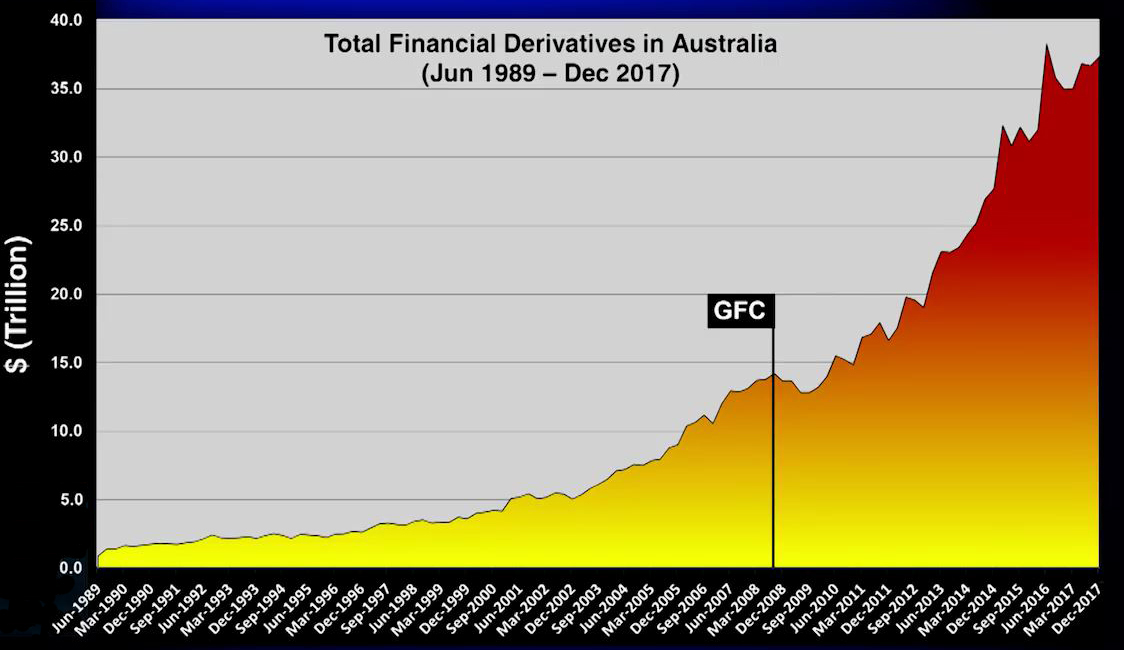

There is a chart doing the rounds courtesy for the CEC (an Australian Political Party, who is advocating the introduction of a Glass Steagall banking separation bill, and which is likely to tabled late June) which shows that the total value of financial derivatives in Australia is around $37 trillion dollars.

I have had a number of people ask about this data, which is not attributed. What does it show, and is it right?

I have had a number of people ask about this data, which is not attributed. What does it show, and is it right?

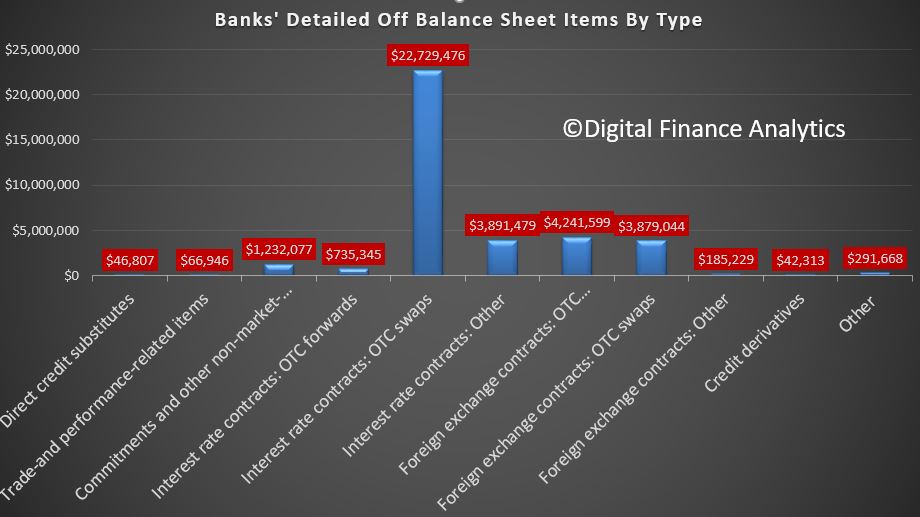

Well the short answer is easy. Derivatives are used quite extensively by many sectors of the Australian economy. The data comes from the RBA series B2 BANKS – OFF-BALANCE SHEET BUSINESS. This lists out Banks’ off-balance balances by category. The major component relates to interest rate derivatives, mainly over the counter (OTC) – meaning they are not exchange based transactions, but are bespoke hedges, either for their customers or trading on their own behalf with other banks, or both. Thus they may be speculative in nature, as traders are taking positions in the market. Over the years the treasury operations of banks have become a profit centre in their own right!

