This time, in our occasional series where we feature Australian Fintech’s, we caught up with Co-Founder & Co-CEO of Lodex, Michael Phillipou.

Imagine the possibility of checking if the loan you have at the moment is the best available, in all but real-time, with no impact on your credit score. That’s the promise offered by Fintech Lodex, which launched a few weeks ago.

At first glance Lodex looks like a typical consumer loan auction site where you specify your finance requirement, be it for a home loan, car loan or personal loan. You register and complete some details via their platform, in around 10 minutes; then anonymously, and for free receive later a range of quotations from lenders, based on your profile and need, over the following 4 days. The anonymous submission means your credit score is unaffected.

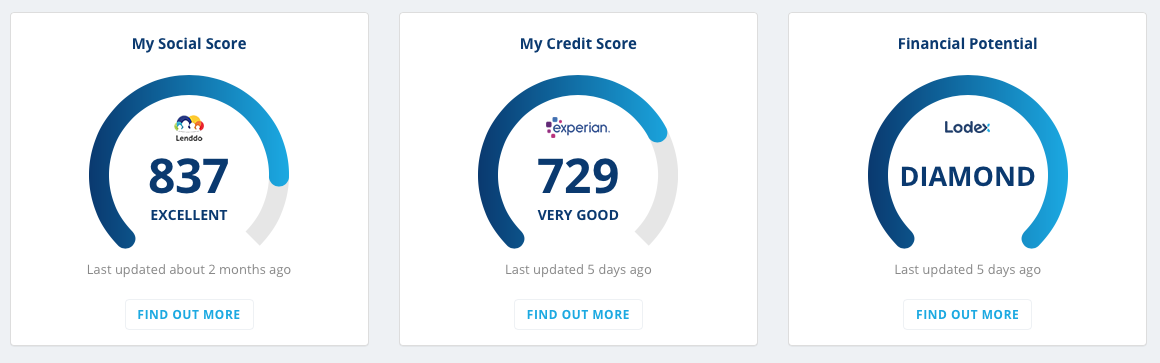

Below the hood, Lodex provides registered users with their credit score, courtesy of Experian, and by using an Australian first “social score” from their tie-up with Lenddo, which uses non-traditional data based around 12,000 parameters to derive an alternative to a traditional credit score.

When a consumer places a request, lenders or brokers on the platform will receive an alert via email, SMS or on their Lodex dashboard, based on their pre-set requirements. Many of the 90 broker groups on the platform at the moment, plus some smaller lenders, have implemented profiles which enable them to generate automated responses in near real time, while others choose to make a manual assessment as to whether to respond. Once the responses are in, the Lodex user can then choose which, if any of the bids to progress, and choose to share their information with the lender. Lodex, other than getting a referral fee from the broker or lender, drops out.

When a consumer places a request, lenders or brokers on the platform will receive an alert via email, SMS or on their Lodex dashboard, based on their pre-set requirements. Many of the 90 broker groups on the platform at the moment, plus some smaller lenders, have implemented profiles which enable them to generate automated responses in near real time, while others choose to make a manual assessment as to whether to respond. Once the responses are in, the Lodex user can then choose which, if any of the bids to progress, and choose to share their information with the lender. Lodex, other than getting a referral fee from the broker or lender, drops out.

Since launch Lodex have around 1,800 registered users, and have had around $55 million of loans requested, home loans being the largest share by value, but unsecured personal loans the largest by volume.

But what makes this platform unique is the possibility that current borrowers can benchmark their existing loans using the platform, to test whether they have the best possible deal. This is a game changer. Because there is no charge to register, the only downside is the short amount of time required to build your profile. But the potential is there to find the best loan available, and then choose whether to switch, or stick. Think of it as a market based loan health check.

Co-Founders & Co-CEO of Lodex, Michael Phillipou (Left) and Bill Kalpouzanis

Co-Founders & Co-CEO of Lodex, Michael Phillipou (Left) and Bill Kalpouzanis

Lodex currently have around 8 people in the team, and co-founders and banking executives Michael Phillipou and Bill Kalpouzanis have plans to take Lodex to other geographies, particularly South East Asia and Europe, which have similar distribution and regulatory frameworks, assisted by Lenddo’s coverage in more than 20 countries, and are also to add into the platform consumer credit cards and unsecured short term loans, as well as savings accounts and term deposits.

They have a strong Advisory Board includes chairman Andrew McEvoy, a former executive at Fairfax Media and managing director of Tourism Australia; marketing and advertising adviser Sean Cummins, the global CEO of Cummins and Partners; strategy adviser Kimberly Gire, a former CFO of retail & business bank at Westpac; and strategy adviser Francesco Placanica, the former CTO of Commonwealth Bank.

So, do not be deceived, this is genuinely an important evolution of lending and puts consumers back in the driving seat. It does break the lending mould.