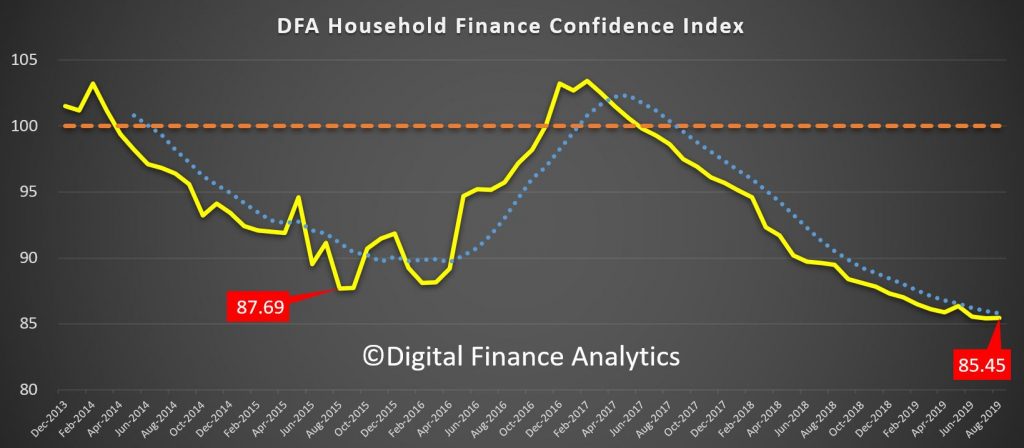

Digital Finance Analytics has released the latest in our series of the Household Financial Confidence Index to end of August 2019. The reading this month was just a little higher at 85.45 (85.43 last month), but still well below the 87.69 back in 2015, which was the previous low, and significantly below the neutral setting. No wonder households are not spending!

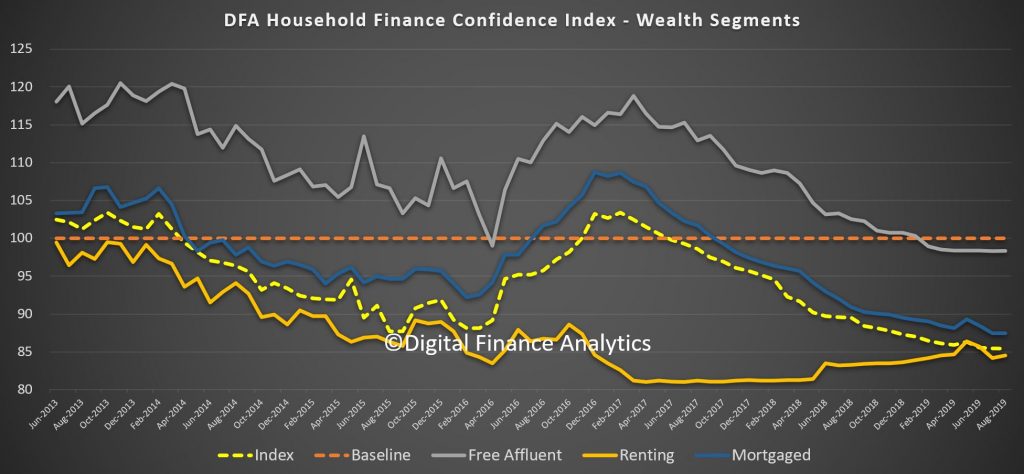

Across our wealth segments, those owing property mortgage free remain the most confident, while those with mortgages are less confident, along with renters.

