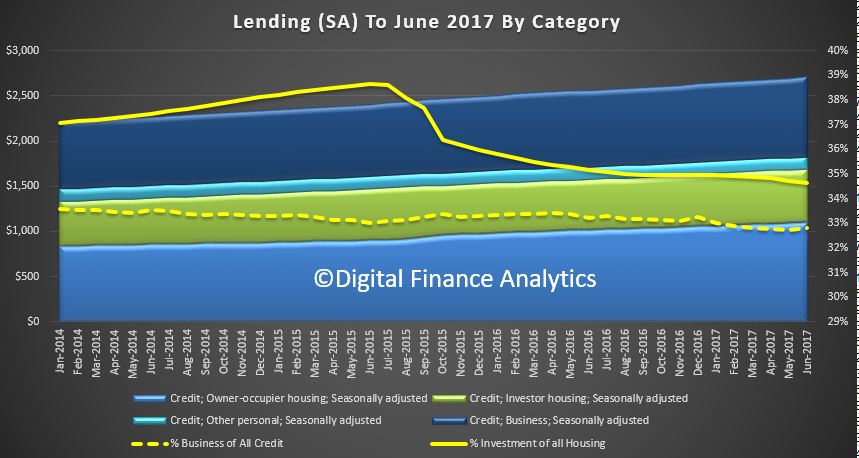

The latest credit aggregates from the RBA to June 2017 shows continued home lending growth, up 0.5% in the month, or 6.6% annually. Business lending rose 0.9%, or 4.4% annually, and personal credit fell 0.1% or down 4.4% over the past year. However, they changed the seasonally adjusted assumptions, so it is hard to read the true picture, especially when we still have significant reclassification going on. In original terms housing loans grew to $1.69 trillion, another record.

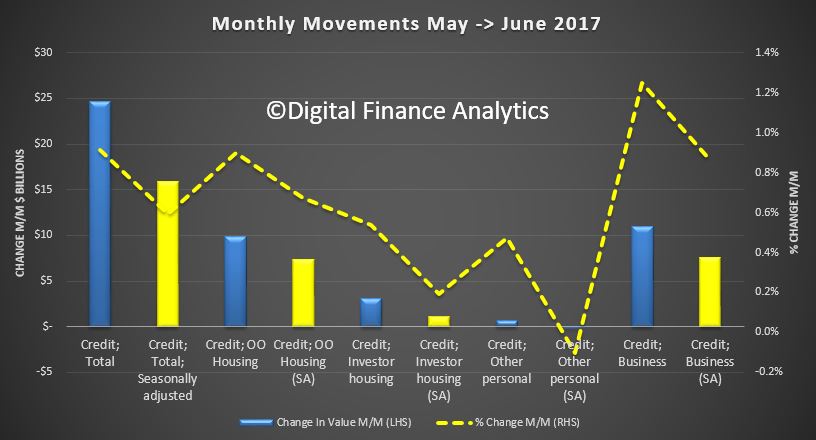

Investor home lending grew 0.5% or $3.13 billion, but this was adjusted down in the seasonal adjusted series to 0.2% or $1.13 billion. Owner occupied lending rose 0.9% or $9.83 billion in original terms, or 0.7% or $7.34 billion in adjusted terms. Business lending rose 1.2% of $11 billion in original terms or 0.9% of $7.61 billion in original terms. The chart below compares the relative movements.

Investor home lending grew 0.5% or $3.13 billion, but this was adjusted down in the seasonal adjusted series to 0.2% or $1.13 billion. Owner occupied lending rose 0.9% or $9.83 billion in original terms, or 0.7% or $7.34 billion in adjusted terms. Business lending rose 1.2% of $11 billion in original terms or 0.9% of $7.61 billion in original terms. The chart below compares the relative movements.

The RBA says:

The RBA says:

Historical levels and growth rates for the financial aggregates have been revised owing to the resubmission of data by some financial intermediaries, the re-estimation of seasonal factors and the incorporation of securitisation data.

