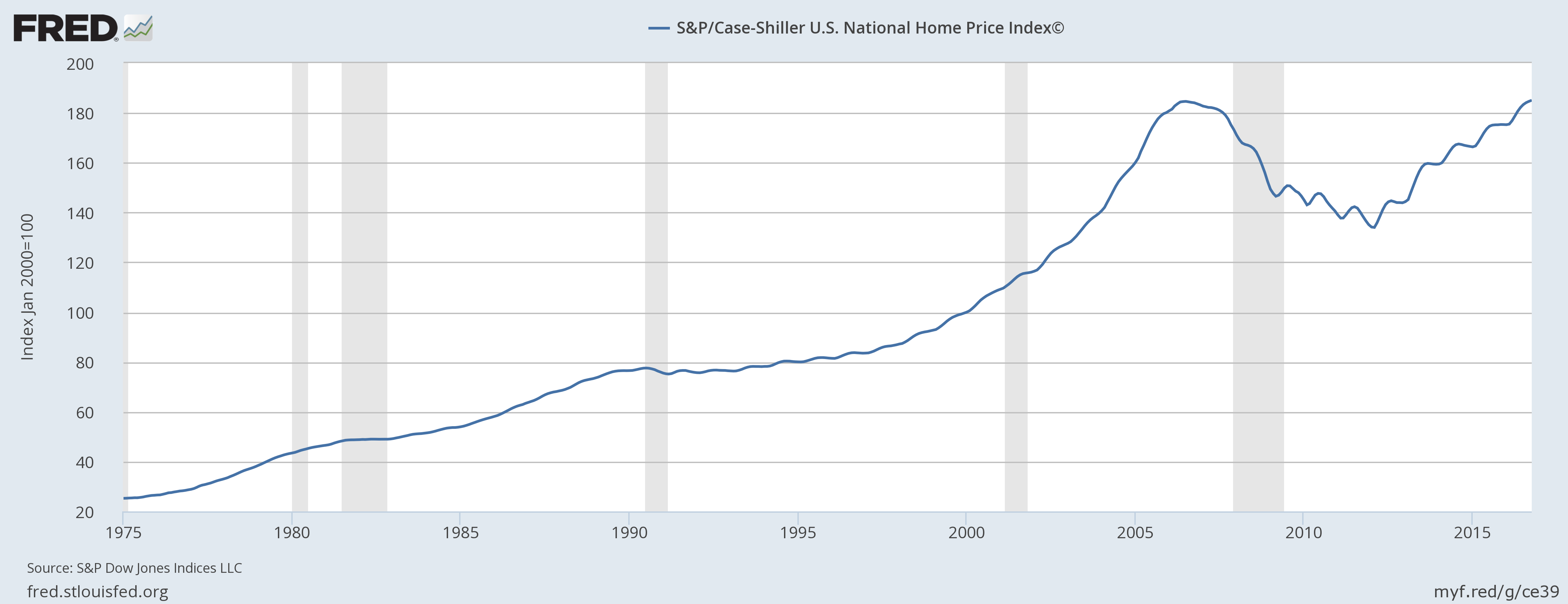

Between 2000 and 2008, two of the largest financial bubbles in history — in technology stocks and housing, respectively — suffered spectacular collapses. Opinions vary, but some market commentators believe at the peak of the tech bubble, total stock market capitalization exceeded 180% of US GDP. To put this in perspective, the tech stock bubble was over twice the size of the 1920s stock bubble!1 As large as the bubble in tech stocks was, it was child’s play compared to the housing bubble. When the US housing bubble collapsed, the credit losses were so large the entire worldwide banking system was considered to be in mortal danger.

One of the primary justifications behind the 1913 founding of the Fed was to prevent financial crises. Logic then dictates if a major motivation behind forming a central bank is the prevention of a financial crisis, then a financial crisis that breaks out under the nose of a central bank must be due — at least in part — to mistakes of that bank. The Fed’s mistakes and its subsequent leading role in causing the housing bubble will be seen by reviewing speeches given by Alan Greenspan and Ben Bernanke that praised the housing bubble era Fed. In addition, a review of statements made in the wake of the tech bubble’s collapse will reveal senior Fed officials taking positions diametrically opposed to positions Alan Greenspan claimed formed the basis for the Fed’s policy toward bubbles, namely, allowing bubbles to burst and dealing with the consequences later.

From its March 2000 peak to its October 2002 bottom the NASDAQ declined 80%. Throughout the 1990s no one cheered on the “new economy” more than the “maestro,” Alan Greenspan. After the bubble collapsed, Greenspan recognized a need to explain his and the Fed’s actions while the tech bubble grew. In August 2002 Greenspan gave a speech at the Fed’s conference in Jackson Hole. In this speech, which Jim Grant called “self-exculpating revisionism,”2 Greenspan offered this rationale for the Fed’s actions during the late 1990s:

The struggle to understand developments in the economy and financial markets since the mid-1990s has been particularly challenging for monetary policymakers. … We at the Federal Reserve considered a number of issues related to asset bubbles — that is, surges in prices of assets to unsustainable levels. As events evolved, we recognized that, despite our suspicions, it was very difficult to definitively identify a bubble until after the fact — that is, when it’s bursting confirmed its existence.

