The ABS released their housing finance data to October 2017 yesterday.

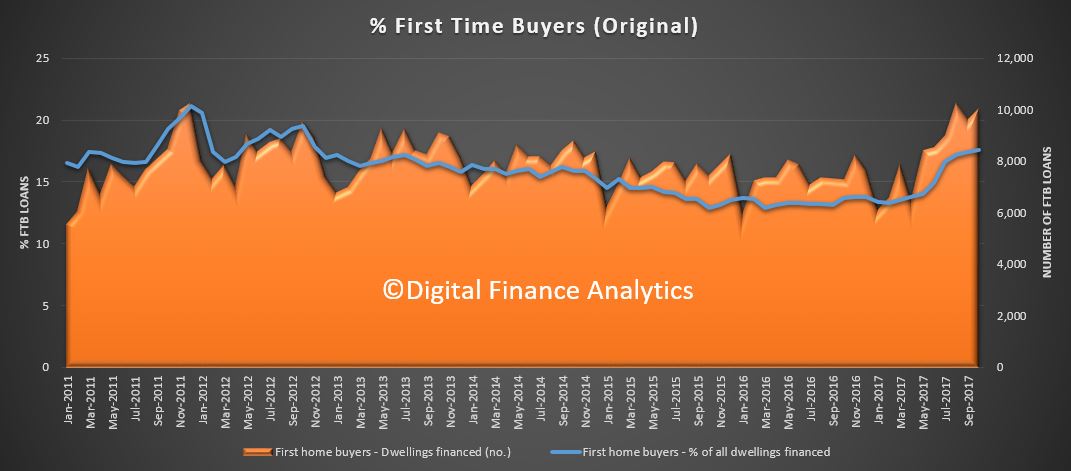

Overall lending was pretty flat, but first time buyers lifted in response to the increased incentives in some states, by 4.5% in original terms to 10,061 new loans nationally.

At a state level, FTB’s accounted for a 19% per cent share in Victoria and 13.7% in New South Wales, where in both states, more favourable stamp duty regime and enhanced grants were introduced this year. But, other states showed a higher FTB share, with NT at 24.8%, WA at 24.6%, ACT at 20.1% and QLD 19.7%. SA stood at 13% and TAS at 13.3%.

There was a shift upward shift in the relative numbers of first time buyers compared with other buyers (17.6% compared with 17.4% last month) , still small beer compared with the record 31.4% in 2009. These are original numbers, so they move around each month.

There was a shift upward shift in the relative numbers of first time buyers compared with other buyers (17.6% compared with 17.4% last month) , still small beer compared with the record 31.4% in 2009. These are original numbers, so they move around each month.

The number of first time buyer property investors slipped a little, using data from our household surveys, down 0.8% this past month. Together with the OO lift, but total first time buyer participation has helped support the market.

The number of first time buyer property investors slipped a little, using data from our household surveys, down 0.8% this past month. Together with the OO lift, but total first time buyer participation has helped support the market.

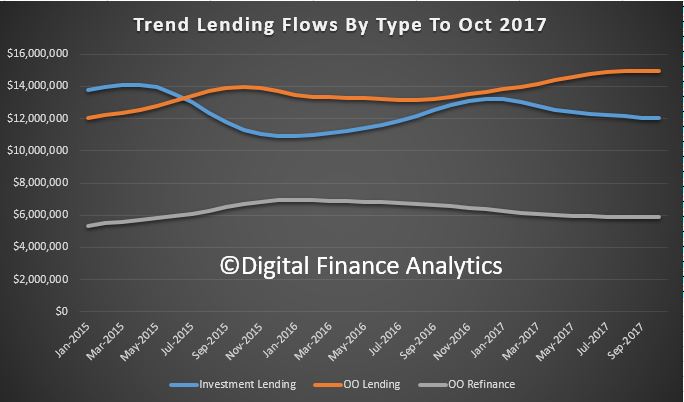

![]() Looking across the data, the trend estimate for the total value of dwelling finance commitments excluding alterations and additions fell 0.3%. Owner occupied housing commitments fell 0.1% and investment housing commitments fell 0.5%. However, in seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions rose 0.6%.

Looking across the data, the trend estimate for the total value of dwelling finance commitments excluding alterations and additions fell 0.3%. Owner occupied housing commitments fell 0.1% and investment housing commitments fell 0.5%. However, in seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions rose 0.6%.

