The latest RBA credit aggregates for October 2015, released today are not easy to interpret because of the myriad of adjustments. Housing loans have more reached $1.5 trillion, another record. But are these numbers trust-worthy?

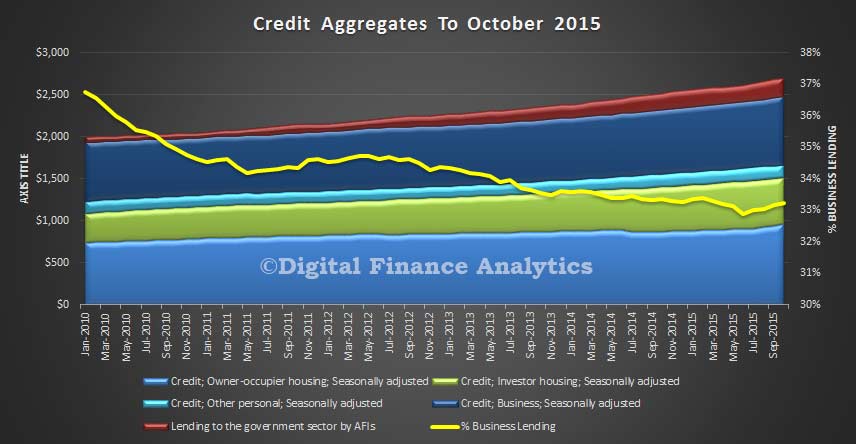

At the aggregate level, total credit rose a seasonally adjusted 0.61% in the month, or 6.11% in the past year. Lending to business grew 0.84% in the month, and 5.88% in the last year. Business lending as a proportion of all lending sits at 33.2%, from an all-time low of 32.9% in July, but clearly business investment continues to be constrained. Housing grew 0.58% in the month, and 7% in the past year, whilst personal credit fell 0.89% in the month and 0.27% in the year, a sign that households remain cautious.

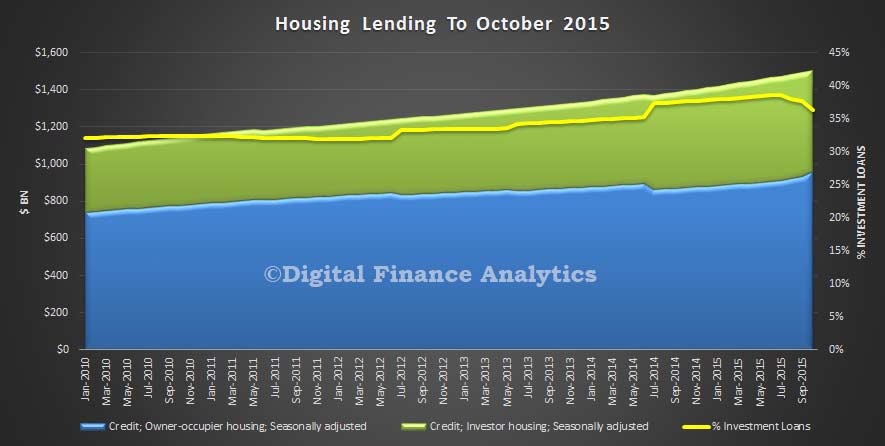

Turning to housing finance in more detail, and this is where it get complex; lending for owner occupied loans rose 2.62% in the month, representing 9.41% growth in the past year, while investment lending fell 2.8% in the month, and grew 3.03% in the year. But there are so many adjustments in these numbers, as the banks reclassify more loans, thanks to a combination of internal review, and customer request. Specifically, the differential movement in investment loans is making people check their loans are correctly classified, and RBA estimates $30bn of loans have been switched. Investor loans on book comprise 36.35% of all housing, down from its recent heights of 38.55% in July. The only thing we can be sure of is the numbers will move again next month. I discussed the recent RBA comments on this issue recently.

Turning to housing finance in more detail, and this is where it get complex; lending for owner occupied loans rose 2.62% in the month, representing 9.41% growth in the past year, while investment lending fell 2.8% in the month, and grew 3.03% in the year. But there are so many adjustments in these numbers, as the banks reclassify more loans, thanks to a combination of internal review, and customer request. Specifically, the differential movement in investment loans is making people check their loans are correctly classified, and RBA estimates $30bn of loans have been switched. Investor loans on book comprise 36.35% of all housing, down from its recent heights of 38.55% in July. The only thing we can be sure of is the numbers will move again next month. I discussed the recent RBA comments on this issue recently.

The RBA makes the following caveats:

The RBA makes the following caveats:

All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series as recorded in the notes to the tables listed below. Data for the levels of financial aggregates are not adjusted for series breaks. Historical levels and growth rates for the financial aggregates have been revised owing to the resubmission of data by some financial intermediaries, the re-estimation of seasonal factors and the incorporation of securitisation data. The RBA credit aggregates measure credit provided by financial institutions operating domestically. They do not capture cross-border or non-intermediated lending.

Following the introduction of an interest rate differential between loans to investors and owner-occupiers a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $30.6 billion over the period of July 2015 to October 2015. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

The APRA ADI data is also out today, and we will look at this later.

One thought on “Housing Lending Up Again In October to $1.5 trillion.”