stocks, bonds and real estate. The pin destined to pop all the bubbles is slightly higher interest rates. The 1% increase in the 10 Year Treasury is already causing havoc in the housing market, the bond market and is hammering pension funds. With the hundreds of trillions in globally interconnected derivatives primed to detonate, 2017 could be an explosive year.

Here are a few things I think could happen in 2017 on the [US] economic front:

- The national debt stands at $19.9 trillion and will reach $20 trillion before Obama departs. With spending on automatic pilot and tax revenue in decline, the national debt will reach $21 trillion in 2017. With most of the debt financed short-term, the increase in rates will ratchet the interest on the debt from $433 billion to over $550 billion.

- With the CPI increasing by over 3% in the first few months of the year, the Fed will continue to raise rates, and the 10 Year Treasury will breach the 3% level.

- Home prices have surpassed the 2006 peak, even though existing home sales are still 20% below 2006 levels and housing starts are 50% below 2006 levels. The entire “recovery” has been engineered by the Fed and Wall Street at the high end of the market. With mortgage rates up 1% already, the further increase will result in existing home sales and housing starts falling by 20% in 2017 and home prices falling by 5% to 10%.

- The short-term OPEC agreement will allow oil prices to move back to $60 per barrel, further eating into consumer discretionary spending. Desperate fracking companies needing cash flow to service their debt will ramp up. Bankrupt or near bankrupt countries like Venezuela, Mexico, and Iran will also increase production. With a slowing global economy and surging supply, prices will collapse again into the $40s in the second half of the year.

- Holiday sales for the bricks and mortar retailers will be reported in January as lukewarm at best. By February, the store closing announcements will reach into the hundreds. Sears will finally declare bankruptcy and shutter at least 50% of their stores. Mall developers will begin to declare bankruptcy as vacancies and rising interest rates create a perfect storm.

- Consumer debt will reach the previous high of $1 trillion, as subprime student loan and auto debt continues to accumulate at an astounding pace. The spigot for student loans is likely to be tightened under Trump, with over 25% of the loans effectively in default. Auto sales (if you can call six year financing and 40% leases, sales) peaked in 2016. Millions of auto buyers are underwater on their loans, subprime auto loans are going into default quicker than you can say Cadillac Escalade, and higher interest rates will price out more potential suckers.

- The faux jobs recovery is running out of steam. With non-existent wage growth, surging costs for rent, health care, energy, and credit cards tapped out, American families will hunker down and reduce spending further. With consumer spending accounting for 68% of GDP, this will lead to an official recession by the middle of 2017.

- All the recent surveys showing consumer confidence soaring and optimism for 2017 are based on nothing but hope. The promises of a Trump administration will not come to fruition until 2018 at the earliest. He will meet resistance from Democrats across the board and resistance amongst his own party. His grand plans for massive tax cuts and spending increases will run into the reality of $1 trillion annual deficits. As reality sets in, and recession arrives, the unwarranted optimism will fade rapidly. Tax cuts will be tempered by reduced spending plans.

- The USD hitting fourteen year highs against the basket of worldwide currencies does not bode well for bringing manufacturing jobs back to make America great again. The reason for the strong dollar is because we are the best looking horse in the glue factory. With Europe and Japan promoting negative interest rates and the Fed slowly raising rates, the dollar will continue to rise. This will hurt our manufacturing businesses, increase our $500 billion annual trade deficit further, and depress the profits of our global corporations.

With rising inflation, rising interest rates, stagnant wages, falling corporate profits, stock valuations at all-time highs, and corporations no longer able to finance stock buy backs at no cost, the stock market will finally hit the wall after a seven year bull market. This last surge of euphoria, based on nothing but Trumpmania sweeping Wall Street, will constitute the final blow-off. The market is currently valued to provide nominal returns of less than 1% over the next twelve years and is likely to experience an abrupt sell-off of 50% in the near future. I believe the near future will be 2017. I think the powers that be will be testing Trump’s mettle in his first year to see if he’ll play ball and do their bidding.