Whilst Genworth, as one of the two independent Lender’s Mortgage Insurers in Australia, will have a skewed mortgage portfolio compared with the market (higher Loan-to-Value (LVR) loans which the banks prefer not to cover internally), we get a good feel for the market from their results today. Whilst the proportion of new loans with a high LVR is falling, delinquencies are rising especially in the mining heavy states.

Now a public company, the level of disclosure from Genworth is useful. They reported statutory net profit after tax (NPAT) of $135.8 million for 1H16. After adjusting for the after-tax mark-to-market move in the investment portfolio of $22.9 million, underlying NPAT was $112.9 million.

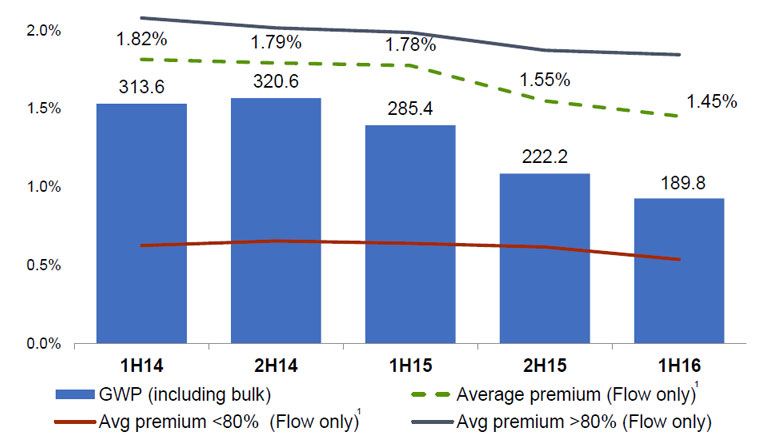

They show that Gross Written Premium declined 33.5% decreased 33.5% to $189.8 million in 1H16. The decline in GWP is consistent with the broader industry trend of a reduction in the proportion of mortgage originations above 90 per cent LVR. The result also reflects changes in the customer portfolio in 1H15.

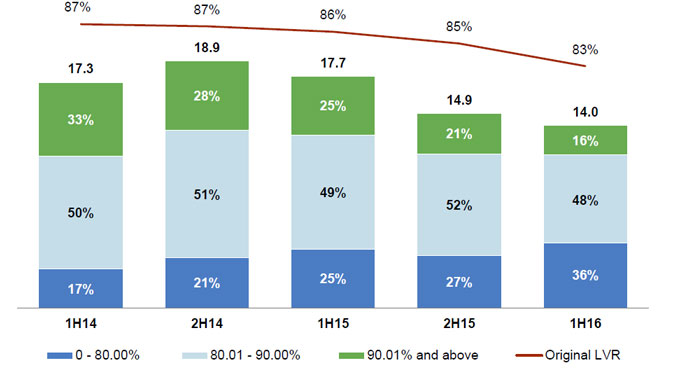

New Insurance Written decreased 20.9% to $14.0 billion in 1H16. NIW in the greater than 90% LVR segment decreased 49.1% while NIW in the less than 80% LVR segment increased 10.9%. The decline in the proportion of high loan-to-value loans originated reflects changes in lender risk appetite and focused regulatory oversight in the Australian mortgage market. The result also reflects changes in the customer portfolio in 1H15.

New Insurance Written decreased 20.9% to $14.0 billion in 1H16. NIW in the greater than 90% LVR segment decreased 49.1% while NIW in the less than 80% LVR segment increased 10.9%. The decline in the proportion of high loan-to-value loans originated reflects changes in lender risk appetite and focused regulatory oversight in the Australian mortgage market. The result also reflects changes in the customer portfolio in 1H15.

The Net Earned Premium increased 1.4% reflecting higher earned premium from prior book years and the benefit from the premium earnings pattern revision adopted since the second half of 2015.

The Net Earned Premium increased 1.4% reflecting higher earned premium from prior book years and the benefit from the premium earnings pattern revision adopted since the second half of 2015.

Net claims incurred increased due to an increase in the number of delinquent loans relative to a year ago and a higher average claim amount. The overall portfolio continues to be supported by strong performance in New South Wales and Victoria. However, the performance in Queensland and Western Australia is challenging, reflecting increased delinquencies, particularly in regions exposed to the slowdown in the resources sector.

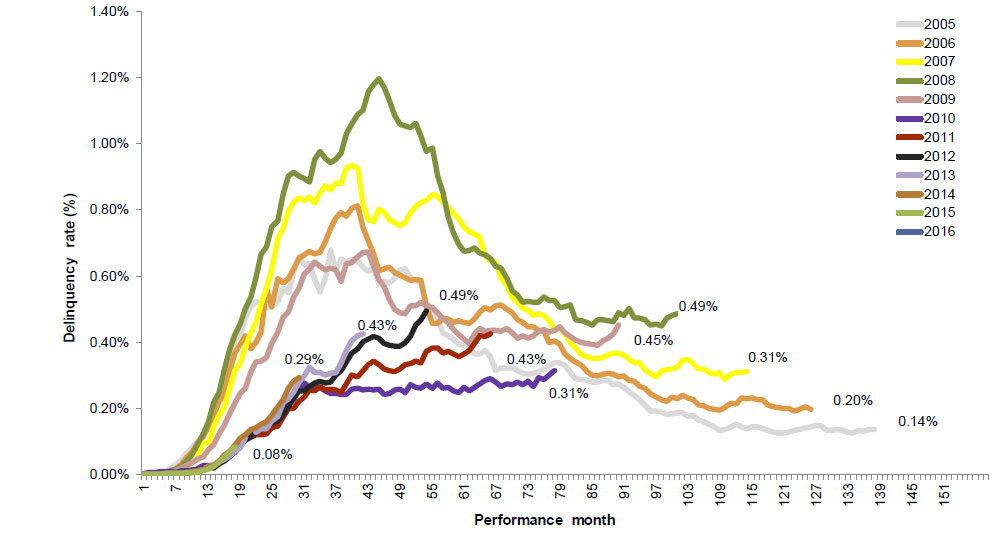

They showed an interesting evolution of Genworth’s 3 month+ delinquencies (Flow only) by residential mortgage loan book year from the point of policy issuance.

