The latest data from the ABS on Housing Finance to February 2017 shows that overall finance continued to grow.

The trend estimate for the total value of dwelling finance commitments excluding alterations and additions rose 0.4%. Investment housing commitments rose 0.7% and owner occupied housing commitments rose 0.2%. [DFA NOTE: They include owner occupied refinance in these numbers]

In seasonally adjusted terms, the total value of dwelling finance commitments excluding alterations and additions fell 2.7%.

But within the moving parts there are interesting observations – as usual we will focus on the trend series, which irons out some of the statistical bumps, though others will rush to comment on the 13% fall in investor loan flows from the previous month.

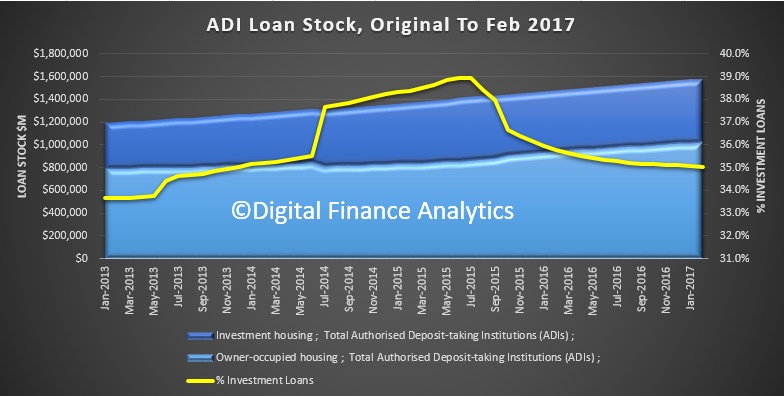

But looking first at ADI loan stock, overall balances rose 0.44% in the month to $1.57 trillion. Investor loans comprise 35% of the total, just down a little, in original terms.

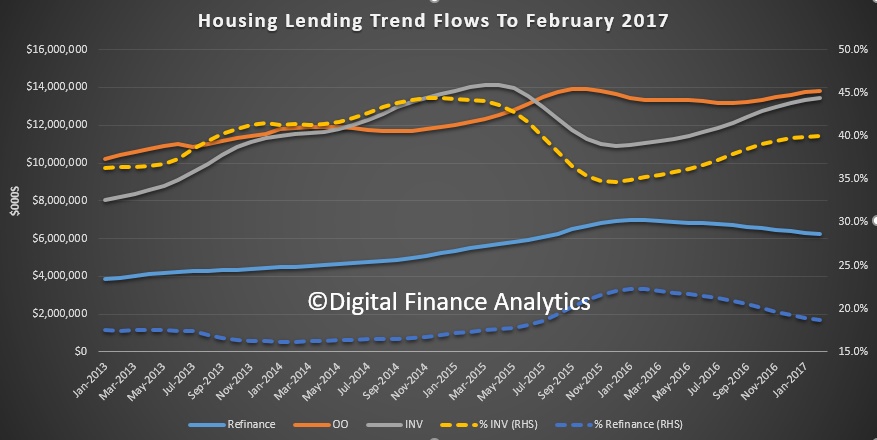

Turning to the trend lending flows, total flows grew by 0.38% compared with the previous month, up $128 million. Within that, refinance fell to 18.7% of flows, down 0.83% or $50 million, owner occupied loans rose 0.65%, up $89 million and investment loans rose 0.69% or $91 million.

Turning to the trend lending flows, total flows grew by 0.38% compared with the previous month, up $128 million. Within that, refinance fell to 18.7% of flows, down 0.83% or $50 million, owner occupied loans rose 0.65%, up $89 million and investment loans rose 0.69% or $91 million.

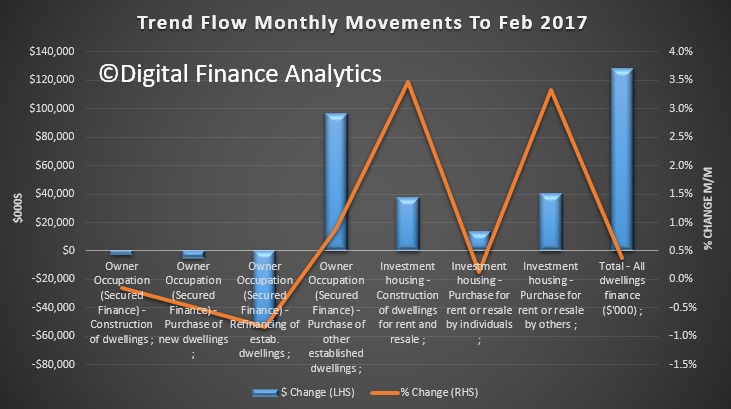

The main rise in the owner occupied sector was the purchase of established dwellings, whilst funding for new purchases and construction both fell a little. All categories of investor lending rose.

The main rise in the owner occupied sector was the purchase of established dwellings, whilst funding for new purchases and construction both fell a little. All categories of investor lending rose.