The RBA data shows the range of products, but the largest by far relate to interest rate swaps, which converts a fixed interest rate into a floating interest rate or vice versa. This offers protection against rate fluctuations, and the opportunity for speculative position taking. A large part of the turnover in both foreign exchange and interest rate derivatives markets is inter-bank activity, with these institutions hedging positions built up through market-making activity, or for proprietary purposes. According to data from the Bank for International Settlements (BIS), around 70 per cent of total turnover reported by Australian-located counterparties is undertaken with another bank, either domestically or offshore.

The RBA data shows the range of products, but the largest by far relate to interest rate swaps, which converts a fixed interest rate into a floating interest rate or vice versa. This offers protection against rate fluctuations, and the opportunity for speculative position taking. A large part of the turnover in both foreign exchange and interest rate derivatives markets is inter-bank activity, with these institutions hedging positions built up through market-making activity, or for proprietary purposes. According to data from the Bank for International Settlements (BIS), around 70 per cent of total turnover reported by Australian-located counterparties is undertaken with another bank, either domestically or offshore.

Looking in more detail, across the various instruments, there are more than $22.7 trillion of swaps are out there, plus other interest rate vehicles, as well as a smaller volume of foreign exchange contracts. These are the principal amounts of the instrument. By the way, the options contracts can be more risky depending whether you hold a put or a call option – but that’s another story.

Looking in more detail, across the various instruments, there are more than $22.7 trillion of swaps are out there, plus other interest rate vehicles, as well as a smaller volume of foreign exchange contracts. These are the principal amounts of the instrument. By the way, the options contracts can be more risky depending whether you hold a put or a call option – but that’s another story.

The bulk of the transactions are interest rate related. But it is worth noting as the RBA did in 2011, that “because redundant OTC derivatives positions are not generally closed out (unlike exchange-traded derivatives), turnover volumes result in a significant build-up of gross outstanding positions for dealers. This notional amount is a much larger figure than the estimated market value of these positions. The bulk of this build-up is due to interest rate derivatives, reflecting both the longer maturity of many interest rate derivatives contracts, and the heavy utilisation of these as hedging instruments by banks and their counterparties. Foreign Exchange derivatives comprise a smaller, though still significant, share. The relatively slower build-up in these positions over time largely reflects the much shorter duration of many FX instruments (in general, these may last only a few days or weeks, compared with many months and years for interest rate derivatives). The interdependencies of counterparties and operational complexities resulting from the build-up of these positions are prime reasons why some central clearing of these positions is desirable”.

The main dealers in Australia include, ANZ, Bank of America–Merrill Lynch, Bank of Tokyo-Mitsubishi, Barclays Capital, BNP Paribas, Citi, CBA, Deutsche Bank, Goldman Sachs, HSBC, J.P. Morgan, Macquarie Group, National Australia Bank, Royal Bank of Canada, UBS, and Westpac.

Just to confuse the picture a bit more, data from DTCC Data Repository (Singapore) Pte. Ltd. (DDRS), says OTC derivatives notional outstanding in Australia totaled $42.3 trillion as of June 30, 2017. Interest Rate Derivatives totaled $34.7 trillion and accounted for 82% of notional outstanding. Foreign Exchange derivatives comprised $7.3 trillion (17% of notional outstanding) and credit derivatives totaled only $264.1 billion. This is because OTC derivatives are used by parties other than banks of course, so the number is larger than the RBA bank series.

Australian Financial Markets Association (AFMA) is another data source. It was formed in 1986 and is “the leading industry association promoting efficiency, integrity and professionalism in Australia’s financial markets” according to their web site. They have more than 110 members, from Australian and international banks, leading brokers, securities companies and state government treasury corporations to fund managers, energy traders and industry service providers. The latest data from AFMA, which was included in their 2017 report says that OTC notional outstanding in Australia was $47.2 trillion, again with interest rates instruments the main element.

But, which ever way you look at it, the numbers are large.

But, which ever way you look at it, the numbers are large.

