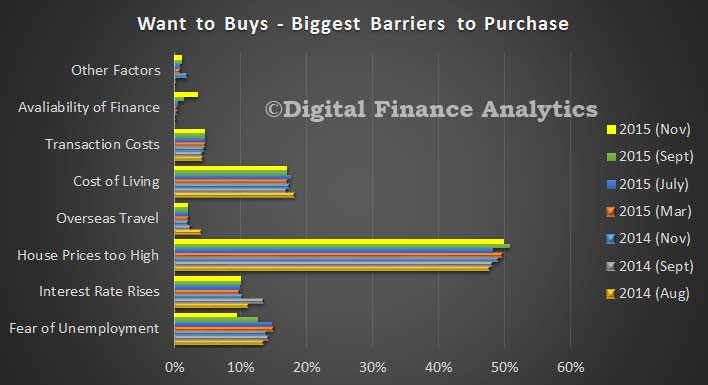

Continuing our analysis of the latest DFA household survey of property drivers and expectations, today we look at the First Time Buyer segment. For those wanting to buy, but are unable to do so, the main barriers remain high house prices, and costs of living (no surprise given static real income growth). However, we also see a spike in availability of funding as a barrier, compared with a couple of months ago. Lending criteria may be getting tighter for some. We also see fears of unemployment receding in the eastern states, though it was a little higher this time in WA.

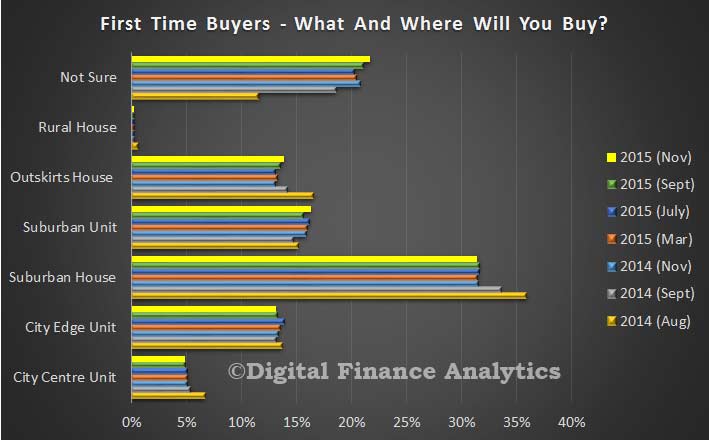

So then, looking at those who are actively seeking to buy for the first time, more than 20% are unsure of the type of property they can find. Overall houses, are preferred but we see units very much in the frame, especially in the eastern states, in and around the main urban centres. There are more units available (resale and new construction) than houses in these areas, and prices for units will be a little lower.

So then, looking at those who are actively seeking to buy for the first time, more than 20% are unsure of the type of property they can find. Overall houses, are preferred but we see units very much in the frame, especially in the eastern states, in and around the main urban centres. There are more units available (resale and new construction) than houses in these areas, and prices for units will be a little lower.

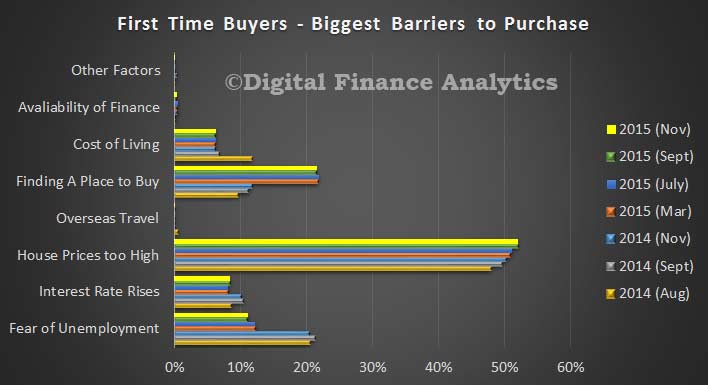

For those actively seeking to buy for the first time, prices are the major barrier, most seem able still to get finance if they do find a place to buy.

For those actively seeking to buy for the first time, prices are the major barrier, most seem able still to get finance if they do find a place to buy.

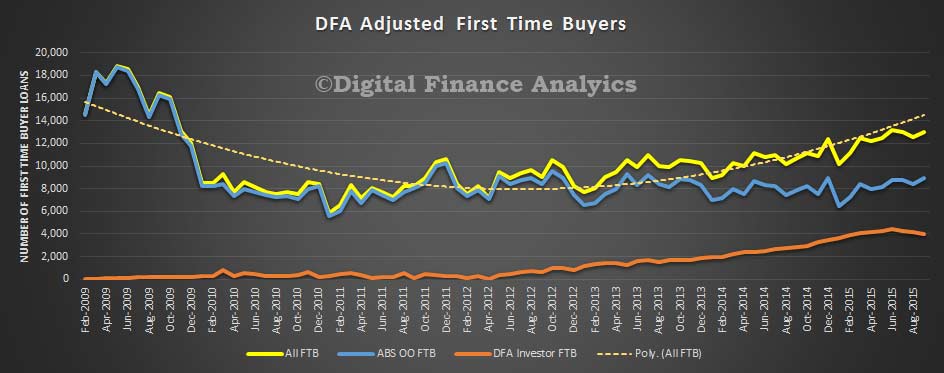

One final perspective, from our earlier research, we are seeing some reduction in the absolute number of first time buyers going direct to the investment sector (the red line), but it is still a very significant factor. It is still a logical approach for some, to gain access to the housing market, perhaps by buying a cheaper place to rent and hoping for capital gains and tax breaks, though of course interest rates have risen in the investment mortgage sector, and prospective buyers are likely to be buying into very full (some would say precarious) prices. For many it is a dilemma, will prices continue to rise (in which case they need to get in now) or will prices begin to correct (in which case it is better to wait, to avoid the pitfalls of negative equity)? Given yesterday’s comments, waiting a bit may be the more sensible path as the property worm is turning, especially in the eastern states.

One final perspective, from our earlier research, we are seeing some reduction in the absolute number of first time buyers going direct to the investment sector (the red line), but it is still a very significant factor. It is still a logical approach for some, to gain access to the housing market, perhaps by buying a cheaper place to rent and hoping for capital gains and tax breaks, though of course interest rates have risen in the investment mortgage sector, and prospective buyers are likely to be buying into very full (some would say precarious) prices. For many it is a dilemma, will prices continue to rise (in which case they need to get in now) or will prices begin to correct (in which case it is better to wait, to avoid the pitfalls of negative equity)? Given yesterday’s comments, waiting a bit may be the more sensible path as the property worm is turning, especially in the eastern states.

More next time on the other segments in our surveys. You can read our last Property Imperative Report which summaries the state of play as at September 2015. This post updates some of the data in that report.

More next time on the other segments in our surveys. You can read our last Property Imperative Report which summaries the state of play as at September 2015. This post updates some of the data in that report.