Last Monday, the Deutsche Bundesbank, Germany’s central bank, reported that residential real estate prices in German cities are overvalued by 15%-30% relative to fundamental measures of value, with the large cities at the upper end of the range (see Exhibit 1). Such overvaluation is credit negative for banks with concentrated retail mortgage books in urban areas, banks with large retail mortgage franchises and residential mortgage-backed securities (RMBS). Overvaluation creates the risk of losses if foreclosed properties backing mortgage loans are sold after a fall in house prices. The credit effect for covered bonds is limited owing to the statutory protection provided by Germany’s covered bond law (Pfandbrief Act).

For banks, the risk lies in their exposure to retail mortgages if a price correction occurs once interest rates rise materially, along with an acceleration in new housing loans originated in the past two years and margins that have shrunk. Although the combination of these factors in and of themselves do not immediately lead to higher defaults owing to the long-term fixed-rate nature of German residential mortgages, a lower recovery value following a price correction in a foreclosure would require the banks to increase cash provisions on defaulted exposures.

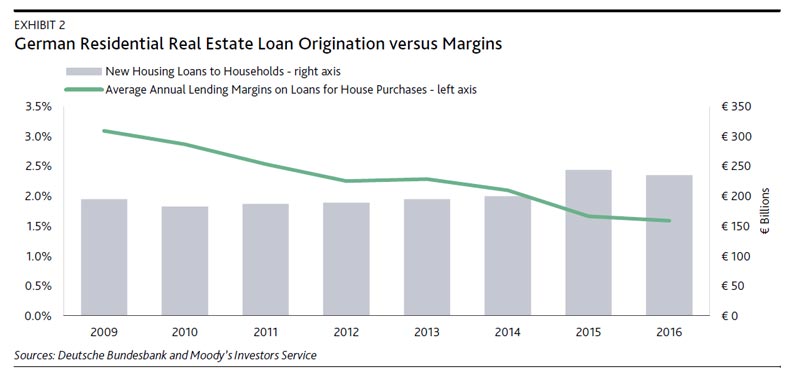

Bundesbank data also show that over the past two years, German banks have increased their new lending volumes by 20% versus the average origination volume during 2009-14 (see Exhibit 2). Hence, if residential property prices were to fall following an increase in interest rates or because of supply-demand imbalances, banks would face meaningful loan-loss provisions in case of default. If residential property prices were to retreat to 2010 levels, we would expect the share of loans with loan-to-value ratios (LTV) of more than 100% to increase to more than 40% of all outstanding mortgages.

RMBS would be negatively affected if house prices were to correct because loss severities (the proportion of the loan not covered by the proceeds from selling the property) would rise. German RMBS typically contain loans originated at high LTVs of 90%,6 on average, with some at above 100%. Deleveraging and house price increases in recent years have resulted in current market price LTVs averaging 55%.7 However, this ratio is primarily driven by one transaction (Pure German Lion RMBS 2008). For instance, EMAC-DE transactions and Kingswood Mortgages have LTVs of 80% on average.

The mortgage covered bonds of Sparkasse KoelnBonn and Hamburger Sparkasse (all rated Aaa) are most exposed to a potential correction of urban residential real estate prices. Both programs have a large share of residential and multifamily mortgage loans in the cover pools, and these issuers focus mortgage loan underwriting on urban areas. Nevertheless, German Pfandbrief are well protected against a potential fall in house prices. The 60% loan-to-lending-value threshold prescribed in the Pfandbrief Act ensures that only loan parts equal to the first 60% of a property’s lending value (defined in the act as the long-term sustainable property value excluding any speculative price components) are eligible for cover pools. The Pfandbrief Act also stipulates that property valuations are not adjusted upward after loan origination in case of property price increases, providing a buffer against price declines if borrowers default on their mortgage loans.