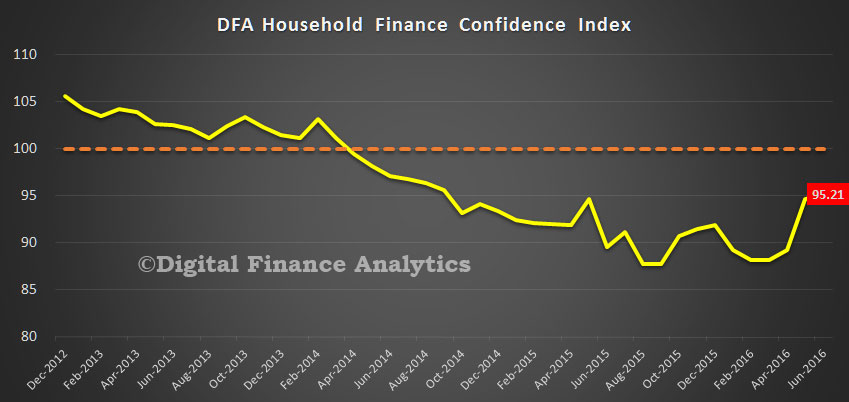

The latest edition of the Digital Finance Analytics Household Finance Confidence Index to end June is released today. Overall confidence improved again, to 95.21, although this is still below the long-term neutral score of 100 which we fell below in 2014.

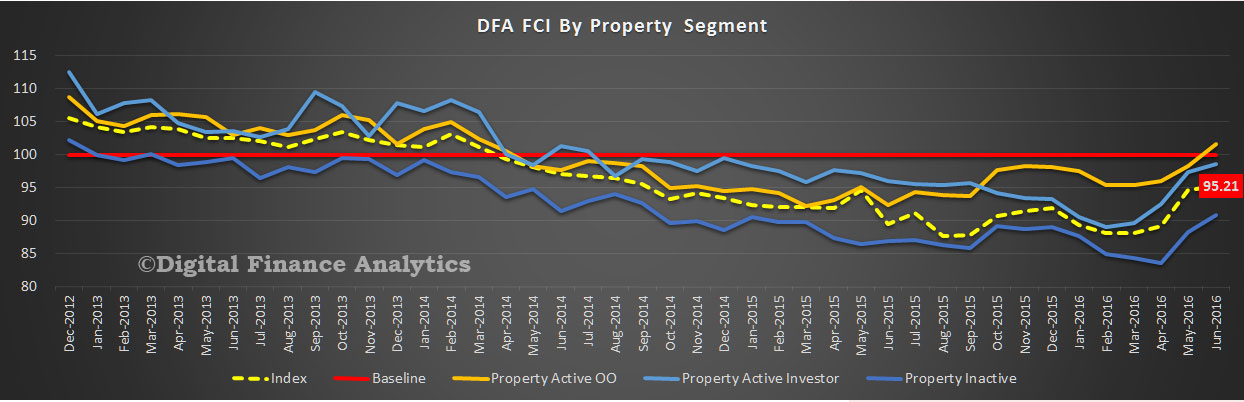

Despite Brexit, the indecisive election result, and stock market volatility, the average financial confidence all household split by property segments improved, with property active owner occupied households now above neutral, thanks to ever lower mortgage interest rates, and positive news on home prices in the major states of NSW and VIC. Property inactive households were a little more positive too, thanks to rental increases being contained and food costs down a little. Property investors are also positive, thanks to lower interest rates, and better access to mortgage funds at good prices. Intention to purchase property has improved, thanks to continued capital gains, lower mortgage funding costs and net perceived better returns than stocks or deposits. Future price growth expectations also rose.

Despite Brexit, the indecisive election result, and stock market volatility, the average financial confidence all household split by property segments improved, with property active owner occupied households now above neutral, thanks to ever lower mortgage interest rates, and positive news on home prices in the major states of NSW and VIC. Property inactive households were a little more positive too, thanks to rental increases being contained and food costs down a little. Property investors are also positive, thanks to lower interest rates, and better access to mortgage funds at good prices. Intention to purchase property has improved, thanks to continued capital gains, lower mortgage funding costs and net perceived better returns than stocks or deposits. Future price growth expectations also rose.

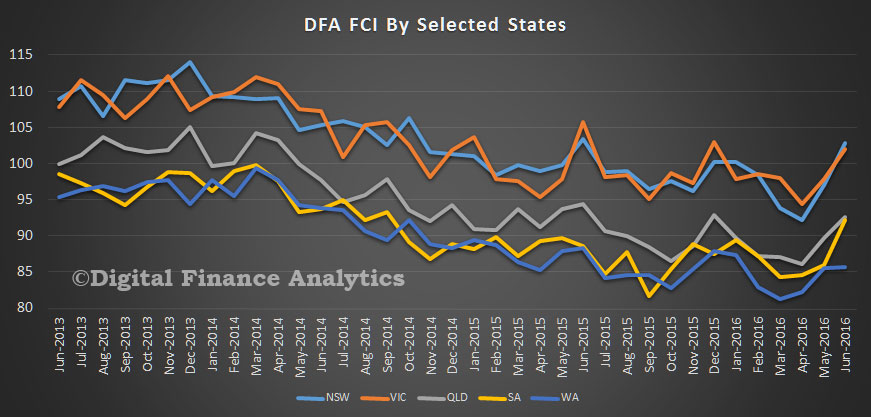

The state variations are quite stark however, with NSW and VIC improving strongly, whilst WA languishes, thanks to flatter home prices, and rising unemployment. Variations across the regions were even more extreme.

The state variations are quite stark however, with NSW and VIC improving strongly, whilst WA languishes, thanks to flatter home prices, and rising unemployment. Variations across the regions were even more extreme.

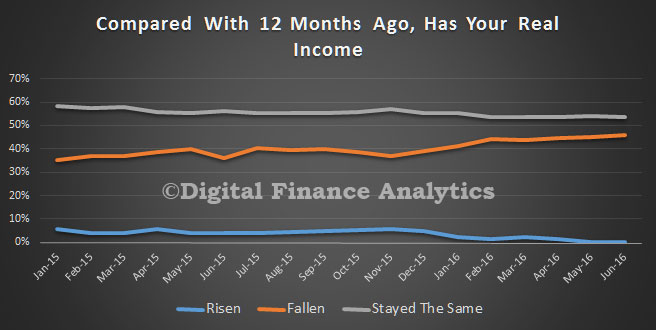

Income, in real terms, continues to fall for many. Those reliant on interest from bank deposits were hardest hit, with average rates for many falling. Further drops in returns on deposits will force many to consider alternatives, including property.

Income, in real terms, continues to fall for many. Those reliant on interest from bank deposits were hardest hit, with average rates for many falling. Further drops in returns on deposits will force many to consider alternatives, including property.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

By way of background, these results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health. To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.