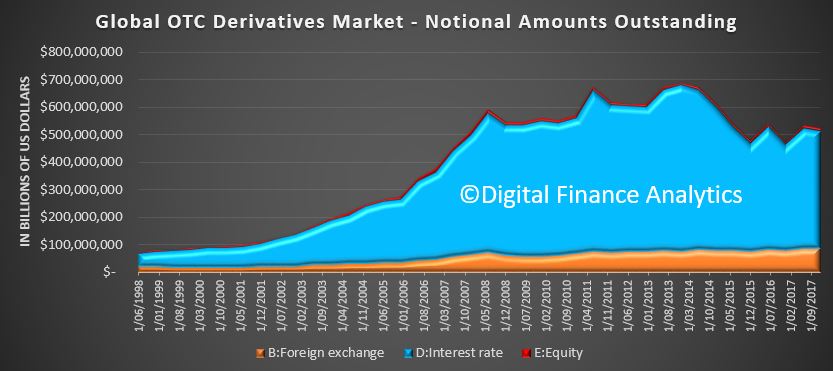

But, we cannot stop there. To try to get to grips with the bigger picture, lets look at the latest data from the BIS – The Bank For International Settlements, the Bankers Banker. They produce massive volumes of statistics including a series on derivatives. Their latest data is to December 2017 and they show that globally the nominal value of Over The Counter (OTC) derivatives has since 2015 has fluctuated in a range between about $480 trillion and $550 trillion. Notional amounts remained in this range in the second half of 2017, ending the year at $532 trillion. On a comparable basis, Australia would comprise about about $31.5 trillion of this, or about 6% of the total, although the RBA notes that data sourced from AFMA and BIS are not strictly comparable, in part due to differences in the data collection basis, and different categorisations of the Australian operations of foreign banks.

Globally, this is down from the $US710 trillion at the end of 2013, which was a 12 per cent increase on the year before. The longer term trend however shows the significant growth over the medium term. Relativity, Australian exposures are growing. But just how much is an interesting question.

Globally, this is down from the $US710 trillion at the end of 2013, which was a 12 per cent increase on the year before. The longer term trend however shows the significant growth over the medium term. Relativity, Australian exposures are growing. But just how much is an interesting question.

Then we need to ask whether the notional amounts outstanding are a meaningful number, because these turnover figures measure the notional principal of contracts. Because of the derivative nature of these transactions, the full principal is generally not exchanged at the time the transaction is initiated, nor might it ever be exchanged over the lifetime of the contract. This is unlike transactions in securities such as equities or bonds, where the full amount of consideration is exchanged at the time the transaction is settled.

Then we need to ask whether the notional amounts outstanding are a meaningful number, because these turnover figures measure the notional principal of contracts. Because of the derivative nature of these transactions, the full principal is generally not exchanged at the time the transaction is initiated, nor might it ever be exchanged over the lifetime of the contract. This is unlike transactions in securities such as equities or bonds, where the full amount of consideration is exchanged at the time the transaction is settled.

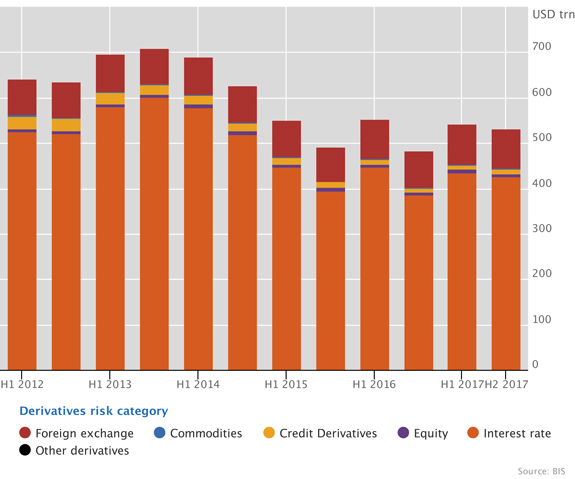

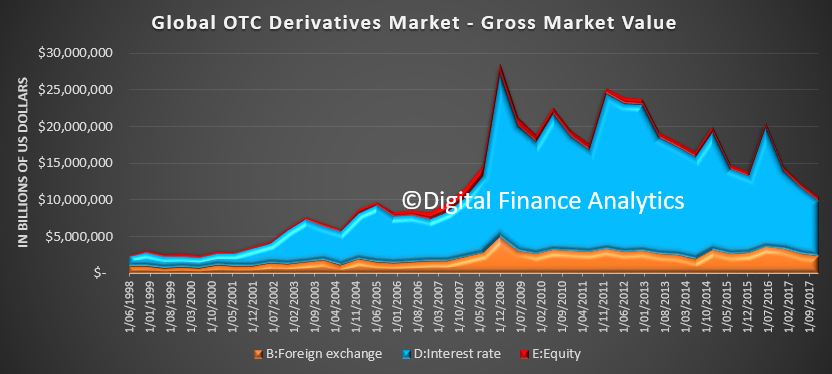

There is another way to look at the exposure. That is through the lens of bought and sold positions. The BIS says the sum of the absolute values of all outstanding derivatives contracts with either positive or negative replacement values evaluated at market prices prevailing on the reporting date gives us the gross market value. Globally, the gross market value of outstanding OTC derivatives contracts fell to $11 trillion at end-2017, its lowest level since 2007. The share of centrally cleared credit default swaps (CDS) rose to 55% at end-2017, as central clearing made further inroads.

