Several industry participants have voiced concern over mortgage stress and the rising risk of defaults, as wage growth fails to keep pace with the costs of living.

Approximately 51,500 borrowers could be at risk of defaulting on their mortgages in the coming year, with over 30 per cent of Australians experiencing mortgage stress, finder.com.au has suggested, after analysing research from Digital Finance Analytics’ (DFA) Household Survey.

Speaking to Mortgage Business, the principal of DFA, Martin North, noted that “at risk” borrowers were most prevalent in mining-centred regions across Queensland and Western Australia. He added that “severe” mortgage stress could be on the rise in other parts of the country.

“There are more people currently at risk in Western Australia and in Queensland, which is an outfall from the mining downturn, but we’re also seeing a significant rise in severe stress in Western Sydney, on the outskirts of Melbourne and around Brisbane,” Mr North said.

“Defaults over the next two years are not necessarily going to be centred in the West or in Queensland, but we’re going to see some more significant risks in and around the main urban centres in Brisbane and Melbourne.”

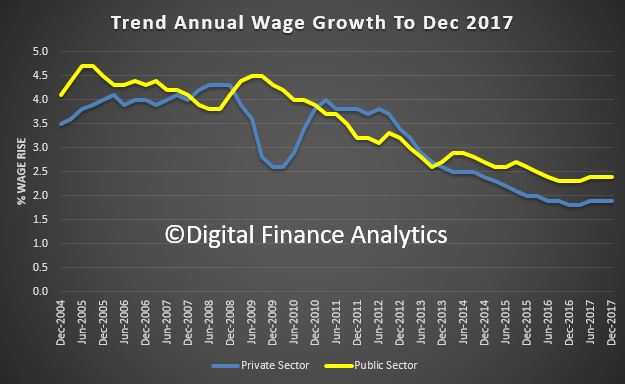

Mr North attributed the increased risk of mortgage defaults to slow wage growth, cost of living pressures and high mortgage repayment costs for borrowers that were issued with home loans prior to regulatory tightening.

The principal said: “There are a few drivers. The first is that incomes are not growing in real terms, particularly if you’re in the private sector. The income growth is on average 1.9 per cent. A lot of people haven’t had a pay rise in a long time, so income is compressed.

“Secondly, cost of living is rising and that includes everything from electricity bills, child-care costs, cost of fuel, [etc]. So, it’s the impact of incomes versus costs not going in the right direction.

“The third thing is that the costs of the mortgage, particularly in the major urban areas around Sydney and Melbourne, are a lot bigger because home prices have gone up a lot, so people are leveraged. They’ve got very large mortgages and very little wiggle room as a result.”

The market analyst also noted that a lack of financial awareness and household budgeting is to blame for rising levels of mortgage stress. Indeed, according to Mortgage Choice’s Financial Savviness Whitepaper, 54.9 per cent of Australians fail to review their finances at least once a week.

“The finding that more than one in two Australians are not checking their bank accounts on a weekly basis at minimum is quite alarming and it suggests that many people are keeping themselves in the dark when it comes to their finances,” CEO of Mortgage Choice John Flavell said.

The Mortgage Choice CEO added that “keeping a close eye” on finances could allow households to identify savings opportunities.

He said: “Keeping a close eye on your finances is essential in helping you better manage and understand where your money is going, where you can cut back on spending and improve your savings.

“When you know how much money you have available in your account, you will avoid overspending or withdrawing beyond your balance and being hit with an overdraft fee. Moreover, when you’re actively tracking your finances, you will benefit from having greater control and confidence to make decisions, whether they be small discretional expenses or a significant purchase such as a car or property.”

Mr Flavell continued: “[Being] aware of your spending patterns helps you catch any unusual expenses, fees or declined transactions you may not have otherwise been aware of.”

The topic of mortgage stress has been in the spotlight recently, after the Reserve Bank of Australia said that it was keeping a watchful eye on interest-only mortgagors whose terms are due to expire between this year and 2022, as it fears some may find the “step-up” to P&I repayments “difficult to manage”.

In her address to the Responsible Lending and Borrowing Summit this year, the assistant governor of the Reserve Bank of Australia (RBA), Michele Bullock, spoke about household indebtedness and mortgage stress.

Ms Bullock said that while mortgage stress has declined since 2011 (largely as a reflection of the fall in interest rates since that time) and that the number of those classed as being in some financial stress is “not growing rapidly”, around 12 per cent of owner-occupiers with mortgage debt indicated that they would expect difficulty raising funds in an emergency.

Noting that “the increasing popularity of interest-only loans over recent years meant that, by early 2017, 40 per cent of the debt did not require principal repayments”, the assistant governor said that “this presents a potential source of financial stress if a household’s circumstances were to take a negative turn”.

Ms Bullock noted that as a “large portion” of principal-free periods begin to expire, some borrowers may therefore struggle to service their mortgages.

She said: “[A] large proportion of interest-only loans are due to expire between 2018 and 2022. Some borrowers in this situation will simply move to principal and interest repayments as originally contracted.

“Others may choose to extend the interest-free period, provided that they meet the current lending standards. There may, however, be some borrowers that do not meet current lending standards for extending their interest-only repayments but would find the step-up to principal and interest repayments difficult to manage.

“This third group might find themselves in some financial stress. While we think this is a relatively small proportion of borrowers, it will be an area to watch.”