The Financial Stability Board (FSB) today published the Global Shadow Banking Monitoring Report 2016. The report presents the results of the FSB’s sixth annual monitoring exercise to assess global trends and risks in the shadow banking system, reflecting data up to the end of 2015. It covers 28 jurisdictions, including Belgium and the Cayman Islands for the first time. These jurisdictions together account for about 80% of global GDP.

The “shadow banking system” can broadly be described as “credit intermediation involving entities and activities (fully or partially) outside the regular banking system” or non-bank credit intermediation in short. Such intermediation, appropriately conducted, provides a valuable alternative to bank funding that supports real economic activity. But experience from the crisis demonstrates the capacity for some non-bank entities and transactions to operate on a large scale in ways that create bank-like risks to financial stability (longer-term credit extension based on short-term funding and leverage). Such risk creation may take place at an entity level but it can also form part of a chain of transactions, in which leverage and maturity transformation occur in stages, and in ways that create multiple forms of feedback into the regular banking system.

As part of the FSB’s strategy to address financial stability concerns associated with shadow banking and transform it into resilient market-based finance, the FSB has been conducting an annual system-wide monitoring to track developments in the shadow banking system. The monitoring exercise adopts the activity-based “economic function” approach where authorities narrow the focus to those parts of the non-bank financial sector where financial stability risks from shadow banking (such as maturity/liquidity mismatches and leverage) may arise and may need appropriate policy responses to mitigate these risks. While further refinements are needed going forward, the 2016 exercise deepened the analysis of this activity-based narrow measure of shadow banking by looking at its components and the potential risks in more detail.

The main findings from the 2016 exercise are as follows:

The main findings from the 2016 exercise are as follows:

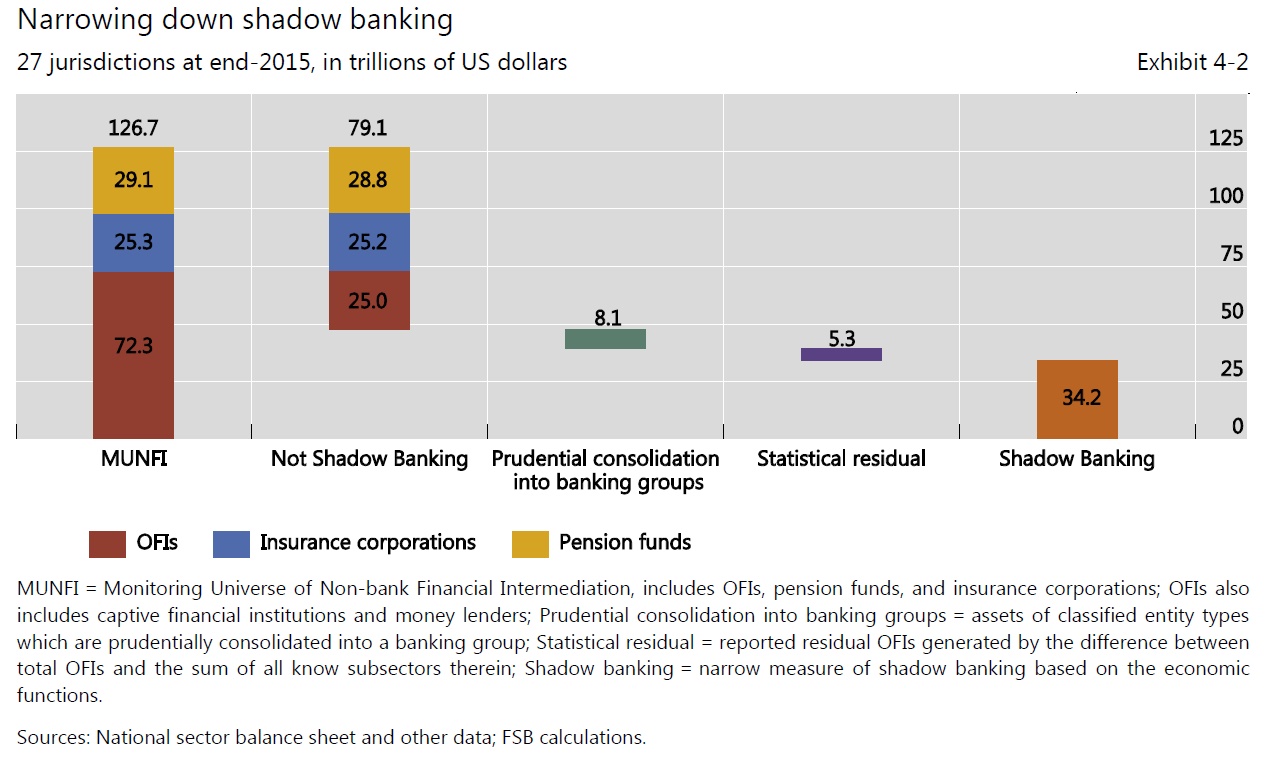

- The activity-based, narrow measure of shadow banking was $34 trillion in 2015, increasing by 3.2% compared to the prior year, and equivalent to 13% of total financial system assets and 70% of GDP of these jurisdictions.

