Lender’s Mortgage Insurer Genworth released their results to December 2016 today. From it, we get insights into the changing nature of the housing market, and also a view of the pressure LMI’s are under.

Genworth reported a statutory net profit after tax (NPAT) of $203.1m, down 10.9% on prior year. After adjusting for the after-tax mark-to-market move in the investment portfolio of $9.1m, underlying NPAT was $212.2m down 19.8% on prior year. The loss ratio was 35.1%, compared with 24% last year. They remain strongly capitalised, and though claims are higher, they declared a final fully franked dividend of $14.00, a FY16 payout ratio of 67.2%, but down from last half.

Banks are clearly writing less high LVR mortgages, thanks to APRA, and when households default, and are forced to sell, there is sufficient capital appreciation in most properties to avoid a LMI claim due to strong price rises. The banks, can’t loose! (Remember the LMI protects the bank, not the borrower). However, in regions where prices are falling – for example in the mining belts of WA and QLD, and home prices are falling, claims are up. This does not bode well if home prices were to revere more widely.

Genworth was listed in 2014, but since then has completed share buy-backs to reduce the number of issued shares. Further restructure will simplify the corporate structure in 2017, with a view to driving efficiency. They are the only separately listed LMI in Australia, (the banks have their own LMI captives, and the other player in the market is less transparent).

We will look at the market data they provided first, then look at the drivers of their results more specifically.

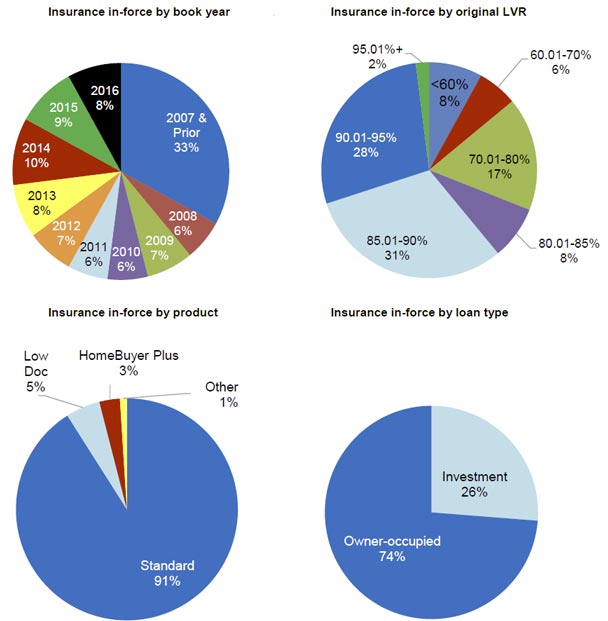

Genworth had an in-force portfolio of approximately $324 billion at Dec 2016. Standard LMI accounted for 91% of the book, and Low Doc 5%. 26% of the book relates to Investment loans.

