AFG provides fresh evidence of the fragile state of Australia’s home loan market emerged today, with new figures revealing national lending activity has slumped to the lowest levels in five years.

Whilst its myopic in one sense as it tracks business via AFG, it does provide further evidence of the slowing pace.

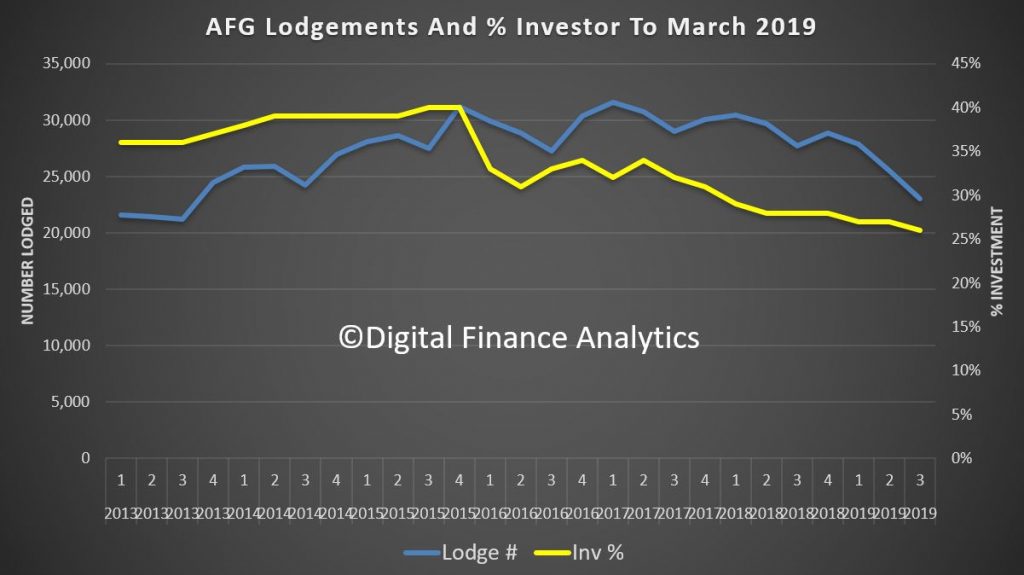

The AFG Mortgage Index and Competition Index released today showed lending volumes across Australia in the first three months of 2019 dropped 10 per cent on the previous quarter. Volumes in the March quarter were 15 per cent lower than the same period last year.

The 23,049 loans lodged during the quarter represented the lowest number in six years, while the $11.6 billion volume was the lowest quarterly figure since 2014.

AFG Chief Executive Officer David Bailey said “Today’s numbers provide stark evidence that the lending environment has significantly deteriorated. It’s a wake-up call for policymakers. The softening of the residential market across the country is a real concern, with Sydney and Melbourne driving the downturn and some states enduring a prolonged period of falling activity.

“Despite moves by regulators to encourage activity, investment lending remains at an all-time low of 26 per cent amid the well- documented concerns around property values, particularly on the eastern seaboard.

“Today’s data confirms we have reached a critical time in the housing market cycle and we would urge policy makers to tread carefully in any regulatory responses flowing from the Royal Commission. This is a time for considered policy formulation that considers the full potential impact on the lending market. It is clear, the broader implications for the Australian economy are huge if we get it wrong.

“The volume of loans written in WA for the quarter of just over $1.3 billion represents the lowest volume seen in WA since the inception of the AFG Mortgage Index. Whilst there has been some talk of WA moving into a brighter resources-led period of sunshine, it is clear the local economy needs broader stimulus.”

The tight lending market and falling house prices have contributed to a decline in NSW volumes of almost 20 per cent on the same quarter in 2018. Victoria is down 16 per cent over the same period.

All other states are also much lower than the same time last year. The only lift in volume over the quarter was seen in the Northern Territory, with an increase in the average loan size and a decrease in Loan to Value Ratios.