… so here is another source of discontinuity in the numbers presented! The movements between original and seasonal adjusted series are significant larger now, and this is a concern. We think the RBA should justify its change of method. Once again, evidence of rubbery numbers!

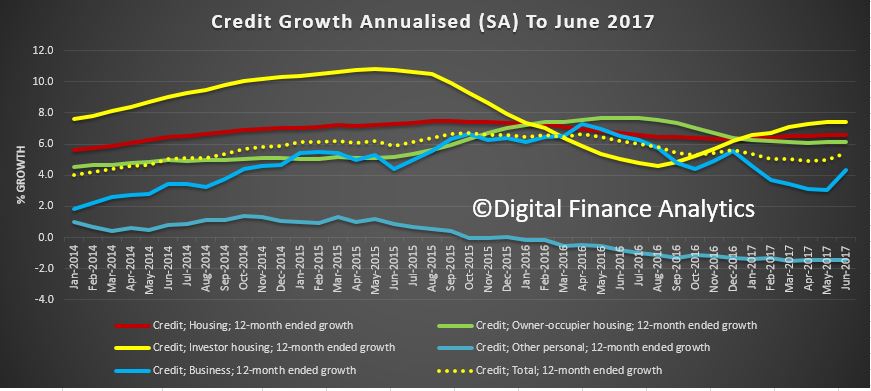

The annualised growth rates highlight that investor lending is still strong relative to owner occupied loans, business lending recovered whilst personal finance continued its decline.

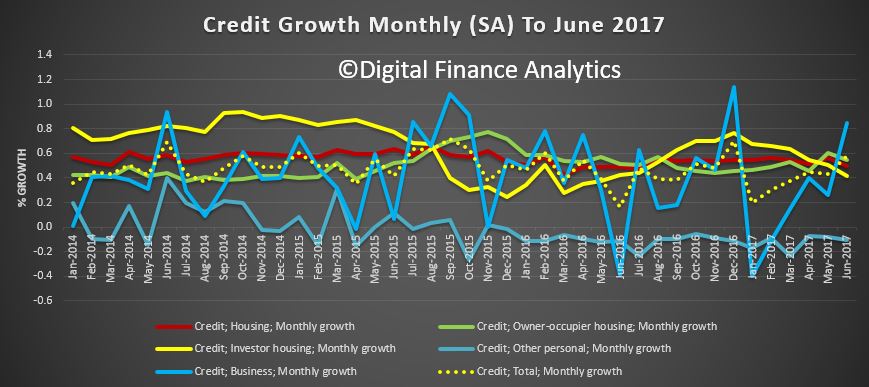

The more volatile monthly series show investor loans a little lower, while owner occupied loans rise further, and there is a large inflection in business lending.

The more volatile monthly series show investor loans a little lower, while owner occupied loans rise further, and there is a large inflection in business lending.

We need to note that now $55 billion of loans have been reclassified between owner occupied and lending over the past year – with $1.3 billion switched in June. This is a worrying continued trend and raises more questions about the quality of the data presented by the RBA.

We need to note that now $55 billion of loans have been reclassified between owner occupied and lending over the past year – with $1.3 billion switched in June. This is a worrying continued trend and raises more questions about the quality of the data presented by the RBA.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $55 billion over the period of July 2015 to June 2017, of which $1.3 billion occurred in June 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

Finally they tell us:

All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series as recorded in the notes to the tables listed below. Data for the levels of financial aggregates are not adjusted for series breaks. The RBA credit aggregates measure credit provided by financial institutions operating domestically. They do not capture cross-border or non-intermediated lending.

So, given the noise in the data, it is possible to argue that either home lending is slowing, or it is not – all very convenient. The APRA data we discussed earlier is clearly showing momentum. Growth is still too strong.

It also makes it hard to read the true non-bank growth rates, but we think they are increasing their relative share as some banks dial back their new business. Taking the non seasonally adjusted data from both APRA and RBA we think the non-bank sector has grown by about $5 billion in the past year to $115 billion. APRA will need to have a look at this, under their new additional responsibility, as we suspect some of the more risky lending is migrating to this less well regulated sector of the market.