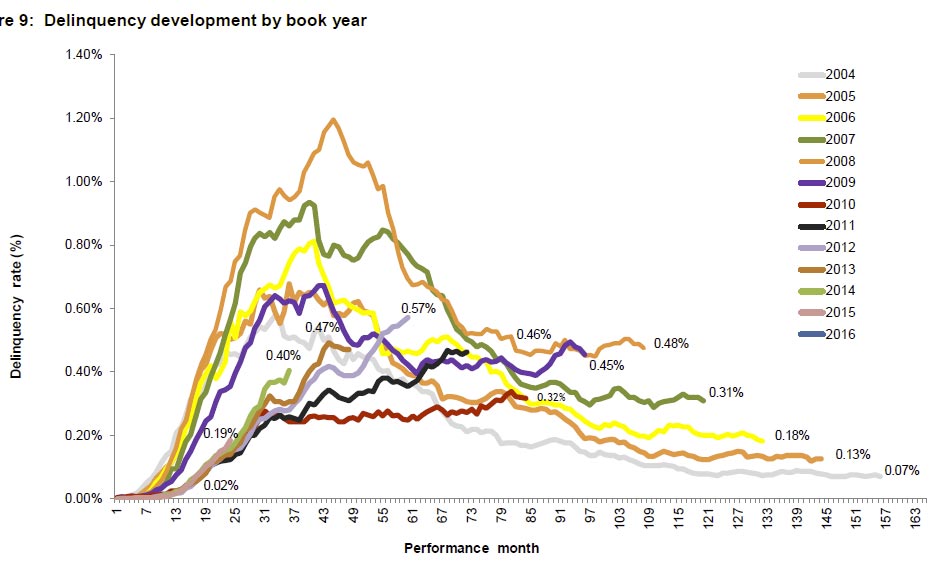

The seasoning picture is interesting. This shows the evolution of Genworth’s 3 month+ delinquencies (flow) by residential mortgage loan book year, from issue.

The seasoning picture is interesting. This shows the evolution of Genworth’s 3 month+ delinquencies (flow) by residential mortgage loan book year, from issue.

The delinquency population by months in arrears aged buckets shows that over the past two years, the mortgagee in possession (MIP) as a proportion of total delinquency is trending down. This is because the strong property market has allowed stressed households to sell and release equity, with no LMI claim.

The delinquency population by months in arrears aged buckets shows that over the past two years, the mortgagee in possession (MIP) as a proportion of total delinquency is trending down. This is because the strong property market has allowed stressed households to sell and release equity, with no LMI claim.

With regards to the current results, a range of factors influenced the lower outcomes.

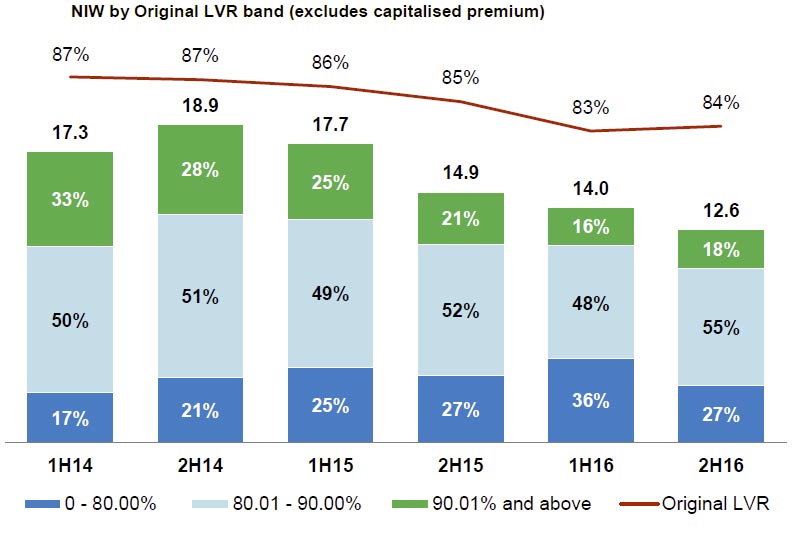

New Insurance Written (NIW) fell 18.4% in FY16, to $26.6 billion. Moreover, NIW above 90% LVR decreased 39.8%, and 80-90% LVR fell 17.2%. This reflects changing appetite among lenders for higher LVR business, following regulatory intervention from APRA.