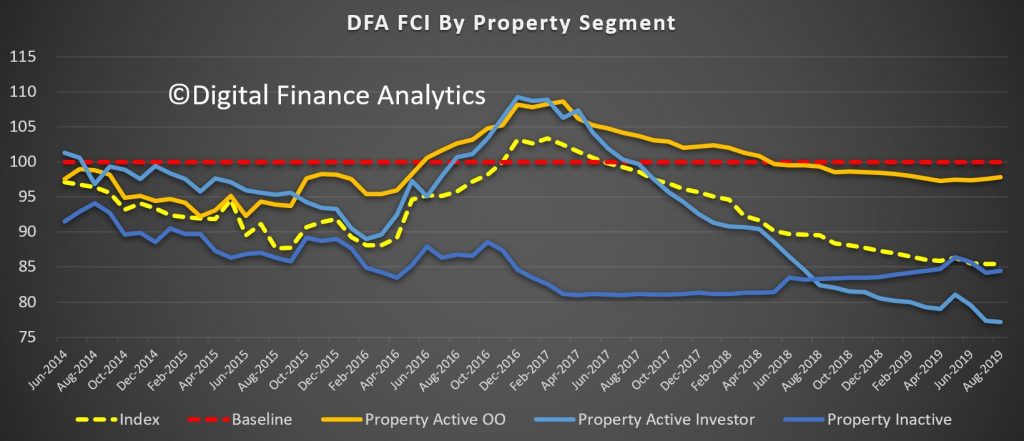

Within the property segments, owner occupied borrowers are a little more confident this month as the mortgage interest rate cuts work through. Property investors are still well below the property inactive group, as rental streams are easing back, and values of high rise apartments in particular are being questioned, thanks to the recent coverage of faulty construction and flammable cladding. In most centers those seeking to rent have more choice, and lower rental options than a couple of years back.

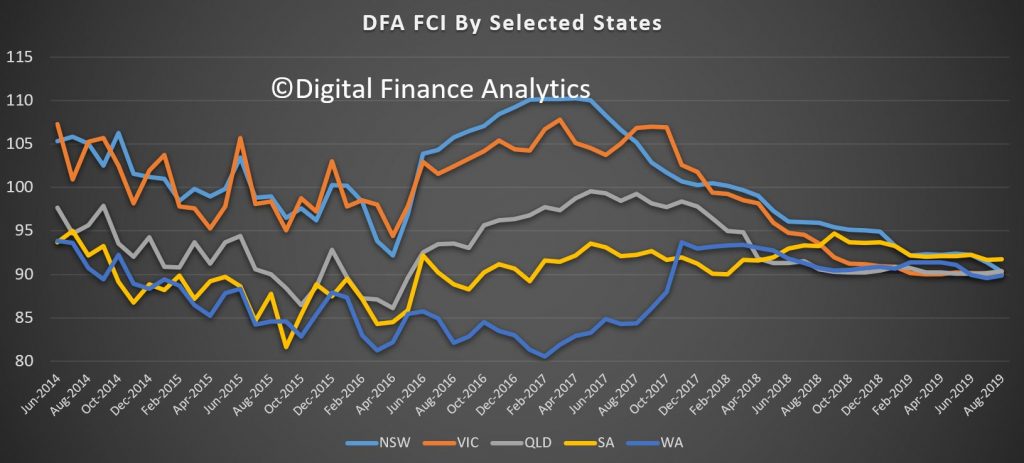

Across the states, the confidence factor are clustering as NSW and VIC continue to weaken, while SA and WA both move a little higher.