The HIA highlights that

The HIA highlights that

the number of loans to owner occupiers constructing or purchasing new homes during February 2017 rose in just two states – South Australia (+6.5 per cent) and Queensland (+3.7 per cent). Compared with a year earlier, the largest reduction in lending volumes affected the Northern Territory (-63.8 per cent), followed by the ACT (-23.4 per cent) and New South Wales (-9.7 per cent). There were also falls in Western Australia (-8.7 per cent), Victoria (-2.0 per cent) and Tasmania (-1.7 per cent).

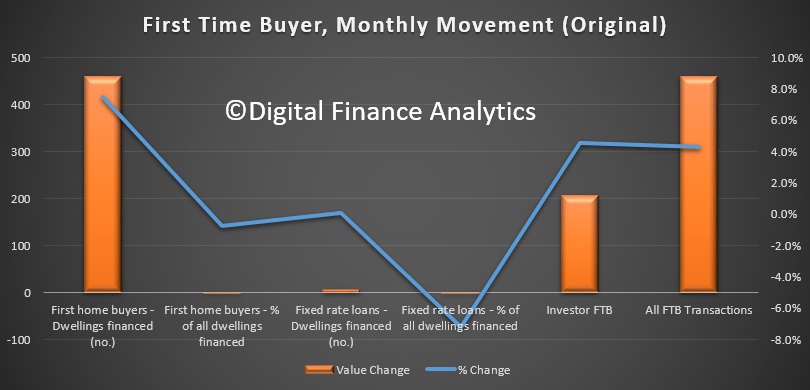

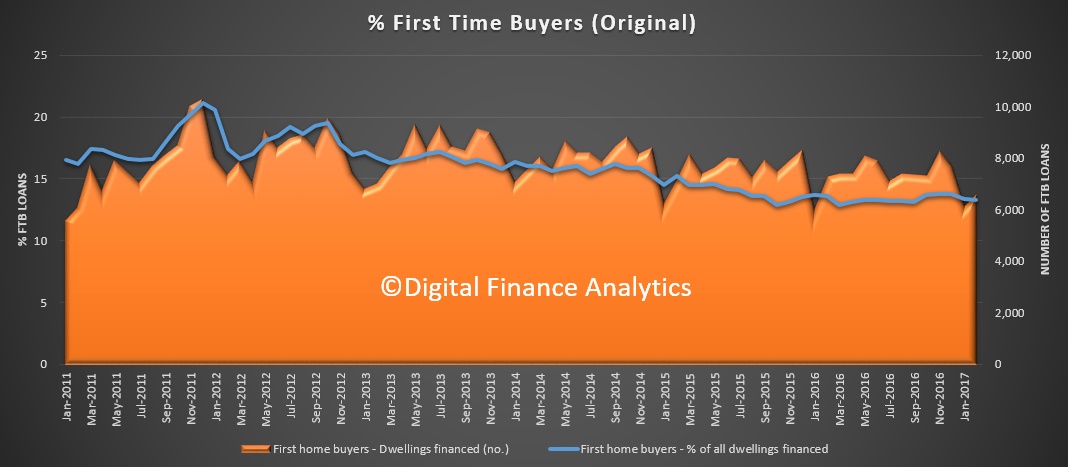

Looking next a first time buyers, the number of transactions rose in the month, in original terms up 7.5% to 6,596, or 13.3% of all transactions, still below previous peaks and lower than last month.

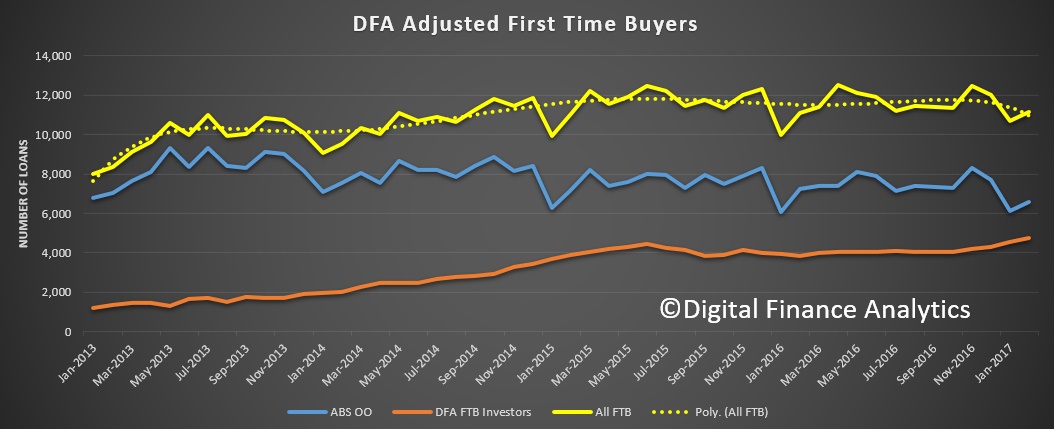

Our surveys also identified another 4,600 first time buyers going direct to the investment sector, so overall volumes are higher than the official figures suggest.

Our surveys also identified another 4,600 first time buyers going direct to the investment sector, so overall volumes are higher than the official figures suggest.

Looking at the movements, month on month, the number of FTB rose, with an increase of 460 over the previous month. Fixed rate lending compared with all transactions was down.

Looking at the movements, month on month, the number of FTB rose, with an increase of 460 over the previous month. Fixed rate lending compared with all transactions was down.