- Credit intermediation associated with collective investment vehicles (CIVs) comprised 65% of the narrow measure of shadow banking and has grown by around 10% on average over the past four years. The considerable growth of CIVs in recent years has been accompanied by liquidity and maturity transformation, and in the case of jurisdictions that reported hedge funds, relatively high level of leverage.

- Non-bank financial entities engaging in loan provision that are dependent on short-term funding or secured funding of client assets, such as finance companies, represent 8% of the narrow measure, and grew by 2.5% in 2015. In at least some jurisdictions, finance companies tended to have relatively high leverage and maturity transformation, which makes them relatively more susceptible to rollover risk during periods of market stress.

- In 2015, the wider aggregate comprising “Other Financial Intermediaries” (OFIs) in 21 jurisdictions and the euro area grew to $92 trillion, from $89 trillion in 2014. OFIs grew quicker than GDP in most jurisdictions, particularly in emerging market economies.

The 2016 exercise also collected new data to measure interconnectedness among the bank and the non-bank financial sectors and to assess the trends of short-term wholesale funding, including repurchase agreements (repos). While the data availability needs to be improved, the data collected suggested that on an aggregated basis, both banks’ credit exposures to and funding from OFIs have continued to decline in 2015, although they remain above the levels before the 2007-09 financial crisis.