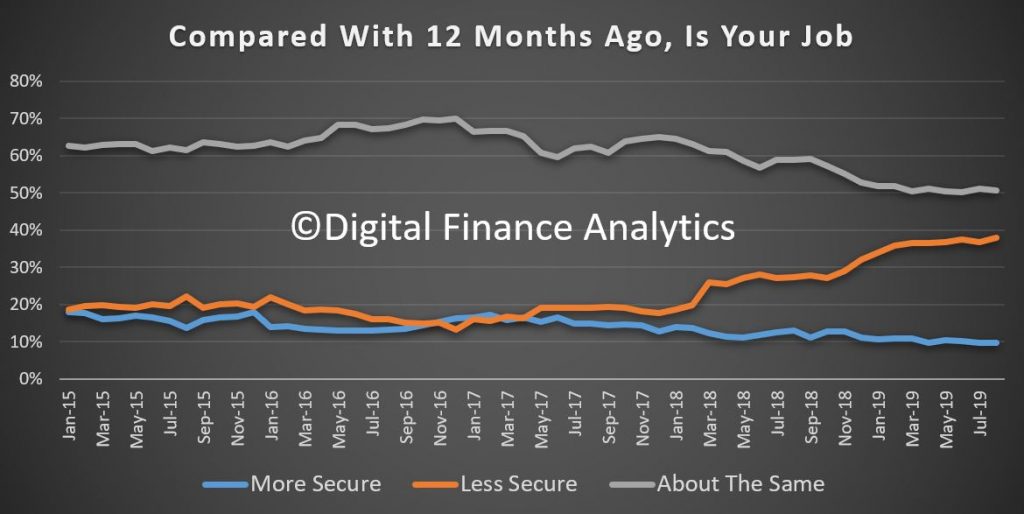

Looking at the moving parts within the index, job insecurity rose further in the month, up 1.38% to 38%. We continue to see higher levels of underemployment and fragmented employment, reflecting the changing work environment, gig economy jobs plus falls in the retail and construction sectors. More jobs are in the lower-paid health care and aged care segments. The drought is also causing issues now for some.

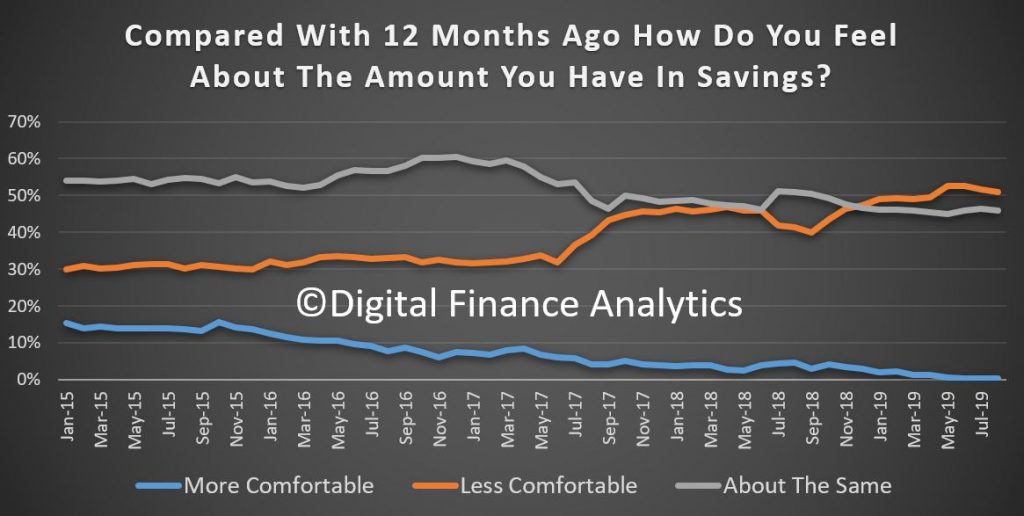

Savings are taking a battering as bank deposit rates continue to tumble, and other households continue to raid savings to maintain lifestyle. There are of course limits to how long this can go on. More than 3 million households rely on income from deposit accounts, and some are considering more risky options, while others have decided to sit tight and just spend less. Again, the myopic focus on mortgage rates misses the issues many savers are facing.

