The IMF have published a paper on Fintech. From artificial intelligence to cryptography, rapid advances in digital technology are transforming the financial services landscape, creating opportunities and challenges for consumers, service providers, and regulators alike. This paper reviews developments in this new wave of technological innovations, often called “fintech,” and assesses their impact on an array of financial services. Given the IMF’s mandate to promote the stability of the international monetary system, it focuses on rapidly changing cross-border payments.

Using an economic framework, the paper discusses how fintech might provide solutions that respond to consumer needs for trust, security, privacy, better services, and change the competitive landscape. The key findings include the following:

Using an economic framework, the paper discusses how fintech might provide solutions that respond to consumer needs for trust, security, privacy, better services, and change the competitive landscape. The key findings include the following:

- Boundaries are blurring among intermediaries, markets, and new service providers.

- Barriers to entry are changing, being lowered in some cases but increased in others, especially if the emergence of large closed networks reduces opportunities for competition.

- Trust remains essential, even as there is less reliance on traditional financial intermediaries, and more on networks and new types of service providers.

- Technologies may improve cross-border payments, including by offering better and cheaper services, and lowering the cost of compliance with anti-money laundering and combating the financing of terrorism (AML/CFT) regulation.

Overall, the financial services sector is poised for change. But it is hard to judge whether this will be more evolutionary or revolutionary. Policymaking will need to be nimble, experimental, and cooperative.

When you send an email, it takes one click of the mouse to deliver a message next door or across the planet. Gone are the days of special airmail stationery and colorful stamps to send letters abroad.

International payments are different. Destination still matters. You might use cash to pay for a cup of tea at a local shop, but not to order tea leaves from distant Sri Lanka. Depending on the carrier, the tea leaves might arrive before the seller can access the payment.

All of this may soon change. In a few years, cross-border payments and transactions could become as simple as sending an email.

Financial technology, or Fintech, is already touching consumers and businesses everywhere, from a local merchant seeking a loan, to the family planning for retirement, to the foreign worker sending remittances home.

But can we harness the potential while preparing for the changes? That is the purpose of the paper published today by IMF staff, Fintech and Financial Services: Initial Considerations.

The possibilities of Fintech

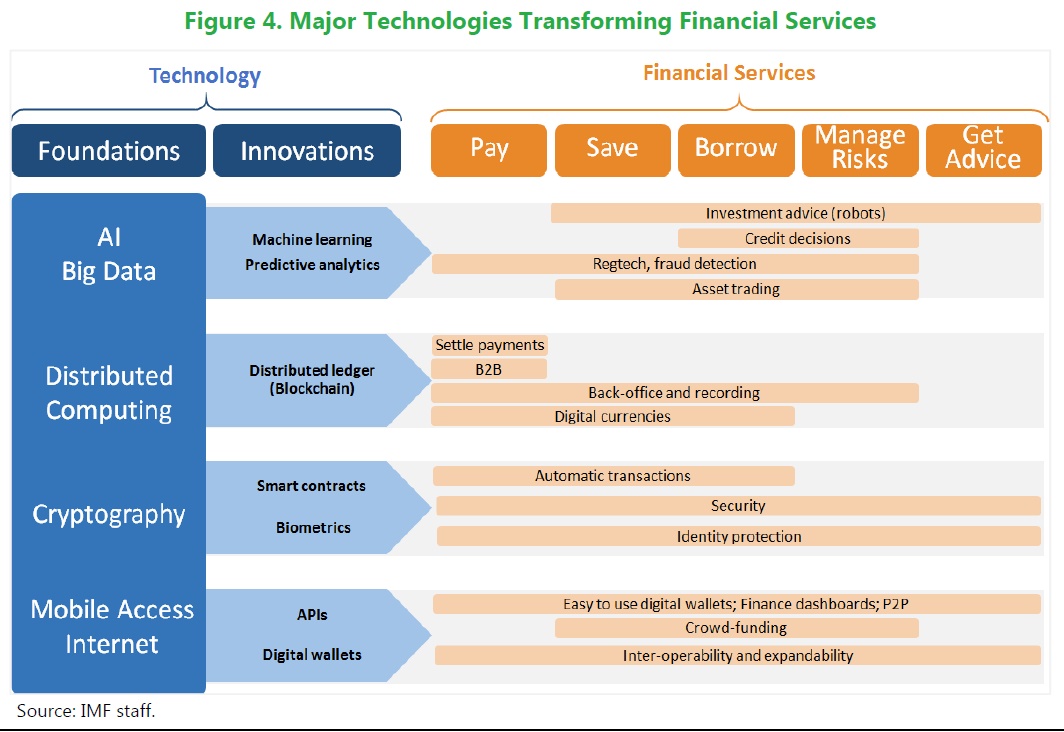

What is Fintech precisely? Put simply, it is the collection of new technologies whose applications may affect financial services, including artificial intelligence, big data, biometrics, and distributed ledger technologies such as blockchains.

While we encourage innovation, we also need to ensure new technologies do not become tools for fraud, money laundering and terrorist financing, and that they do not risk unsettling financial stability.

Although technological revolutions are unpredictable, there are steps we can take today to prepare.

The new IMF research looks at the potential impact of innovative technologies on the types of services that financial firms offer, on the structure and interaction among these firms, and on how regulators might respond.

As our paper shows, Fintech offers the promise of faster, cheaper, more transparent and more user-friendly financial services for millions around the world.

The possibilities are exciting.

- Artificial intelligence combined with big data could automate credit scoring, so that consumers and businesses pay more competitive interest rates on loans.

- “Smart contracts” could allow investors to sell certain assets when pre-defined market conditions are satisfied, enhancing market efficiency.

- Armed with mobile phones and distributed ledger technology, individuals around the world could pay each other for goods and services, bypassing banks. Ordering tea leaves from abroad might become as easy as paying for a cup of tea next door.

These opportunities are likely to reshape the financial landscape to some degree but will also bring risks.

Intermediaries, so common to financial services—such as banks, firms specialized in messaging services, and correspondent banks clearing and settling transactions across borders—will face significant competition.

New technologies such as identity and account verification could lower transaction costs and make more information available on counterparties, making middlemen less relevant. Existing intermediaries may be pushed to specialize and outsource well-defined tasks to technology companies, possibly including customer due-diligence.

But we cannot ignore the potential advances in technology that might compromise consumer identities, or create new sources of instability in financial markets as services become increasingly automated.

Rules that will work effectively in this new environment might not look like today’s rules. So, our challenge is clear—how can we effectively build new regulations for a new system?

Regulating without stifling innovation

First, oversight needs to be reimagined. Regulators now focus largely on well-defined entities, such as banks, insurance companies and brokerage firms. They may have to complement this focus with more attention on specific services, regardless of which market participants offers them. Rules would be needed to ensure sufficient consumer safeguards, including privacy protection, and to guard against money laundering and terrorist financing.

Second, international cooperation will be critical, because advances in technology know no borders, and it will be important to keep networks from moving to less regulated jurisdictions. New rules will need to clarify the legal status and ownership of digital tokens and assets.

Finally, regulation should continue to function as an essential safeguard to build trust in the stability and security of the networks and algorithms.

The launch or our paper today is one of the steps in the process of preparing for this new digital revolution. As an organization with a fully global membership, the IMF is uniquely positioned to serve as a platform for discussions among the private and public sectors on the rapidly evolving topic of Fintech.

As our research shows, adapting is not only possible, but it is the only way to ensure that the promise of Fintech is enjoyed by everybody