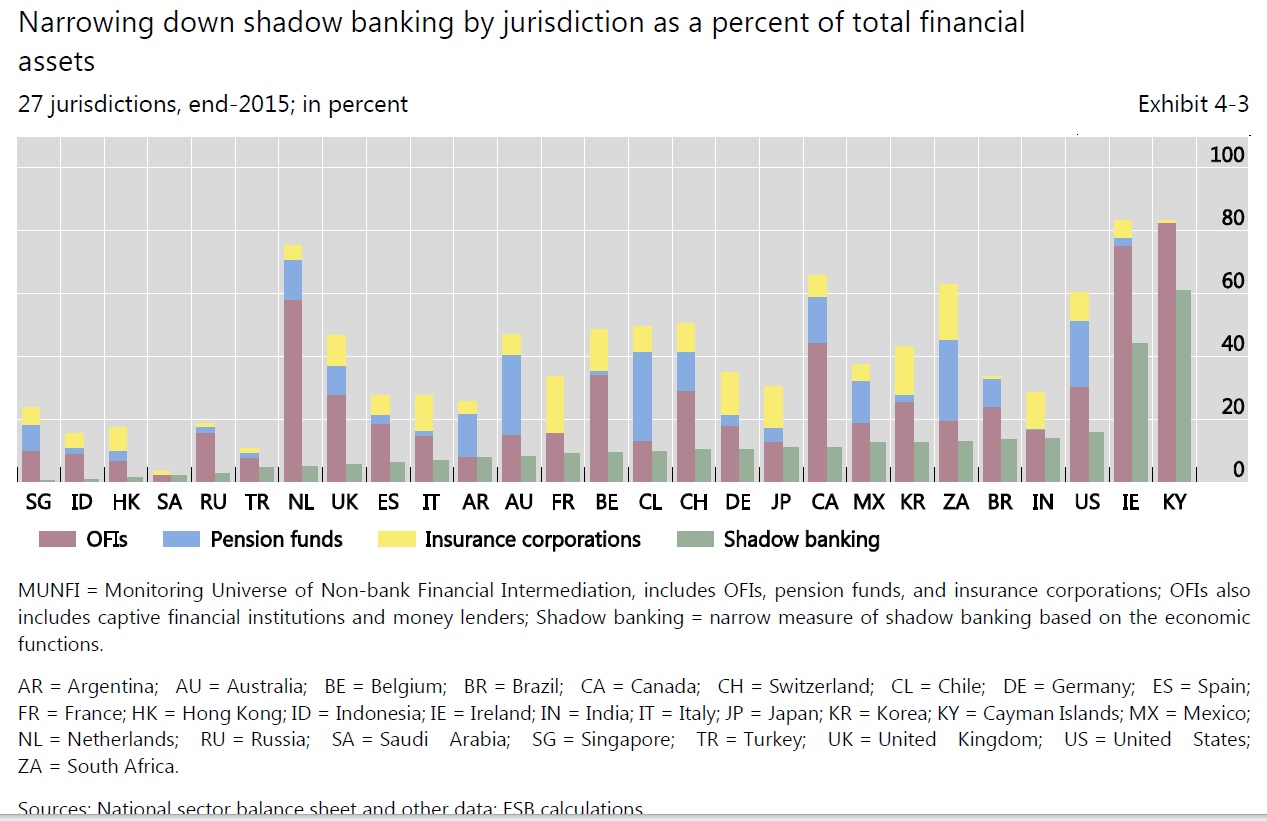

Australia is in the middle of the pack, in terms of percent of total financial assets. The US had the largest shadow banking sector, with $13.8 trillion in 2015, representing 40% of the total shadow banking sector reported by the 27 jurisdictions. The Cayman Islands reported the second largest shadow banking sector, amounting to $4.3 trillion, followed by Japan ($3.2 trillion), and Ireland ($2.2 trillion).

Compared to 2011, the US share of the total shadow banking sector for 27 jurisdictions declined from 48% to 40% according to the narrow measure, whereas the Cayman Islands’ share increased from 8% to 13%. Combined together, the US, the UK, and participating euro area jurisdictions represented 65% of total global shadow banking at end-2015, compared to 73% in 2011.109 Combined, participating euro area jurisdictions represented 20% of the global narrow measure, amounting to $6.8 trillion in 2015.

Loans extended by the OFI sector have been growing in 14 jurisdictions and the euro area since 2011. In some jurisdictions the growth in OFI loans since 2011 has been substantial, increasing at an annual rate of 10% or more in Australia, China, Germany, Indonesia, Korea, and South Africa, with China reporting the highest increase of 35%.

Loans extended by the OFI sector have been growing in 14 jurisdictions and the euro area since 2011. In some jurisdictions the growth in OFI loans since 2011 has been substantial, increasing at an annual rate of 10% or more in Australia, China, Germany, Indonesia, Korea, and South Africa, with China reporting the highest increase of 35%.

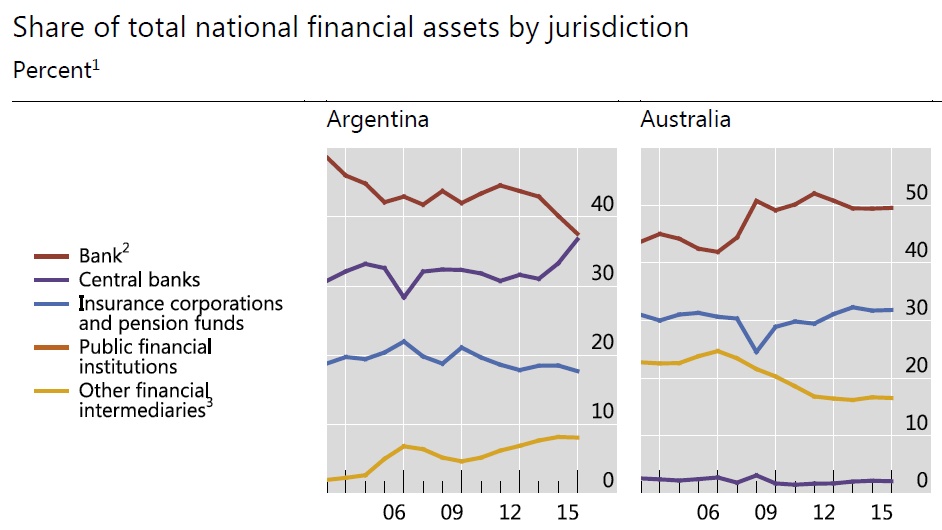

In Australia, banks have half of total national financial assets.

Mark Carney, Chair of the FSB, said “Market-based finance provides important diversification of the funding sources which support the real economy. The enhanced and coordinated system-wide monitoring by authorities continues to improve our understanding of non-bank financial activities and risks to the financial system. This helps to inform our judgement on appropriate policy responses as we transform shadow banking into resilient market-based finance”.

Klaas Knot, Chair of the FSB Standing Committee on Assessment of Vulnerabilities and President of De Nederlandsche Bank, said “The 2016 monitoring exercise has made progress by broadening its scope and deepening the analysis of associated financial stability risks. As shadow banking by its nature continuously evolves and adapts to a new environment, it is important for authorities to continue to improve data availability and risk analysis so as to be able to identify new sources of systemic vulnerabilities in a timely manner”.

The FSB Chair’s letter to the G20 Finance Ministers and Central Bank Governors ahead of their Baden-Baden meeting noted that in completing the work under the Shadow Banking Roadmap, the FSB has not identified new shadow banking risks that currently require additional regulatory action at global level. However, given that new forms of shadow banking activities are certain to develop in the future, FSB member authorities must maintain and continue to invest in an effective and ongoing programme of surveillance, data sharing and analysis so as to support judgements on any required regulatory response in the future.