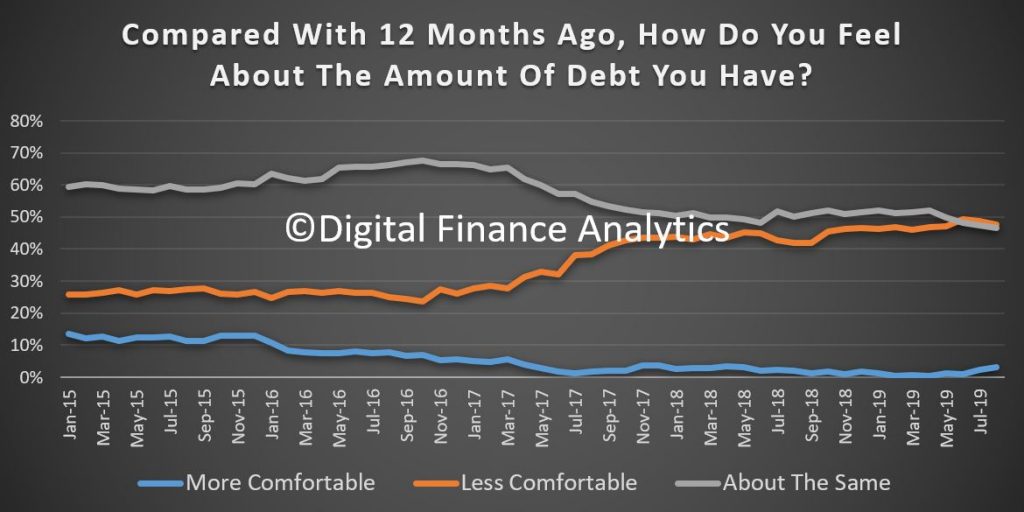

Lower mortgage interest rates have provided some relief to mortgage borrowers now, up 0.68% this month to 3.12%. However many households remain gridlocked with large outstanding debts, which often include credit cards as well as a mortgage. 47% are less comfortable than a year ago. Refinancing is available to some, but those with negative equity, of higher LVR loans are locked into more expensive loans.

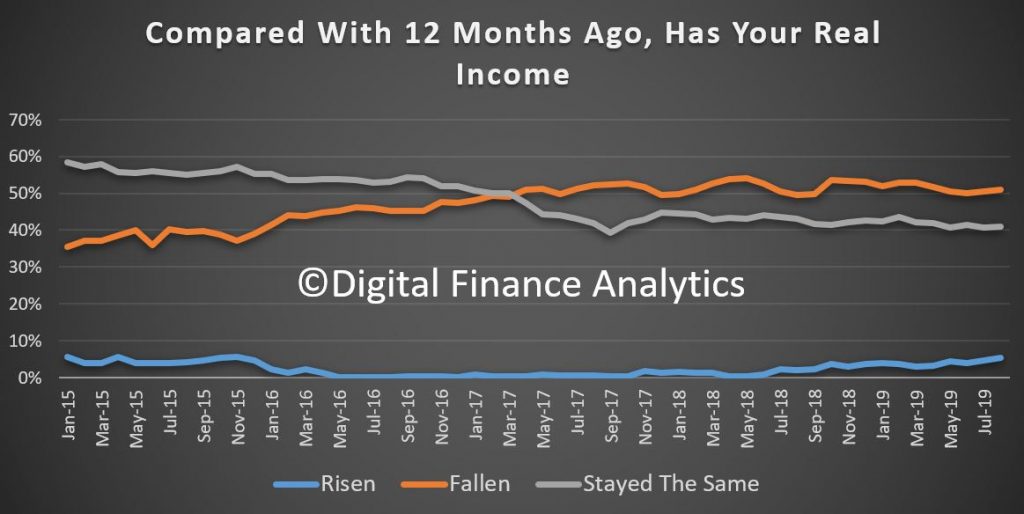

Incomes remain under pressure, with 5.32% of households reporting higher real incomes than a year ago, up 0.57% compared with last month. 51.1% reported real incomes have fallen in the past year and 40.8% no change. The recent changes to weekend rates and healthcare rates in VIC are showing. Public sector employees continue to do better than the private sector.

