The Reserve Bank has today published a consultation paper on dual-network debit cards and mobile wallet technology following discussion of these issues by the Payments System Board at its November meeting.

Dual-network debit cards are debit/ATM cards that allow transactions to be routed through two different networks. They offer convenience for cardholders and enhance the ability of merchants to encourage the use of lower-cost payment methods. Around two-thirds of the debit cards issued in Australia have dual-network functionality.

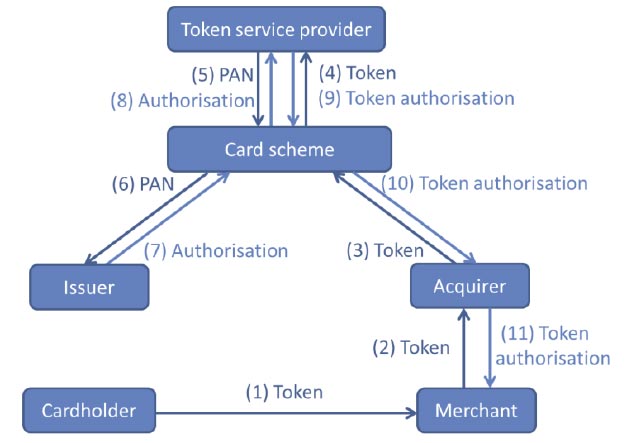

New technology has enabled mobile devices, such as mobile phones, to be used to make payments via an electronic representation of a payment card, as opposed to a traditional plastic card. The electronic representation of a card is typically contained in a ‘mobile wallet’, which is a software application on a mobile device that enables payments to be made through the card networks. This technology may offer greater convenience for cardholders as it avoids some of the physical limitations of carrying and using multiple plastic cards.

Some stakeholders have recently raised concerns about possible restrictions on competition in the mobile wallet sphere, specifically about conduct that may prevent or make it more difficult for both networks on a dual-network debit card to be enabled on a mobile device. This conduct could have the effect of reducing choice and convenience for cardholders in making mobile payments and reduce the ability of merchants to encourage the use of lower-cost payment methods. This consultation paper discusses these issues and raises a number of specific questions for consultation.

Interested parties are invited to make submissions on the consultation paper by 7 February 2017.

Questions for consultation:

1. What are the views of end-users (cardholders and merchants) regarding dual-network cards, including their use in mobile payments? Are there particular benefits that arise for end-users from having multiple payment networks available on a mobile device? What risks and costs might arise?

2. Are there any impediments or restrictions imposed (or planned or foreshadowed) by card schemes on the mobile wallet provisioning of competing networks on dual-network cards? If so, how significant are these and can they be justified on commercial or other grounds?

3. What are the likely effects – on competition and efficiency in the payments system, as well as more broadly – of the action of any scheme to prevent or discourage the mobile wallet provisioning of a competing network on a dual-network card? Are there benefits for end-users that arise from rules or policies that constrain the provisioning of an additional network on a device?

4. Do cardholders, issuers or others have views as to the feasibility of different possible ways of provisioning dual-network cards?

5. Under the existing voluntary undertakings to the Bank in place since August 2013 (see page 4), schemes have committed to some voluntary principles regarding dual-network cards. Have these principles been an effective response to the competitive issues that arose earlier? Have there been any issues in practice with the operation of these principles? Would an extension of these principles be an appropriate response to the current issues?

6. Are there any foreign precedents that are relevant for the consideration of these issues in Australia?

7. Are the issues raised relevant only to dual-network debit cards or are they also relevant to so-called ‘combo cards’ with credit functionality from one scheme and debit functionality from another?

8. Are there any prospective developments in payment card technology that may be relevant for the Bank as it considers these issues?

9. If the Bank were to contemplate a standard addressing conduct in this area, are there particular compliance costs that would arise for industry?

Dual-network (or ‘co-badged’) cards have attracted the attention of policymakers in a number of other jurisdictions – most notably the United States, Canada and the European Union, with different policy responses. In each case, however, the response has tended to focus on reducing costs to payments system end-users.

In the United States, Section 1075 of the 2010 Dodd-Frank Act, known as the Durbin Amendment, provided for a number of reforms to the debit card market with the intention of providing more competition in the market. One aspect, which came into effect in April 2012, has the effect of requiring that all debit cards be enabled on at least two unaffiliated networks. Networks must also not restrict or limit an issuer’s ability to contract with other networks.

In the European Union, the 2015 regulation on interchange fees makes specific reference to co-badged cards and their role in reducing the cost of payments. The regulation prevents card schemes from having rules that prevent issuers from including payments functionality of two or more networks on one card. It also requires that any scheme rules, routing principles or technical or security standards involving co-badged cards should be objectively justified and non-discriminatory. It specifies that the choice of payment application for transactions using co-badged cards should be made by users, not imposed by card schemes, issuers, acquirers or processing entities.

Individual countries within Europe have different structures with respect to card networks and mobile payments. For example: In Denmark, the domestic debit card system is Dankort; there are also co-badged ‘Visa Dankort’ debit cards. On co-badged cards, domestic transactions are routed via Dankort, while transactions made abroad are routed through the Visa network. In France, Carte Bancaire is the domestic (credit and debit) scheme, often co-badged with MasterCard or Visa, with the latter networks used typically for cross-border transactions and Carte Bancaire used for domestic purchases. In Canada, the Code of Conduct for the Credit and Debit Card Industry in Canada (‘the Code’) explicitly provides for dual-network cards but takes a different approach. It allows for non-competing, complementary domestic applications from different networks to exist on the same debit card but specifies that competing domestic applications from different networks cannot be offered on the same card. In practice, this means that domestic point-of-sale transactions made on co-branded debit cards are processed through one network, in particular the domestic Interac network, while other applications such as on-line payments and payments at foreign point-of-sale terminals may be processed through the other network on the card. Contactless payments are also processed via Interac (‘Interac Flash’ transactions). The Code also states that payment card networks must ensure that co-badged debit cards are equally branded. All representations of payment applets in a mobile wallet or mobile device, and the payment card network brands associated with them, must be clearly identifiable and equally prominent.

Cardholders in Canada are now able to provision non-competing domestic networks on dual-network cards for mobile use. Although there is no unifying precedent so far regarding how public policy will evolve regarding mobile payments and dual-network cards, many authorities recognise the benefits of competition among different schemes and have sought to avoid artificial restrictions on competition. A press release from the European Commission in June this year indicates its expectation that dual-network card functionality will be available in both physical and mobile forms.7 In particular, the Commission noted that under its new interchange fee regulation, consumers will be able to require their bank to co-badge a single card (or in the future their mobile phone) with any card brands that they issue to the consumer.