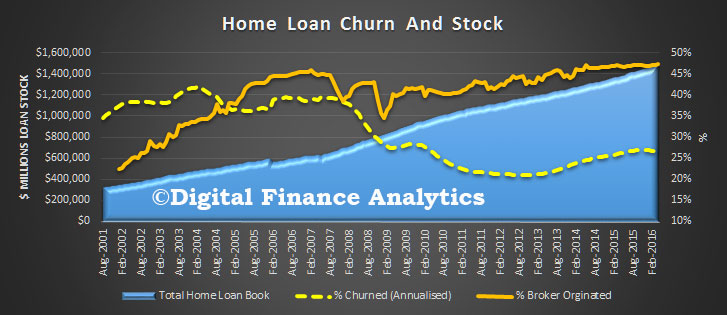

Currently more than 26 percent of the home loan lending book is being churned each year, reflecting strong refinance demand, low rates and massive marketing campaigns. So it is interesting to look at the trend data, especially in the light of the New Zealand Reserve Bank data we discussed yesterday, which indicated 35 per cent of loans there are churning annually.

Data from the ABS enables us to analyse the proportion of the home loan book which, by value is churned each year. To do this we compare the loan stock data, with the loan flow data, by total value pools. Here are the result for the ADI’s.

The stock figure takes account of new loans written, refinanced and repaid. The flow data shows us the new loans written. So we see a rise in churn from 2012, moving from about 20 per cent to more than 26 per cent. We also see a slowing turn in recent months, suggesting perhaps that the refinance drive has peaked. That said, there are a number of marketing campaigns suggesting that borrowers should refinance now if their mortgage rate does not have a three in front of it! On average, households with a loan of more than a year old would do well to check their rate.

The stock figure takes account of new loans written, refinanced and repaid. The flow data shows us the new loans written. So we see a rise in churn from 2012, moving from about 20 per cent to more than 26 per cent. We also see a slowing turn in recent months, suggesting perhaps that the refinance drive has peaked. That said, there are a number of marketing campaigns suggesting that borrowers should refinance now if their mortgage rate does not have a three in front of it! On average, households with a loan of more than a year old would do well to check their rate.

All things being equal, you could say that the average loan is under four years, though in the real world, there is diversity, with some loans turned over every one to two years, and others retained for a much longer term.

What is also striking though is that in the 2000’s churn moved up from around 13 per cent to reach a peak of 39 per cent prior to the 2007/8 GFC. This rise in churn can be mapped to the rise of mortgage brokers in Australia (whilst the correlation could be coincidence, we suspect there is a link) as many brokers were on commission structures without claw-backs, with upfront commissions more generous that tail commissions. Changes in regulation and commission structures made the churn harder to execute later.

Still a quarter of the book turning over annually is pretty amazing, considering all the activity (and fees etc.) which are generated. It also suggests to me that bank’s should be thinking much harder about retention strategies.