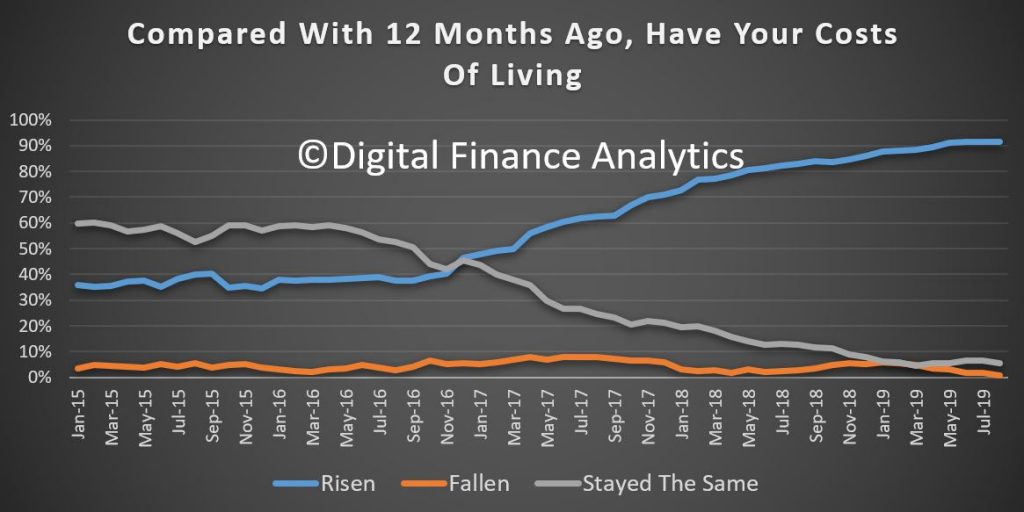

Costs of living remains a black spot, with the official cpi just not reflecting the lived experience of many households. 91.6% said real costs were higher than a year ago. The rising price of vehicle fuel, healthcare and childcare costs, plus energy bills and rates all registered as significant issues. Everyday costs are also higher.

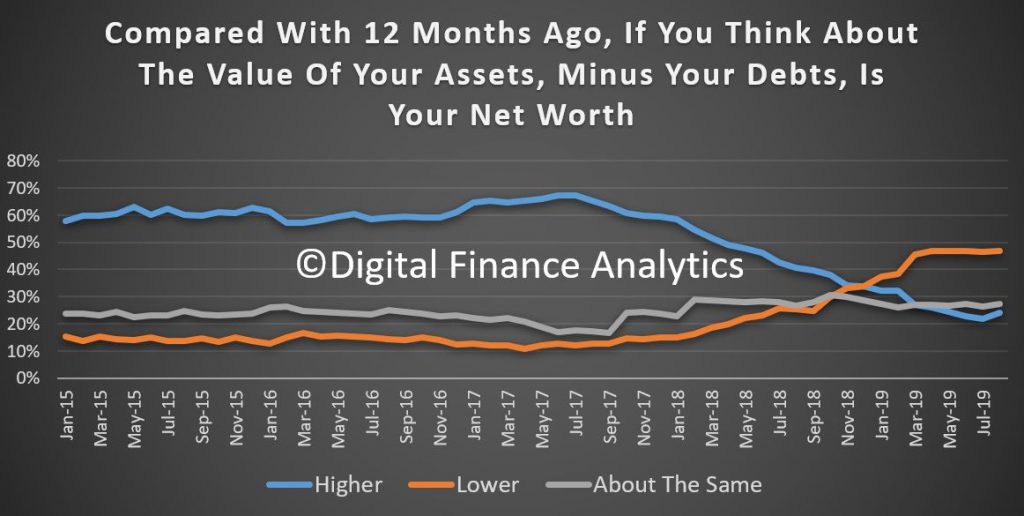

Net worth has risen for 24% of households over the last year, up from 21.84% the prior month. However 46.88% reported a lower net worth than a year ago, thanks to lower property values, changes in share prices and lower levels of savings.

In summary therefore the recent moves in property prices higher in some locations is having a net positive effect on households financial confidence – which illustrates the extent to which property is wired into household balance sheets (at least for those who own property). The critical question is of course whether this will turn into a Bull trap as the international environment worsens, or whether the recent moves to cut rates and reduce lending standards will have a material positive impact on household financial confidence ahead. Plus all the spruiking, of course.

That said cost pressures, incomes pressures, and lower returns for savers are still having a significant impact. The housing sector alone will not turn household financial confidence around. The journey back to a neutral level will be long and hard won.