Interesting Analytical Note from the Reserve Bank New Zealand. They have recently changed their modelling of inflation, preferring to use past data rather than a two year prediction because despite low unemployment, inflation has remained lower than would be expected on the old method. This suggests monetary policy needs to be more stimulatory than expected .

Forecasts of non-tradables inflation have been produced using Phillips curves, where capacity pressure and inflation expectations have been the key drivers. The Bank had previously used the survey of 2-year ahead inflation expectations in its Phillips curve. However, from 2014 non-tradables inflation was weaker than the survey and estimates of capacity pressure suggested. Bank research indicated the weakness in non-tradables inflation may have been linked to low past inflation and its impact on pricing behaviour.

This note evaluates whether measures of past inflation could have been used to produce forecasts of inflation that would have been more accurate than using surveys of inflation expectations. It does this by comparing forecasts for annual non-tradables inflation one year ahead. Forecasts are produced using Phillips curves that incorporate measures of past inflation or surveys of inflation expectations, and other information available at the time of each Monetary Policy Statement (MPS). This empirical test aims to determine the approach that captures pricing behaviour best, highlighting which may be best for forecasting going forward.

The results show that forecasts constructed using measures of past inflation have been more accurate than using survey measures of inflation expectations, including the 2-year ahead survey measure previously used by the Bank. In addition, forecasts constructed using measures of past inflation would have been significantly more accurate than the Bank’s MPS forecasts since 2009, and only slightly worse than these forecasts before the global financial crisis (GFC). The consistency of forecasts using past-inflation measures reduces the concern that this approach is only accurate when inflation is low, and suggests it may be a reasonable approach to forecasting non-tradables inflation generally.

From late 2015, the Bank has assumed that past inflation has affected domestic price-setting behaviour more than previously. As a result, monetary policy has needed to be more stimulatory than would otherwise be the case. This price-setting behaviour is assumed to persist, and is consistent with subdued non-tradables inflation and low nominal wage inflation in 2017.

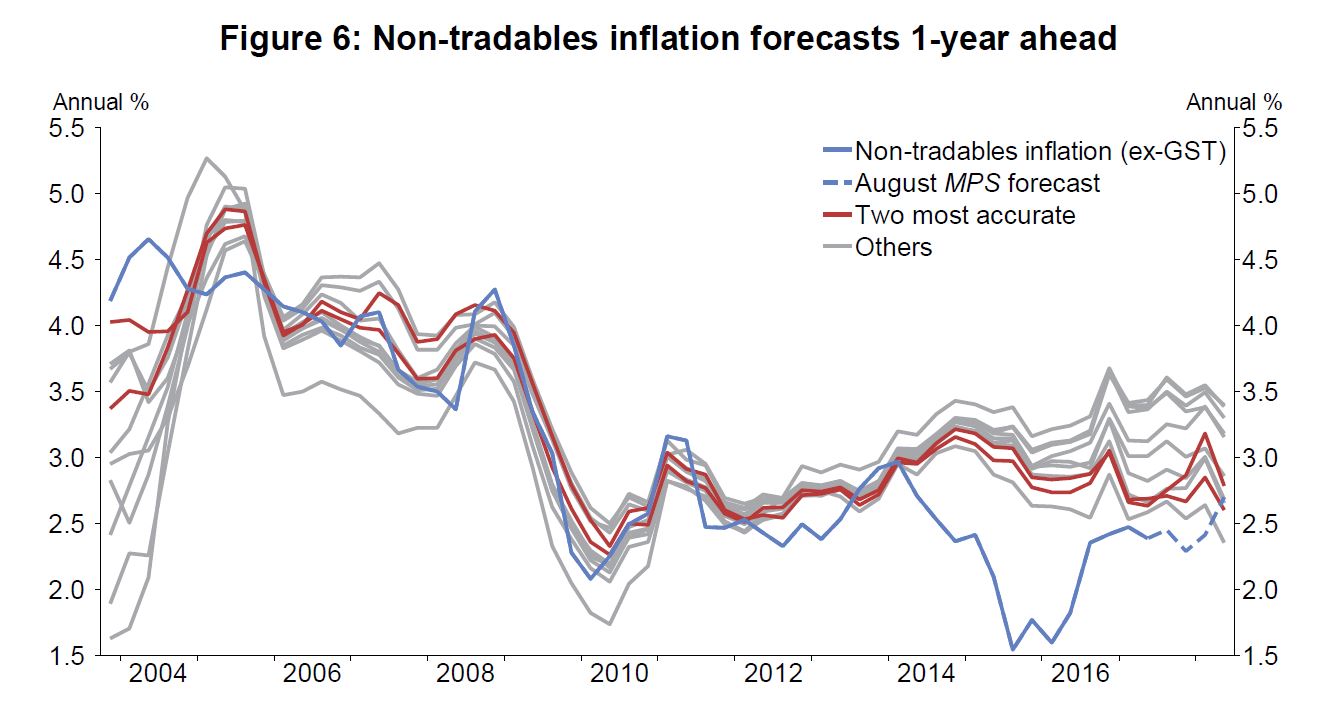

Figure 6 shows the average 1-year ahead forecast of non-tradables inflation for the measures of past inflation and surveys of inflation expectations. The range of forecasts produced by the models is currently large relative to history, perhaps reflecting differences between the surveys of inflation expectations and measures of past inflation. The two most accurate measures (shown by the red lines) suggest non-tradables inflation will be between 2.5 and 3 percent in 2018 – similar to the forecast in the August 2017 MPS and only a little higher than the latest outturn of 2.4 percent in the June quarter 2017.

Conclusion

Non-tradable inflation has been surprisingly weak since 2014. Phillips curves with the survey of 2-year ahead inflation expectations suggest non-tradables inflation should have risen by more than we have seen, given the level of the unemployment rate and the Bank’s estimates of the output gap. This note shows that using measures of past CPI inflation instead of surveyed inflation expectations would have produced more accurate forecasts of non-tradables inflation, although not all of the weakness in non-tradables inflation would have been predicted.

The Bank has adjusted its forecasting models to better capture the role of past inflation, moving away from using the survey of 2-year ahead inflation expectations to underpin its forecasts

The Analytical Note series encompasses a range of types of background papers prepared by Reserve Bank staff. Unless otherwise stated, views expressed are those of the authors, and do not necessarily represent the views of the Reserve Bank.