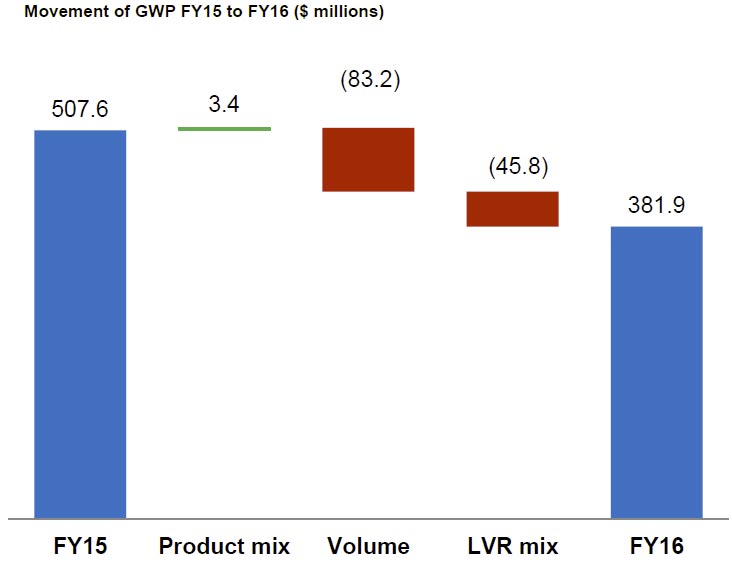

Lower Sales (Gross Written Premium – GWP) fell 24.8% compared to previous period due to the lower number of high loan-to-value (LVR) penetration in the market and a lower LVR mix of business.

Lower Sales (Gross Written Premium – GWP) fell 24.8% compared to previous period due to the lower number of high loan-to-value (LVR) penetration in the market and a lower LVR mix of business.

The average price for Flow (GWP/NIW) decreased from 1.63% to 1.51% in FY16. However, they got some benefit from premium repricing in the second half.

The average price for Flow (GWP/NIW) decreased from 1.63% to 1.51% in FY16. However, they got some benefit from premium repricing in the second half.

Lower Revenue (Net Earned Premium) – NEP fell 3.6% reflecting lower earned premiums from current and prior book years.

Higher Net Claims Incurred – Net claims incurred increased by $46.1 m to $158.8m due to an increase in the number of delinquent loans relative to a year ago, and a higher average claim amount. The performance in QLD and WA is “challenging”, reflecting increased delinquencies, especially in resource exposed regions. NSW and VIC were better performers. Overall, the delinquency rate rose from 0.38% to 0.46%.

Whilst financial income (interest income and realised and unrealised gains/losses) increased by $18.1 m, to $126.0 m in FY16, the yield on the investment portfolio dropped 3.69%.

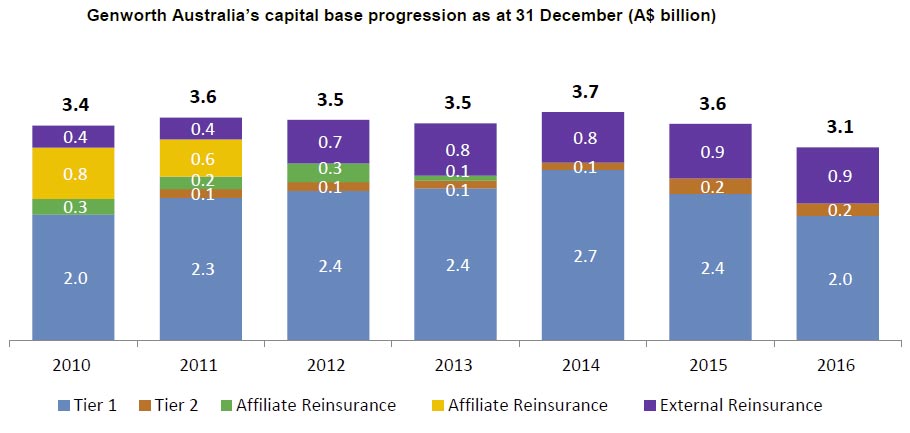

Regulatory capital fell from $2,600 m in 2015 to $2,213 m in 2016. CET1 decreased in FY16 mainly reflecting the $250 m of dividends, $202 m capital reduction and $86 m decrease in the excess technical provision, offset by $203 m NPAT. Tier 2 capital decreased following the redemption of $50 m of the $140 m notes issued. The PCA coverage ratio was consistent with FY15.