The Pre-election Economic and Fiscal Outlook 2016 is out. The modelling is close to the budget numbers – though the deficit will be bigger sooner, then begin to reduce. The underlying cash balance is estimated to be a deficit of $37.1 billion (2.2 per cent of GDP) in 2016-17, improving to a deficit of $5.9 billion (0.3 per cent of GDP) in 2019-20. The current financial year deficit estimate has been changed since the budget, increasing by $100 million to $40 billion. As with any “hockey stick” projections, you just know the timing of improvements will be uncertain.

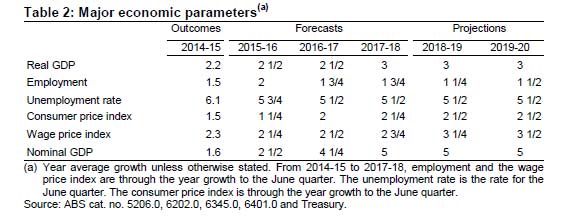

The 2016 PEFO uses the same projection methodology that has been used in budgets and budget updates since the 2014-15 Budget.

The 2016 PEFO uses the same projection methodology that has been used in budgets and budget updates since the 2014-15 Budget.

Treasury’s medium-term economic projection methodology assumes that any estimated gap between forecast real GDP and potential GDP closes over the first five projection years (2018-19 to 2022-23) as spare capacity in the labour market is absorbed. Beyond that point, real GDP and other economic variables are assumed to grow in line with their estimated long-run trend rates.

The medium-term economic and fiscal projections are sensitive to the assumptions that underpin Treasury’s estimate of potential GDP — that is, assumptions about population, productivity and participation. They are also sensitive to the assumed pace of the economy’s return to potential — that is, the assumption that the adjustment period lasts five years.

Analysis reported in the 2016-17 Budget shows that a faster (two year) adjustment to potential requires comparatively faster growth in real GDP and employment as the output gap closes and spare labour is put to use. This leads to lower unemployment and faster growth in wages and domestic prices, increasing nominal GDP and improving the projected underlying cash balance over the medium term even as

Pre-election Economic and Fiscal Outlook 2016 long-run real GDP is unchanged from the Budget projections. A more gradual adjustment period (eight years) is estimated to have broadly opposite effects on the projections.

Analysis in the 2016-17 Budget also shows that lower trend productivity growth than assumed in the Budget projections would directly reduce potential growth — leading to permanently lower real GDP and wages with only a small impact on prices. In this scenario, lower nominal GDP leads to lower projected tax receipts which weakens the projected underlying cash balance over the medium term. By contrast, assuming faster trend productivity growth than assumed in the Budget projections results in higher nominal GDP and tax receipts, strengthening the underlying cash balance.

Net debt, net financial worth, net worth and net interest payments are essentially the same as published at the 2016-17 Budget. In 2016-17, net debt for the Australian Government general government sector is expected to be $326.1 billion (18.9 per cent of GDP). Net financial worth is estimated to be -$427.2 billion and net worth is estimated to be -$301.0 billion.

Net interest payments are estimated to be $12.6 billion in 2016-17 (0.7 per cent of GDP). Interest payments largely relate to the public debt interest on government securities, based on the interest rates on the existing stock of Commonwealth Government Securities (CGS) and the prevailing market interest rates across the yield curve for future issuance of CGS. This PEFO assumes a weighted average cost of borrowing of around 2.5 per cent for future issuance of Treasury Bonds in the forward estimates period, the same as the assumed market yields used in the 2016-17 Budget. Yields are volatile and could vary from those assumed in the Budget. Recent movements in interest rates, if maintained, would lower the government cost of borrowing, reducing interest payments and expenses over the forward estimates. It would also reduce interest receipts earned on assets.