Having released our November Mortgage Stress analysis, we now look across the states in more detail. Today we look at NSW and Greater Sydney.

NSW has 251,576 households in stress, up 9,000 from last month, and we estimated there are around 13,900 households at risk of default over the next 12 month in the state.

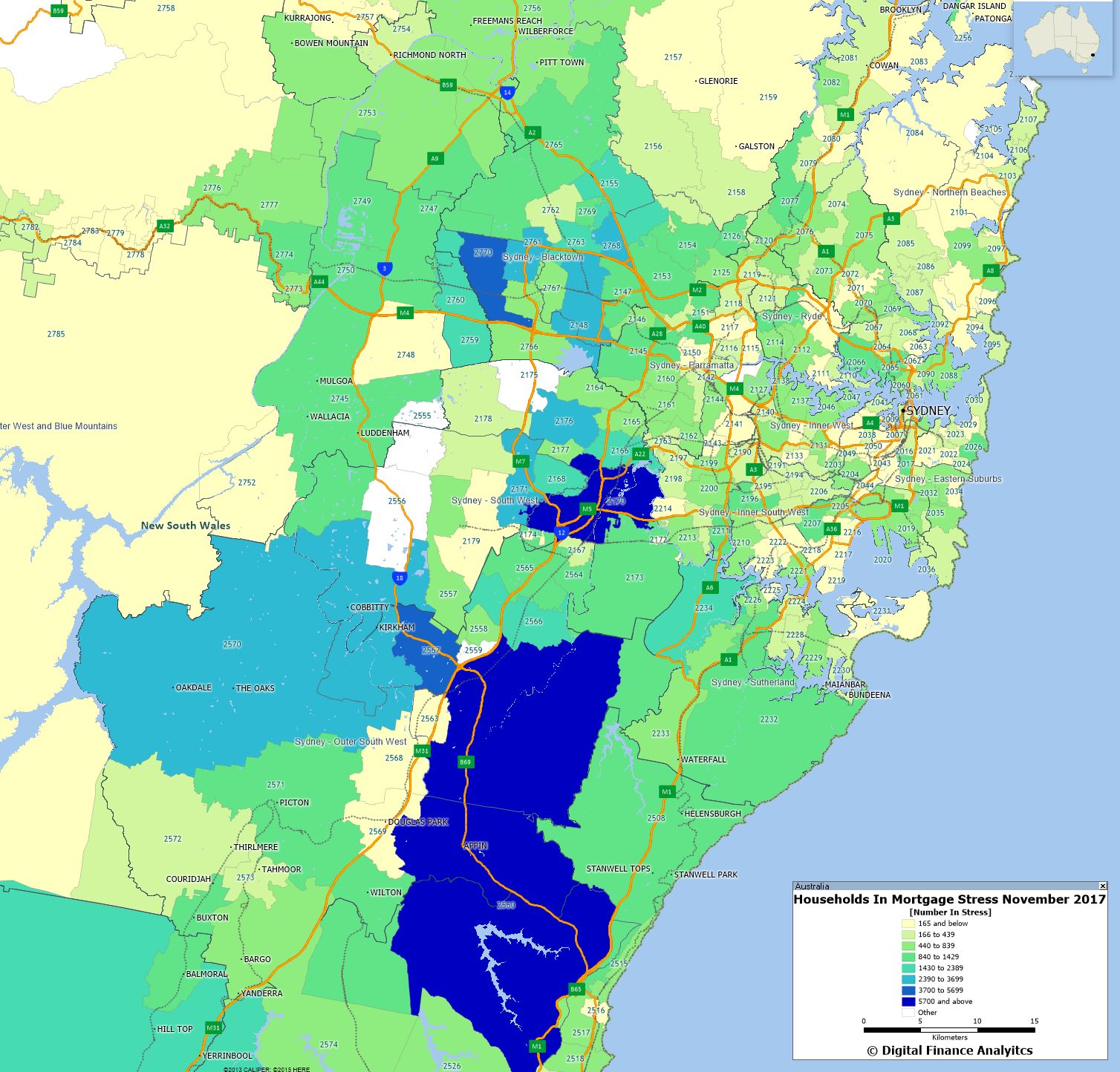

Here is the stress mapping around Great Sydney of the count of households in difficulty. We see a swathe of issues across Western Sydney.

The post code with the highest count of stressed household is 2170, the area around Liverpool, Warwick Farm and Chipping Norton, which is around 27 kilometers west of Sydney. There are 6,807 households in mortgage stress here. The average home price is $803,000 compared with $385,000 in 2010. There are around 27,000 families in the area, with an average age of 34. The average income is $5,950. 36% have a mortgage and the average repayment is about $2,000 each month.

Next is the area around Campbelltown, 2560, which is around 43 kilometers inland from Sydney. Here 5,786 households are in mortgage stress. The average home price is $625,000, up from $320,000 in 2010. Around 20,000 households live in the area with an average age of 34 years. The average income is $6,100 a month. 37% have a mortgage and the average repayment is higher than the national average at $1,800.

We continue to see mortgage stress still strongly associated with fast growing suburbs, where households have bought property relatively recently, often on the urban fringe. The ranges of incomes and property prices vary, but note that it is not necessarily those on the lowest incomes who are most stretched. Banks have been more willing to lend to these perceived lower risk households but the leverage effect of larger mortgages has a significant impact and the risks are underestimated.

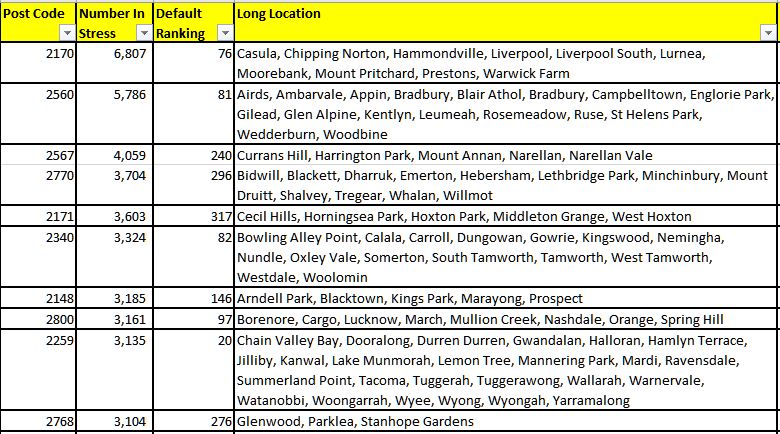

Next, here is the overall listing of the top 10 most stressed post codes across New South Wales as at the end of November 2017. We also show the relative default risk ranking across the country. We will explore risk of default further in a later post, not least because we get different distributions depending on whether we look at the number of defaults, or the absolute value at risk.

Meanwhile, in our next stress-related post, we will look at Victoria.

Meanwhile, in our next stress-related post, we will look at Victoria.