On the international horizon there are two potential events which may impact Australian bank funding. Today we consider the potential impacts on the banks, and households. First, it is likely the FED will start to lift interest rates later in the year as they adjust towards more normal rates. Second within a couple of weeks the Greek situation will crystalise, with either a negotiated debt settlement or an early exit. Both these (not totally unconnected) issues could play on bank funding because the large banks here are still quite reliant on accessing the international financial markets.

In recent times funding costs have fallen from their very high levels during the GFC. Australian bond spread mirrors the global picture.

The question is what happens if the financial markets react negatively to the news from the USA or Europe? At very least we can expect greater volatility, and the risk premium on funding costs would likely be raised. This would potentially translate to higher funding costs for the banks because they do rely on the global financial markets (we have been a net importer of funds to support the banks for years).

The question is what happens if the financial markets react negatively to the news from the USA or Europe? At very least we can expect greater volatility, and the risk premium on funding costs would likely be raised. This would potentially translate to higher funding costs for the banks because they do rely on the global financial markets (we have been a net importer of funds to support the banks for years).

However, the latest data shows that the banks have a greater proportion of funding from deposits compared with pre-GFC, and there has been a corresponding fall in short term debt funding.

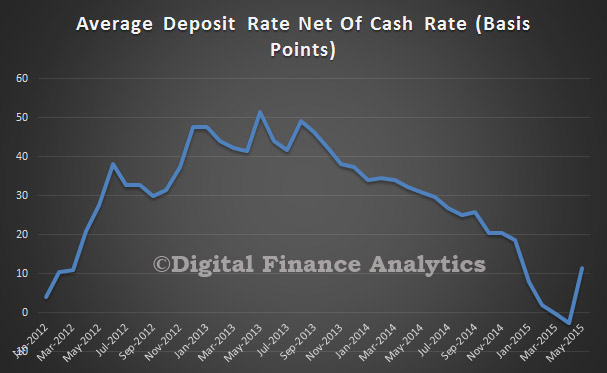

So we think the Australian Banks are quite well placed, despite the potential need to raise an additional $20-30bn to meet expected changes to their capital ratios (work in progress but it is certain to rise). They have already shown their willingness to drop deposit rates more than the market, and we think it is likely this would go further.

So we think the Australian Banks are quite well placed, despite the potential need to raise an additional $20-30bn to meet expected changes to their capital ratios (work in progress but it is certain to rise). They have already shown their willingness to drop deposit rates more than the market, and we think it is likely this would go further.

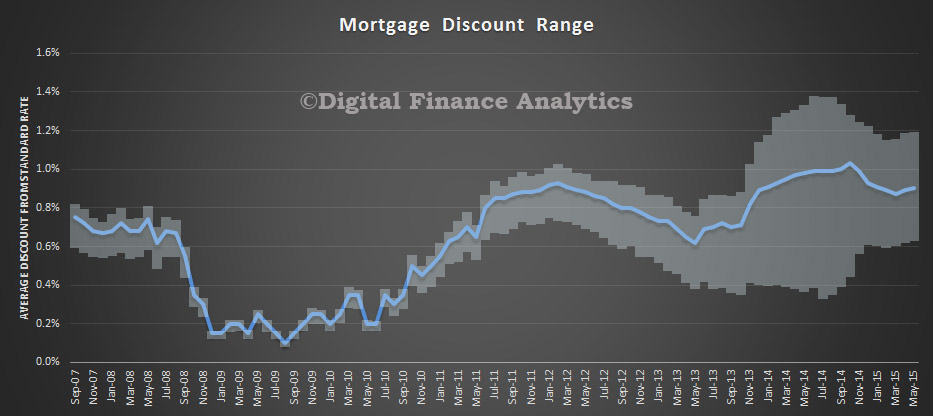

In addition, they could reduce the discounts on mortgage lending, as currently they are quite high.

In addition, they could reduce the discounts on mortgage lending, as currently they are quite high.

They could also throttle back on their lending – especially for housing – to better match deposit growth to lending growth. Finally, they have access to the RBA “emergency” fund if needed – The Committed Liquidity Facility (CLF).

They could also throttle back on their lending – especially for housing – to better match deposit growth to lending growth. Finally, they have access to the RBA “emergency” fund if needed – The Committed Liquidity Facility (CLF).

The Reserve Bank is providing a Committed Liquidity Facility (CLF) as part of Australia’s implementation of the Basel III liquidity standards from 1 January 2015. Consistent with the standards, certain authorised deposit-taking institutions (ADIs) are required by APRA to maintain a liquidity coverage ratio (LCR) at or above 100 per cent. These ADIs may seek approval from APRA to meet part of their Australian dollar liquidity requirements through a CLF with the Reserve Bank. In consideration of the Reserve Bank’s CLF commitment to an ADI, the ADI must pay a monthly CLF Fee in advance to the Reserve Bank.

Industry insiders estimate the capacity of the facility could be as high as $300 billion, a substantial amount. In effect the banks are backed by a Government guarantee.

So, we think that the wash through of these international issues will not create major financial stability problems locally, but there may well be higher costs to savers and borrowers, and potentially Australian tax payers, if the RBA is called on to assist with liquidity, or worst case the deposit insurance scheme is called upon if a bank were to get into difficulty. Currently deposits up to $250,000 in ADI’s supervised by APRA are covered.

Two other points to highlight. First, household savings ratio are on their way down, from their highs post GFC. We would expect households to hunker down and save more if there was an external shock, thus bolstering bank deposits (and a likely flight to quality, as we saw in the GFC). We do not think a run on an Australian bank is likely.

Second, bank net margins are compressing thanks to the severe competition in mortgage lending. This dynamic may change if there was an external shock, as demand for mortgages eased, providing some relief.

Second, bank net margins are compressing thanks to the severe competition in mortgage lending. This dynamic may change if there was an external shock, as demand for mortgages eased, providing some relief.

In addition the US Australian dollar exchange rate would probably drop, providing some relief. However, second order impacts, namely slowing economic activity, falls in confidence, and rising unemployment which may follow from a global shock, in turn have the potential to impact the banks much more, because it would translate into risks in the housing sector basket, where they have been placing their eggs in recent times.

In addition the US Australian dollar exchange rate would probably drop, providing some relief. However, second order impacts, namely slowing economic activity, falls in confidence, and rising unemployment which may follow from a global shock, in turn have the potential to impact the banks much more, because it would translate into risks in the housing sector basket, where they have been placing their eggs in recent times.