Following on from yesterdays video blog on the overall results from the latest household surveys, over the next few days, we will dig further into the data. We start with some cross segment observations, before in later posts, we begin to go deeper into segment specific motivations. You can read about our segmentation approach here. Many households still want to get into property – demand is strong, thanks to lower interest rates, despite high home prices and flat incomes. Future capital growth is expected by many in the market, and by those hoping to enter. This despite a fall in household confidence, as measured in our finance confidence index.

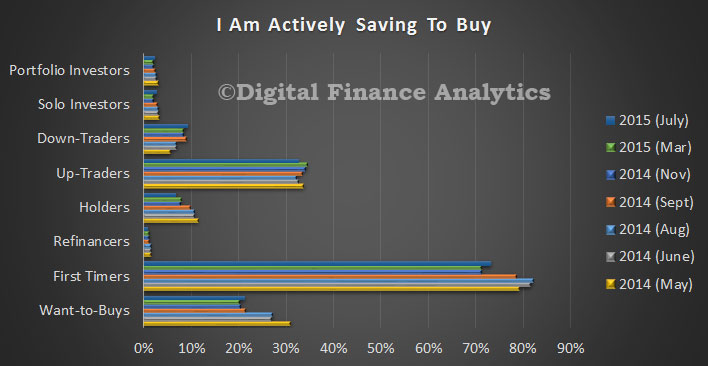

We start with savings intentions. Prospective first time buyers are saving the hardest, despite the lower interest being paid on deposits. More than 70% are actively saving to try and get into the market (though we will see later, more are switching to an investment purchase). Portfolio and solo property investors are saving the least – despite the recent changes to LVR’s on loans.

A significant proportion of those saving are actively foregoing other purchases and spending less, so they can top up their deposits. A higher proportion are also looking to the “Bank of Mum and Dad” for help.

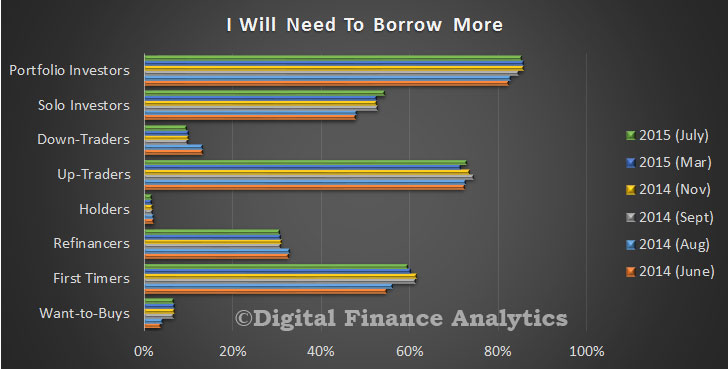

Looking next at borrowing intentions over the next 12 months (an indication of future mortgage finance demand), down-traders are slightly less likely to borrow now, compared with a year ago, whilst investors are firmly on the loan path. First time buyers will need to borrow. Refinancers are active, and one motivation we are seeing is the extraction of capital during refinance, onto a lower interest rate.

Looking next at borrowing intentions over the next 12 months (an indication of future mortgage finance demand), down-traders are slightly less likely to borrow now, compared with a year ago, whilst investors are firmly on the loan path. First time buyers will need to borrow. Refinancers are active, and one motivation we are seeing is the extraction of capital during refinance, onto a lower interest rate.

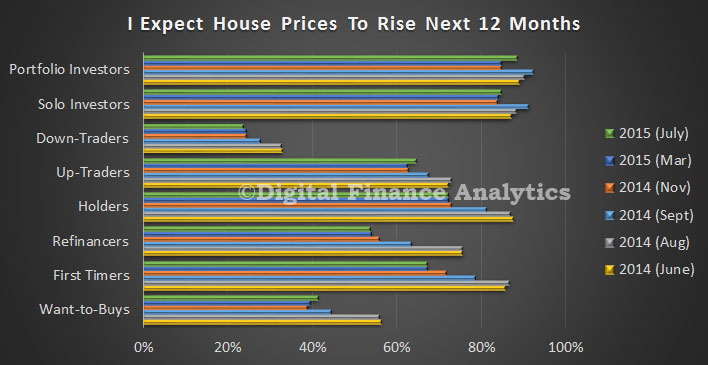

Many households are still bullish on house price growth. Investors are the most optimistic, whilst down-traders the least. There are significant state differences, with those in the eastern states more positive than those elsewhere.

Many households are still bullish on house price growth. Investors are the most optimistic, whilst down-traders the least. There are significant state differences, with those in the eastern states more positive than those elsewhere.

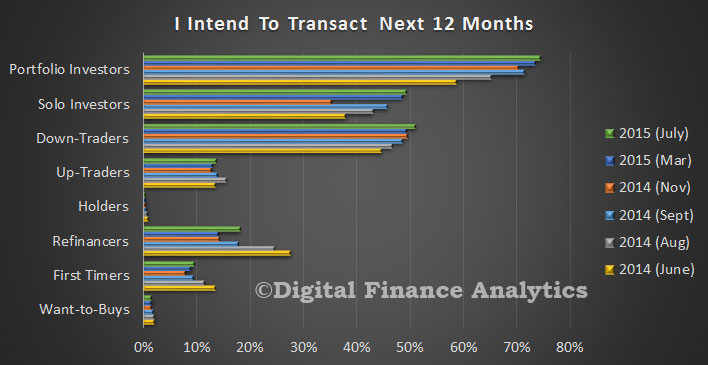

So, who is most likely to transact? Portfolio investors are most likely, then down-traders, and solo investors. There is also a lift in the number of households looking to refinance, to take advantage of lower interest rates. The recent public announcements by the banks, about tightening lending criteria appears to have encouraged some to bring forward their plans to purchase, in the expectation that later it may be more difficult to get a loan.

So, who is most likely to transact? Portfolio investors are most likely, then down-traders, and solo investors. There is also a lift in the number of households looking to refinance, to take advantage of lower interest rates. The recent public announcements by the banks, about tightening lending criteria appears to have encouraged some to bring forward their plans to purchase, in the expectation that later it may be more difficult to get a loan.

The recent tweaks in rates are having no impact on household plans, as the absolute rates are still very low – lower than ever – for many. We conclude that the demand side of the property and mortgage markets are still intact.

The recent tweaks in rates are having no impact on household plans, as the absolute rates are still very low – lower than ever – for many. We conclude that the demand side of the property and mortgage markets are still intact.

Next time we will look in detail at data from first time buyers, and then investors.

One thought on “DFA Survey Shows Property Demand Remains Strong”