The federal government has announced a $600 million fighting fund to support the recommendations of the financial services royal commission, via InvestorDaily.

Buried on page 167 of the hefty 2019 Federal Budget are the Hayne-related expenses to be incurred by Treasury over the next five years.

The government will provide $606.7 million over five years from 2018-19 to facilitate its response to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

The package comprises a suite of measures that fulfil the government’s commitment to take action on all 76 of the recommendations of the Royal Commission’s Final Report, including:

• Designing and implementing an industry funded compensation scheme of last resort for consumers and small business ($2.6 million over two years from 2019-20);

• Providing the Australian Financial Complaints Authority with additional funding to help establish a historical redress scheme to consider eligible financial complaints dating back to 1 January 2008 ($2.8 million in 2018-19);

• Paying compensation owed to consumers and small businesses from legacy unpaid external dispute resolution determinations ($30.7 million in 2019-20);

• Resourcing the Australian Securities and Investments Commission (ASIC) to implement its new enforcement strategy and expand its capabilities and roles in accordance with the recommendations of the Royal Commission ($404.8 million over four years from 2019-20).

• Resourcing the Australian Prudential Regulation Authority (APRA) to strengthen its supervisory and enforcement activities which will support its response to key areas of concern raised by the Royal Commission, including with respect to governance, culture and remuneration ($145.0 million over four years from 2019-20);

• Establishing an independent financial regulator oversight authority, to assess and report on the effectiveness of ASIC and APRA in discharging their functions and meeting their statutory objectives ($7.7 million over three years from 2020-21);

• Undertaking a capability review of APRA, which will examine its effectiveness and efficiency in delivering its statutory mandate, as well as its capability to respond to the Royal Commission ($1.0 million in 2018-19);

• Establishing a Financial Services Reform Implementation Taskforce within the Treasury to implement the Government’s response to the royal commission, and co-ordinate reform efforts with APRA, ASIC and other agencies through an implementation steering committee ($11.2 million in 2019-20); and

• Providing the Office of Parliamentary Counsel with additional funding for the volume of legislative drafting that will be required to implement the Government’s response to the Royal Commission ($0.9 million in 2019-20).

The cost of this measure will be partially offset by revenue received through ASIC’s industry funding model and increases in the APRA Financial Institutions Supervisory Levies and from funding already provisioned in the Budget.

Lower taxes

Handing down the Federal Budget 2019-2020 in parliament last night, Mr Frydenberg said that the budget would restore the nation’s finances without raising taxes.

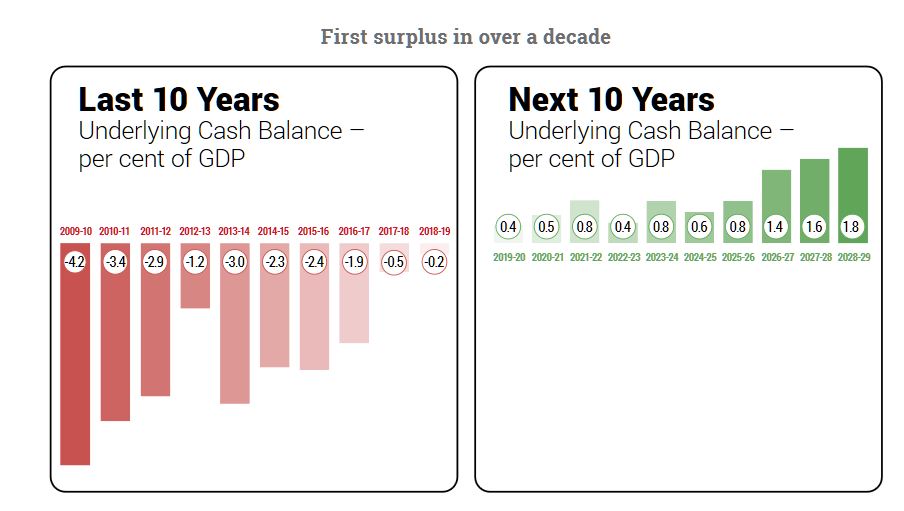

“The budget is back in the black and Australia is back on track,” the treasurer said, announcing that the coalition delivered a $7.1 billion surplus.

