The dollar has ousted the VIX index as a barometer of the banking sector’s appetite for leverage, with bank lending coming under pressure when the dollar appreciates, Bank for International Settlements Economic Adviser and Head of Research Hyun Song Shin said on Tuesday.

Speaking at the London School of Economics, Mr Shin said the link between the VIX, a measure of implied stock market volatility, and bank borrowing, or leverage, which had held before the crisis has broken down since. Bank leverage has been subdued despite low VIX readings. Instead, bank leverage is now tied more closely to the dollar.

“Just as the VIX index was a good summary measure of the price of balance sheets before the crisis, so the dollar has become a good measure of the price of balance sheets after the crisis,” Mr Shin said.

“The dollar has supplanted the VIX index as the variable most associated with the appetite for leverage. When the dollar is strong, risk appetite is weak.”

Mr Shin said the breakdown of rules of thumb for well functioning markets, like the equalisation of interest rates across different market segments, showed that incipient deleveraging pressures have been building in recent months.

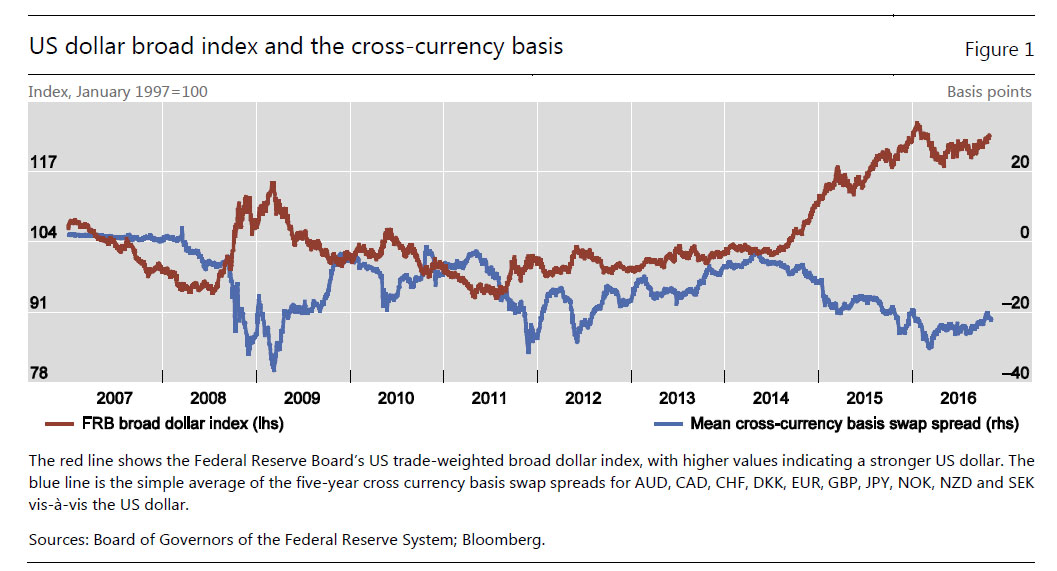

This rise in the so-called cross-currency basis, the premium banks charge borrowers of sought-after currencies like the US dollar, reflects the breakdown of covered interest parity (CIP), a previously ironclad rule that kept the interest rates implicit in currency markets closely in line with those in money markets.

A BIS working paper, published on Tuesday, found that a stronger dollar means wider deviations from CIP – signalling the higher cost of borrowing dollars in foreign exchange markets – as well as a pullback in cross-border bank lending in dollars.

The paper, by Mr Shin and BIS colleagues Stefan Avdjiev and Cathérine Koch, together with Wenxin Du from the US Federal Reserve Board, finds that a stronger dollar crimps bank balance sheets and reduces banks’ ability to take on risks.

“To the extent that the CIP deviation turns on the constraints on bank leverage, our results suggest that the strength of the dollar is a key determinant of bank leverage,” the paper states. Eroding bank risk capital put a higher price on bank balance sheets, while better capitalised banks were more able to withstand deleveraging pressures and keep up the flow of credit to the real economy.

Mr Shin said the developments showed the need for a global perspective in tracking the functioning of the financial system and the importance of capital market indicators in assessing strains that affect banks and the wider economy.

“This link between banks and capital markets has gone global. We can begin to understand some of the big puzzles of our day when we lift our gaze to take in this global picture,” he said.