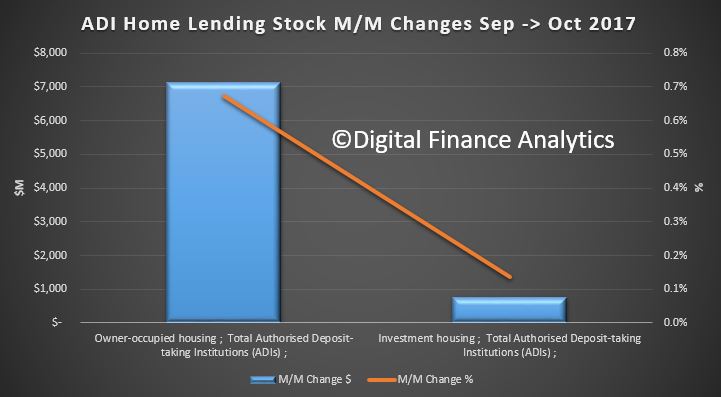

The monthly flows show that owner occupied lending fell $23m compared with the previous month, down 0.15%, while investment lending flows fell 0.5%, down $60m in trend terms. Refinanced loans slipped 0.13% down $7.5 million. The proportion of loans excluding refinanced loans for investment purposes slipped from a recent high of 53.4% in January 2015, down to 44.6% (so investment property lending is far from dead!)

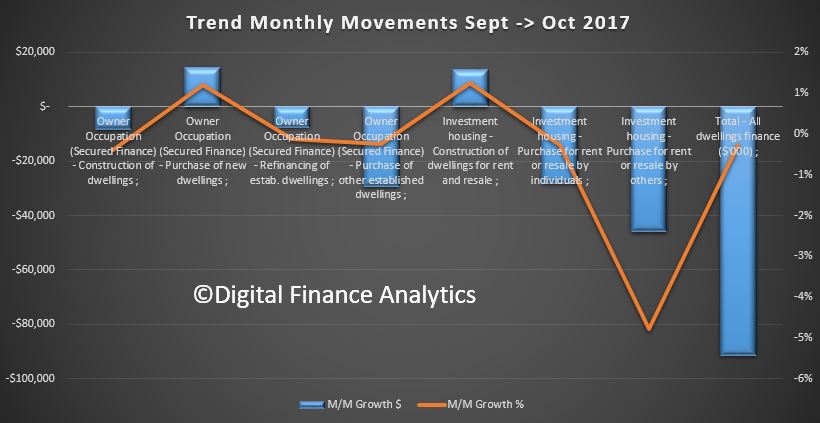

Here is the breakout by category.

Here is the breakout by category.

We see that from a trend monthly perspective, only secured finance for owner occupied purchase of new dwellings, and construction for rent rose.

We see that from a trend monthly perspective, only secured finance for owner occupied purchase of new dwellings, and construction for rent rose.

In trend terms, the number of commitments for the purchase of new dwellings rose 1.0% and the number of commitments for the purchase of established dwellings rose 0.3% while the number of commitments for the construction of dwellings fell 0.5%.

In trend terms, the number of commitments for the purchase of new dwellings rose 1.0% and the number of commitments for the purchase of established dwellings rose 0.3% while the number of commitments for the construction of dwellings fell 0.5%.

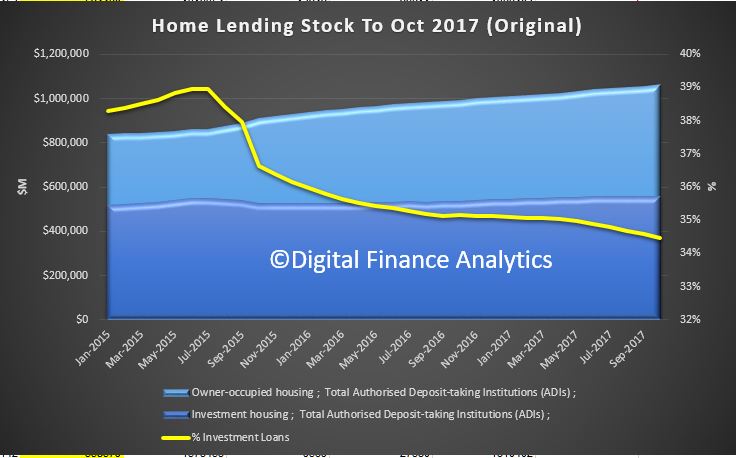

The stock data shows the value of all loans rose 0.49% or $7.8 billion (still an annual equivalent rate of three times income or inflation). Investor stock was 34.5% of all loans, slightly down from last month, but still a substantial proportion of the total.

The stock data (in original terms) showed a 0.67% rise in owner occupied loans worth around $7.1 billion and investor loans rose by 0.14% of $764 million.

The stock data (in original terms) showed a 0.67% rise in owner occupied loans worth around $7.1 billion and investor loans rose by 0.14% of $764 million.

So, overall the market is being supported by first time buyers, and some refinancing, reflecting the attractor rates currently on offer and recent incentives. But the fact is overall housing debts are rising, creating problems later as household debt rises, relative to income.

So, overall the market is being supported by first time buyers, and some refinancing, reflecting the attractor rates currently on offer and recent incentives. But the fact is overall housing debts are rising, creating problems later as household debt rises, relative to income.

Worth also highlighting that many will not see their property lift in value, if the trends in Sydney continue and spread. So many first time buyers are coming in close to the top and when wages are static. So it is important to allow sufficient capacity to handle these risks and that underwriting standards are adjusted accordingly. Trends here continue to mirror events in the USA in 2005/6. Caveat Emptor!