“Over the last year the interest bill on national debt was $18 billion,” he said. “We are reducing the debt and this interest bill, not by higher taxes, but by good financial management and growing the economy.”

The government has announced immediate tax relief for low- and middle‑income earners of up to $1,080 for singles or up to $2,160 for dual income families to ease the cost of living.

The coalition will also be lowering the 32.5 per cent rate to 30 per cent in 2024-25, increasing the reward for effort by ensuring a projected 94 per cent of taxpayers will face a marginal tax rate of no more than 30 per cent.

“The Australian Government is lowering taxes for working Australians and backing small and medium‑sized business, while ensuring all taxpayers, including big business and multinationals, pay their fair share,” the treasurer said.

Superannuation

The Government will allow voluntary superannuation contributions (both concessional and non-concessional) to be made by those aged 65 and 66 without meeting the work test from 1 July 2020. People aged 65 and 66 will also be able to make up to three years of non-concessional contributions under the bring-forward rule.

Those up to and including age 74 will be able to receive spouse contributions, with those 65 and 66 no longer needing to meet a work test.

“This measure is estimated to reduce revenue by $75.0 million over the forward estimates period,” the treasurer said.

“Currently, people aged 65 to 74 can only make voluntary superannuation contributions if they self-report as working a minimum of 40 hours over a 30 day period in the relevant financial year. Those aged 65 and over cannot access bring-forward arrangements and those aged 70 and over cannot receive spouse contributions.”

The government will make permanent the current tax relief for merging superannuation funds that is due to expire on 1 July 2020.

“This measure is estimated to have an unquantifiable reduction in revenue over the forward estimates period,” Mr Frydenberg said.

Since December 2008, tax relief has been available for superannuation funds to transfer revenue and capital losses to a new merged fund, and to defer taxation consequences on gains and losses from revenue and capital assets.

The tax relief will be made permanent from 1 July 2020, ensuring superannuation fund member balances are not affected by tax when funds merge. It will remove tax as an impediment to mergers and facilitate industry consolidation, consistent with the recommendation of the Productivity Commission’s final report into the superannuation industry.

The treasurer said consolidation would help address inefficiencies by reducing costs, managing risks and increasing scale, leading to improved retirement outcomes for members.

The government will also reduce costs and simplify reporting for superannuation funds by streamlining some administrative requirements for the calculation of exempt current pension income (ECPI).

The Government will allow superannuation fund trustees with interests in both the accumulation and retirement phases during an income year to choose their preferred method of calculating ECPI.

The Government will also remove a redundant requirement for superannuation funds to obtain an actuarial certificate when calculating ECPI using the proportionate method, where all members of the fund are fully in the retirement phase for all of the income year.

This measure will start on 1 July 2020 and is estimated to have no revenue impact over the forward estimates period.

FSC has mixed feelings

The Financial Services Council (FSC) welcomed the government’s superannuation changes to reduce red tape and improve access to voluntary contributions.

“The expansion of the work test exemption, spouse contributions and bring-forward arrangements will provide workers nearing retirement greater flexibility to make additional super contributions if they are able. The electronic requests for release of super and simplification of exempt current pension income calculations are sensible and welcome,” FSC chief executive Sally Loane said.

“The FSC also supports the tax relief for merging super funds, as this will help the superannuation industry consolidate to reduce costs and improve member outcomes.”

However, the FSC is disappointed this is not part of a comprehensive product rationalisation scheme, despite this being a longstanding government commitment.

“A lack of reform in this area means consumers are locked into older, more expensive products,” Ms Loane said.

The FSC is pleased to note the Budget has largely kept the superannuation settings unchanged. However, Ms Loane said the council is disappointed the government has failed to reform non-resident withholding tax for managed funds in the Asia Region Funds Passport.

“This means Australia will remain uncompetitive in our region, and Australia will not be competing with Asian funds on a level playing field.

“The withholding tax on managed funds raises little money, but harms our competitiveness within Asia, putting Australia’s fund managers at a major competitive disadvantage in the region.”