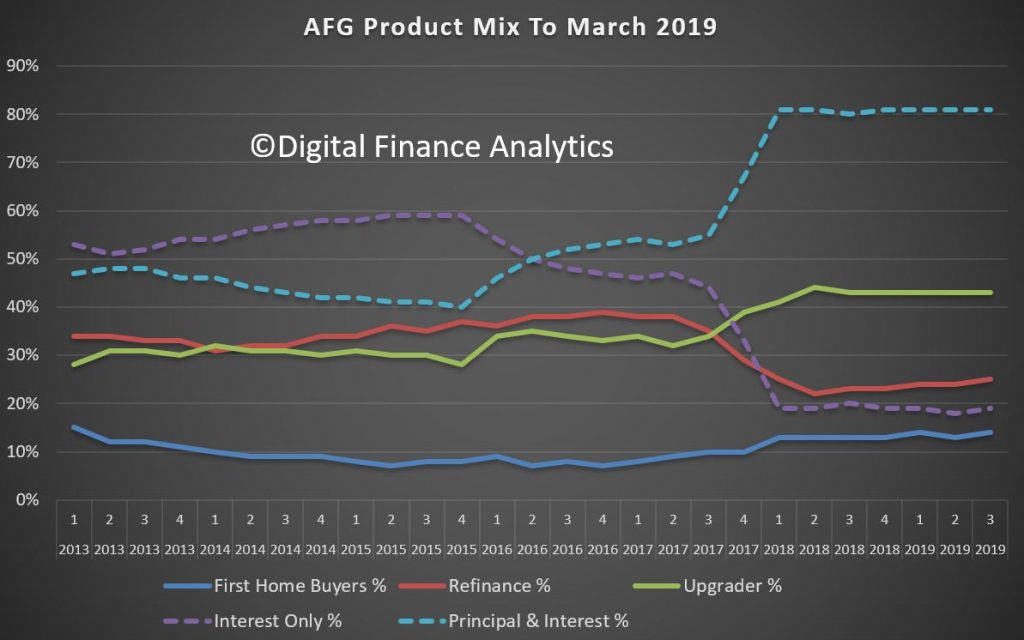

Following the relaxation of APRA-imposed caps on Interest Only (IO) lending, AFG noted a small lift in IO lending driven by the major lenders.

Four years ago, fuelled largely by strong investor demand, Interest Only loans accounted for around 60 per cent of all loans written. Now, with investor loans accounting for a quarter of new business, Interest Only loans account for just 19 per cent of lodgements.

The breakdown of mortgages between major lenders – the ‘big four’ banks and their affiliated brands – and non-majors highlights the crucial role mortgage brokers play in delivering competition to the home loan sector.

The AFG Index showed the market share of non-majors has now been locked in above 40 per cent for more than a year despite a marginal increase for the majors to 58.6 per cent of total lodgements.

Mr Bailey said “The value mortgage brokers deliver by facilitating a competitive lending environment is most starkly shown by the ongoing decline in the market share of the major banks, which peaked in Q3 of 2013 at 78.2 per cent. Outside of the mortgage broking channel, the majors have control and dominate the market. The distribution capability provided by mortgage brokers enables the country’s non-major lenders to compete.

“With the sole exception of First Home Buyers, who remain the last bastion of major bank lending, the growth in non-major lending has been broadly uniform across all other customer types.”

Major lenders are ahead on fixed-rate loans, with a steady increase across the quarter, leaving four out of five homebuyers that chose the certainty of fixing their interest rates doing so with a major lender.

Examination of the overall volumes going to the major bank reveals the big losers over the past six months have been ANZ and NAB. NAB’s share has halved over the past six months to now be as low as five per cent.

The Westpac stable of brands emerged as big winners, as has Bankwest – whose renewed focus on broker and customer service has paid strong dividends in Western Australia. Bankwest accounts for more than one in every five WA originations. Together with CBA, Bankwest has a stranglehold on more than 35 per cent of all loans written in the State.