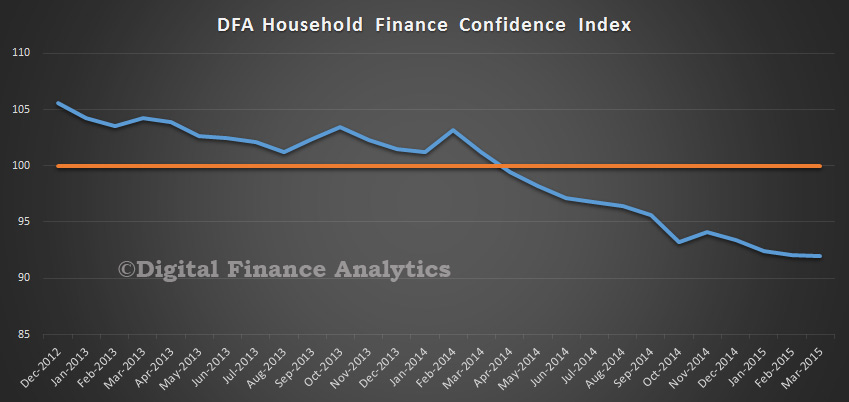

We have released the latest edition of the DFA Household Finance Confidence Index, the results of are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health.

To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

The overall index fell from 92.1 to 91.97 in March, which continues the overall declining trend since February 2014.

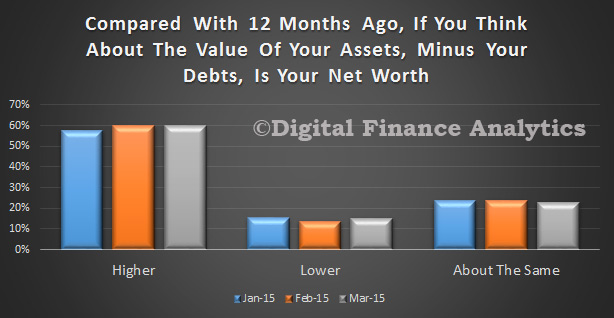

Looking at the elements within the index, nearly 60 percent of households are enjoying a growth in their net worth, mainly thanks to further rises in house prices and positive stock market movements. On the other hand, there was a rise of 1.5 percent in those who have seen their net worth fall, these are households who predominately do not own property.

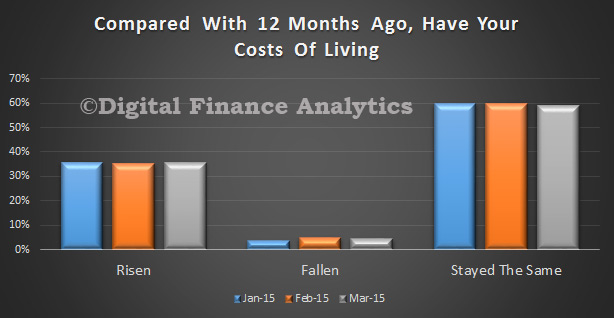

There were small movements in the costs of living data, with school fees and child care being two elements which have hit some households hard, though offset by falls in the costs of fuel. We also see the impact of falling exchange rates on overseas purchases, especially from the US. Finally, rentals are increasing faster than incomes for some households, especially in cities on the east coast.

Household real incomes are relatively static, though there is little evidence of rising income. Less than 4 percent of households recorded a rise in real terms.

Some households are a little more comfortable with their level of debt, this is directly linked to the fall in RBA rates in February. However, there was also a rise in those households who were concerned about the debts they owed, with a rise of 0.57 percent. On average females were more concerned than males, and older households more worried than younger ones.

There was a small rise in households who were more comfortable with their savings position, but more are less comfortable, and this is directly linked to the current low interest rates offered for deposits, and the prospect of even lower rates, and the quest for higher yield elsewhere looking ahead. Females were significantly more concerned than males.

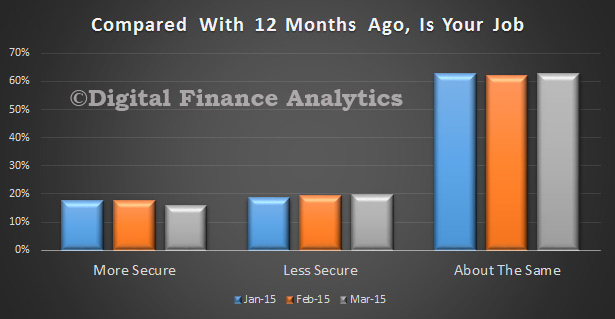

Finally, looking at job security, there was a significant rise in those households who are concerned, with a drop in those who felt more secure than last year by 1.7 percent and a rise in those who fell less secure. That said, more than 60 percent registered as about the same. We noted some state variations, with those in WA significantly more concerned than those in NSW.

Note that the detailed state by state and segmented data is not publicly released. We will update the index again in a months time.

Note that the detailed state by state and segmented data is not publicly released. We will update the index again in a months time.

One thought on “DFA Household Finance Confidence Index Falls In March”