Less than two years later, in January 2004, Greenspan would congratulate himself on the apparent success of the Fed’s strategy. In doing so he would expose the Fed’s role in creating the far more ruinous housing bubble.

There appears to be enough evidence, at least tentatively, to conclude that our strategy of addressing the bubble’s consequences rather than the bubble itself has been successful. … As I discuss later, much of the ability of the U.S. economy to absorb these sequences of shocks resulted from notably improved structural flexibility. But highly aggressive monetary ease was doubtless also a significant contributor to stability.3

The “monetary ease” — slashing interest rates — Greenspan was taking credit for here was not helping the economy heal. Instead it was fueling an enormous bubble in housing whose negative consequences can best be described as world-altering.

One month later, in February, Greenspan’s partner in criminal economic ignorance, Ben Bernanke, gave a speech titled, “The Great Moderation.” In this speech Bernanke would, unknowingly, provide further evidence of the Fed’s enormous role in fueling the housing bubble. Bernanke claimed the Fed’s monetary policy was a source of stability and helped to reduce variations in economic output. The irony in giving this speechat this time should not be lost. Bernanke’s speech, like Greenspan’s, betrays a total ignorance of the enormous housing bubble that was only a few weeks from peaking. (Homeownership peaked in April 2004!) With just these two speeches, the criminal incompetence of the Greenspan/Bernanke and the leading causal role the Fed played in the housing bubble are demonstrated.

The Fed’s bubble befuddlement was not limited to a few speeches. For years on end Fed officials would take positions in contradiction to those established by Greenspan in his Jackson Hole, Wyoming, speech. For example, in July 2005 and in his capacity as head of the president’s council of economic advisors, Ben Bernanke was asked on CNBC if there was a housing bubble. He does not answer by saying bubbles can’t be seen until after they burst. Instead he says the following:

Well, I guess I don’t buy your premise. It’s a pretty unlikely possibility. We’ve never had a decline in housing prices on a nationwide basis, so what I think is more likely is house prices will slow, maybe stabilize, might slow consumption spending a bit. I don’t think it will drive the economy from its full employment path.

Later in October 2005, other Fed officials would also contradict Greenspan’s Jackson Hole speech. By then, homeownership had already peaked and the bubble had started to collapse. Amazingly, two Fed economists investigated if there was a housing bubble. They — erroneously, of course — concluded home prices are “high but not out of line.”4 Obviously, if Fed officials were investigating to see if a housing bubble existed, then they believed it could be observed without first having to collapse.

Often, the most damning indictments of the bubble-era Fed come from other Fed officials. The most loquacious of these officials is current St. Louis Fed president James Bullard. Among the truths Bullard accidently exposed was the one concerning the obvious nature of the recent stock and housing bubbles. In a September 2013 interview Bullard said, “The bubbles we had in the past were gigantic and obvious.”5 Later, in a November 2013 interview, he said the housing and tech bubbles were “blindingly obvious.”6

Amazingly, Alan Greenspan would eventually completely contradict Greenspan! Here is “Mr. Chairman,” as CNBC lovingly refers to him, discussing the Lehman Brothers failure in October 2013, “We missed the timing badly on September 15th, 2008 [the day Lehman Brothers went bankrupt]. All of us knew there was a bubble.”7 So which is it Mr. Chairman? Can bubbles be “obvious” or something “everyone knew” to exist before they pop — as you indicate here — or do you have to wait until after they pop to confirm their existence as you said in Jackson Hole?

Our brief review here demonstrates both the leading role the Fed played in creating the housing bubble — the January and February 2004 speeches — and the many mutually exclusive positions the Fed took on bubbles. In spite of being exposed in what is either a self-exculpating lie (the claim that bubbles can only be seen after they burst) or a sign of gross incompetence (the failure to see two of the largest financial bubbles in history), no Fed official has ever been asked to explain or rationalize the Fed’s contradictory positions on bubbles. Whether anyone from the Fed is ever forced to do so or not, it is obvious the Fed has much to answer for concerning all the economic hardships their bubble befuddlement has caused.

- 1. Marc Faber, “The Monetization of the American Economy,” DailyReckoning.com, January 16, 2002 https://dailyreckoning.com/the-monetisation-of-the-american-economy/

- 2. Jim Grant, Mr. Market Miscalculates (Mt. Jackson, Va.: Axios Press, 2008), pp. 241.

- 3. “Risk and Uncertainty in Monetary Policy”, Remarks by Chairman Alan Greenspan at the Meetings of the American Economic Association, San Diego, California, January 03, 2004.

- 4. Jonathan McCarthy and Richard W. Peach, “Is there a Bubble in the Housing Market Now?” Federal Reserve Bank of New York, 2005.

- 5. Steven C. Johnson, “Fed Need Not Rush to Taper While Inflation is Low,” September 20, 2013, CNBC, http://www.cnbc.com/id/101051526/

- 6. Matthew J. Belvedere, “Fed’s Bullard: $1-trillion a year QE pace torrid,” CNBC, http://www.cnbc.com/id/101166475

- 7. Matthew J. Belvedere, “Bubbles and leverage cause crisis: Alan Greenspan,” October 23, 2013 CNBC, http://www.cnbc.com/id/101135835