Each line illustrates the level of 3 month+ delinquencies relative to the number of months an LMI policy has been in-force for policies issued within a specific year.

Each line illustrates the level of 3 month+ delinquencies relative to the number of months an LMI policy has been in-force for policies issued within a specific year.

The 2008 Book Year was affected by the economic downturn experienced across Australia and heightened stress experienced among self-employed borrowers, particularly in Queensland, which was exacerbated by the floods in 2011.

The 2010 to 2015 Book Years are performing favourably relative to the previous five years (2005-2009). The recent increase in the 2012 and 2013 book years is due to increased delinquencies, mainly in parts of Queensland and Western Australia.

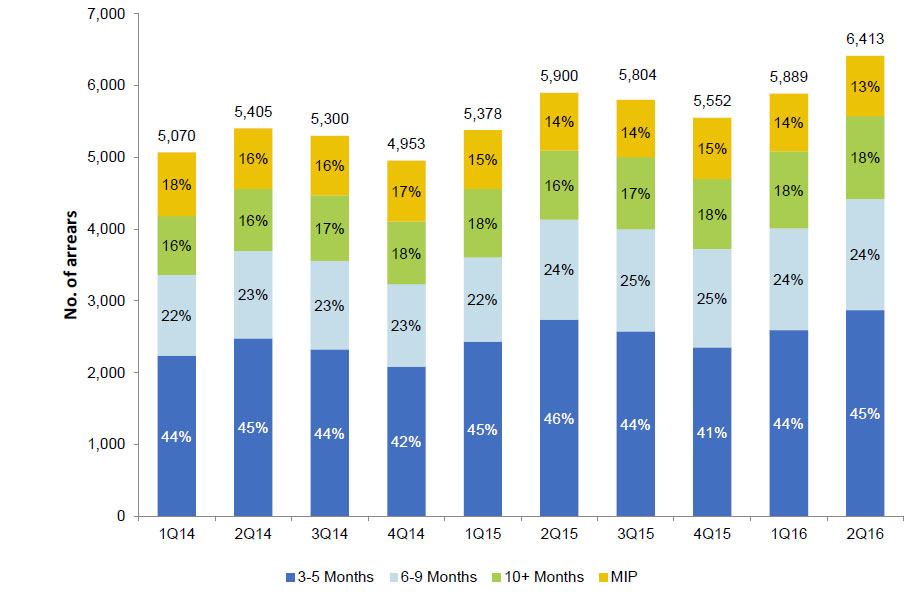

Finally, the delinquency population by months in arrears (MIA) aged bucket at the end of each reporting period. Over the past two years, the MIP percentage as a proportion of the total delinquency population has been trending down. This reflects strong housing market conditions and the low interest rate environment in which a mortgagee in possession (MIP) generally progresses faster to a claim, or sold with no claim situation, which in turn leads to a relatively lower claims pipeline. The 3-5 months MIA bucket, shows a seasonal uptick in the second quarter of each year, consistent with historical observed experience.

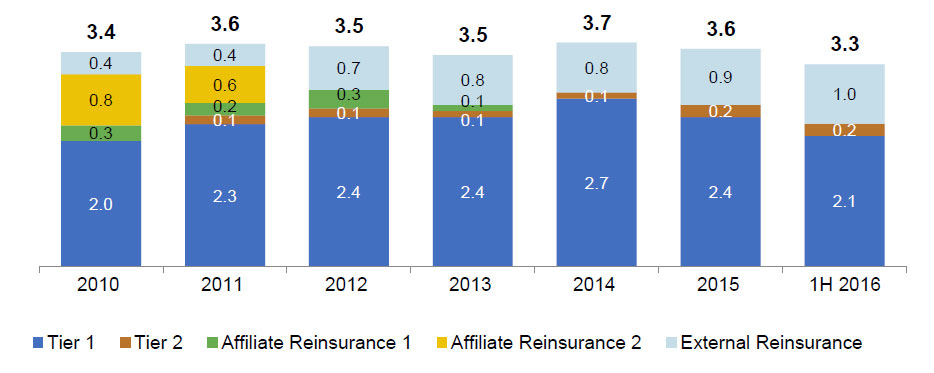

The Group’s capital position was strong as at 30 June 2016 with a regulatory capital solvency level of 1.56 times the Prescribed Capital Amount (PCA) on a Level 2 basis and a CET1 ratio of 1.43 times PCA. The decrease in CET1 capital reflects $114.9 million of dividends and the $202.4 million capital reduction paid to shareholders during 1H16, partially offset by $135.8 million reported NPAT. Tier 2 capital decreased due to the redemption of the remaining $49.6 million of the 2011 subordinated notes.

The Group’s capital position was strong as at 30 June 2016 with a regulatory capital solvency level of 1.56 times the Prescribed Capital Amount (PCA) on a Level 2 basis and a CET1 ratio of 1.43 times PCA. The decrease in CET1 capital reflects $114.9 million of dividends and the $202.4 million capital reduction paid to shareholders during 1H16, partially offset by $135.8 million reported NPAT. Tier 2 capital decreased due to the redemption of the remaining $49.6 million of the 2011 subordinated notes.