Australia’s public debt ratios are likely to peak later – and at a higher level – than previously expected by the government and Fitch Ratings as the economic outlook weakens. However, the debt trajectory remains consistent with our ‘AAA’/Stable sovereign rating on Australia, most recently affirmed in September.

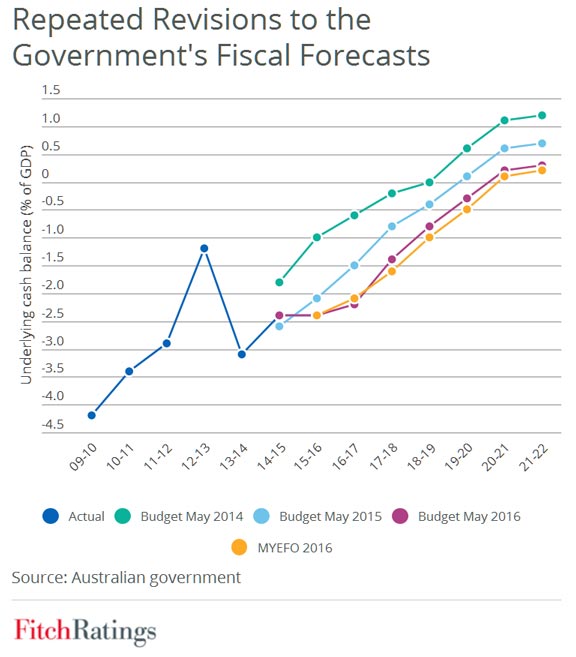

The government increased its budget deficit forecasts for the underlying cash balance by a cumulative AUD10.3bn (0.6% of GDP) for the next four years, largely owing to lower expectations for real GDP growth and wage inflation, according to its Mid-Year Economic and Fiscal Outlook (MYEFO), released on Monday. It also projected gross and net debt ratios would peak in FY19 (12 months to end-June), a year later than forecasted six months ago in the 2017 budget. That said, revisions were smaller than those that have been made in recent years, mainly in response to sharp falls in commodity prices.

Fitch still expects the government to reduce its deficit at a slower rate than official forecasts. The MYEFO abandons the practice of assuming commodity prices will remain at recent averages; instead, it factors in a steady decline from current levels, though using price assumptions that are still higher than our own. We also believe the government will find it hard to deliver on hitherto unlegislated spending cuts assumed in the MYEFO, worth a cumulative AUD13.2bn (0.8% of GDP) by FY20, given that the coalition government lacks a majority in the Senate. The government has made some progress on budget repair through the legislature since the July election, saving AUD6.3bn in the Omnibus Savings Bill and raising AUD4.7bn in revenues through increasing tobacco excise. However, forming a political consensus over the remaining measures will be considerably more challenging.

Fitch still expects the government to reduce its deficit at a slower rate than official forecasts. The MYEFO abandons the practice of assuming commodity prices will remain at recent averages; instead, it factors in a steady decline from current levels, though using price assumptions that are still higher than our own. We also believe the government will find it hard to deliver on hitherto unlegislated spending cuts assumed in the MYEFO, worth a cumulative AUD13.2bn (0.8% of GDP) by FY20, given that the coalition government lacks a majority in the Senate. The government has made some progress on budget repair through the legislature since the July election, saving AUD6.3bn in the Omnibus Savings Bill and raising AUD4.7bn in revenues through increasing tobacco excise. However, forming a political consensus over the remaining measures will be considerably more challenging.

General government debt is now likely to peak at a level slightly higher than the 40.4% of GDP that we forecast for FY18 at the time of our September review. This would still be broadly in line with the median public debt/GDP ratio for ‘AAA’-rated sovereigns, of 42%. However, the deterioration since 2007 – when general government debt was less than 10% of GDP – has eroded the sovereign’s buffer against shocks. A housing market downturn or another slowdown in the global economy, for example, could weigh on Australia’s rating if it resulted in further significant deterioration in public finances.

Australia’s fiscal outlook is sensitive to economic performance, a risk highlighted by the -0.5% qoq fall in Australia’s GDP in 3Q16, the first contraction in five years. Some of the factors behind the decline are likely to prove temporary – public investment fell sharply after a strong second quarter, construction activity was hampered by poor weather, and coal-mine disruption held back exports. Furthermore, the drag from falling mining investment should continue to fade in coming quarters, while real exports will be boosted by LNG projects reaching the production stage. However, last quarter’s data also showed a slowdown in consumer spending growth – in keeping with subdued wage gains – and continued weakness in non-mining investment. Fitch had previously expected the economy to expand 2.9% in 2016 and 2017, but those forecasts now face a higher risk of downside adjustments