So you might net off the exposures, positive and negative, to get a baseline netted position. In a balanced position the exposures may be quite small, but changes in relative rates may create much larger exposures without much notice. Thus in a volatile market these exposures could be larger than anticipated, which creates the risks in the system.

So you might net off the exposures, positive and negative, to get a baseline netted position. In a balanced position the exposures may be quite small, but changes in relative rates may create much larger exposures without much notice. Thus in a volatile market these exposures could be larger than anticipated, which creates the risks in the system.

The RBA said in 2010, the estimated market value of cross-sectoral bought (or sold) positions across all derivatives classes (both exchange traded and OTC) was around $350 billion, as opposed to the $15 trillion dollars notional exposure. The largest component of this was positions bought and sold between domestic financial institutions and offshore counterparties (largely financial institutions). However, the public sector and the non-financial corporate sector are also significant users, each with around $30 billion of bought and sold positions outstanding as at December 2010.

So the exposures can range from trillions of dollars to a few billions. It all depends what you mean by “exposures” in the first place.

And this is where it gets tricky. Banks have an obligation to assess their off-balance sheet exposures and use APRA approved formulations to discount the total exposures back to those which may appear in the balance sheet. Does APRA get inside these figures or validate them. We suspect not, leaving it to the accountants who work with the banks. An APRA spokesman after the GFC said, said: “We are not in the business of running banks, we are in the business of supervising them”, adding that the role of APRA was to set standards that the banks agreed to abide by.

But as we have described the exposures are highly leveraged, and in a time of crisis, these smaller deeply discounted exposure values may be insufficient to handle the demands from the derivatives they hold. If so, and in a crisis, a bank may find their exposures escalate and it might swamp their balance sheet, meaning that the other operations, including loans and deposits may get caught up.

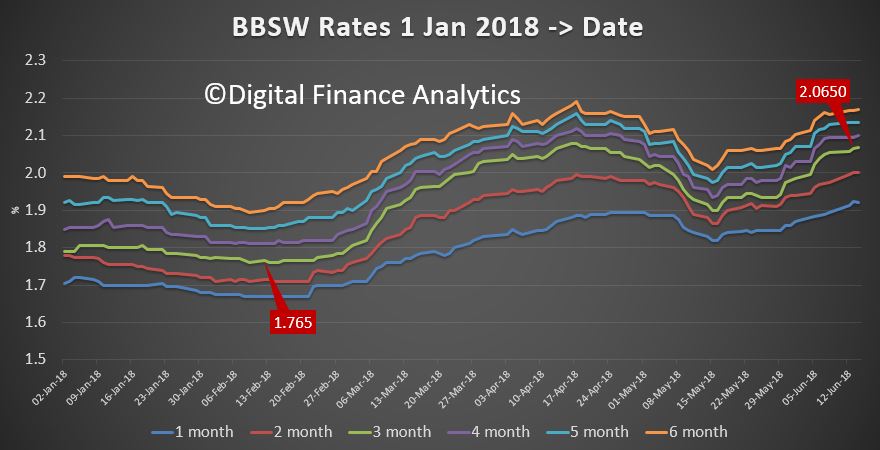

This is especially relevant, because in the current environment, with interest rates shifting between the USA and Australia, as shown by the BBSW chart, (rates have move up around 30 basis points since February) things could get interesting.

And this is the point, banks who play in the derivatives area actually have additional risks in their business, which are not knowable, but potentially large. In a crisis, it risks the rest of the business. There is no ring fence.

And this is the point, banks who play in the derivatives area actually have additional risks in their business, which are not knowable, but potentially large. In a crisis, it risks the rest of the business. There is no ring fence.

And this is where Glass-Steagall comes in, because this legislation would separate the trading operations from core banking operations, and protect depositors as a result. The current “all mixed up” universal banks are totally exposed.

But such a change would also have an immediate impact on both the profitability and capability of banks, which is why they will resist any such move, despite it now being proposed in Italy, and already in existence in some form in China.

The bottom line is the $37 trillion is a good representation of the current gross exposures in our banking system, and this dwarfs the banks’ current balance sheets, and the countries total economy. The risks are literally enormous, and in a system-wide banking crash, when multiple parties are exposed, a bail-out if required would likely have profound economic effects. It might be enough to swamp the entire economy. That’s how big the potential risks are. That’s why Glass-Steagall is worth pursuing.