Moody’s says On 3 October, ING Groep N.V. announced that it will accelerate plans to digitalize its retail business, and, in addition to previously announced cost cutting, will cut another €900 million by 2021 as part of its updated “Think Forward” strategic plan. The updated plan will help the bank preserve profitability, a credit positive.

Although ambitious, we believe the updated plan can be implemented as scheduled, which will help ING preserve its profitability and reach its 50%-52% cost/income target ratio by 2021 (versus 56.2% as of June 2016), a good performance relative to the European Union bank average of 63%. ING is accelerating its transformation plan amid persistent low interest rates that negatively pressure its net interest margin and what it estimates is a 52% increase in regulatory costs in 2016.

The new measures aim to reduce ING’s cost base, focus on direct banking and gain primary relationships with customers. ING expects to meet these targets by merging Record Bank (unrated) within ING Belgium and building a single bank platform for the Dutch and Belgian entities; accelerating the retail bank’s digitalization; closing about 600 of 1,245 branches in Belgium; building a uniform range of products for retail customers in other markets including Spain, Italy, France, Czech Republic and Austria; and optimizing support functions globally. Through these measures, ING plans to reduce staff by 7,000 by 2021 (including 3,500, or 34%, of its workforce in Belgium and 2,300, or 18%, in the Netherlands). ING expects IT expenses of about €800 million between now and 2021, but forecasts the upgrades delivering €900 million of gross annual cost savings during the same period. The restructuring costs will be covered by a €1.1 billion provision, €1 billion of which will be booked in the fourth quarter of this year.

Since announcing its Think Forward plan in 2014, ING has improved its group common equity Tier 1 capital ratio to 13.1% as of June 2016, from 10% in 2013, and the bank has increased its return on equity to 10.8%, which is within its 10%-13% target range. ING also resumed dividends to shareholders in 2015.

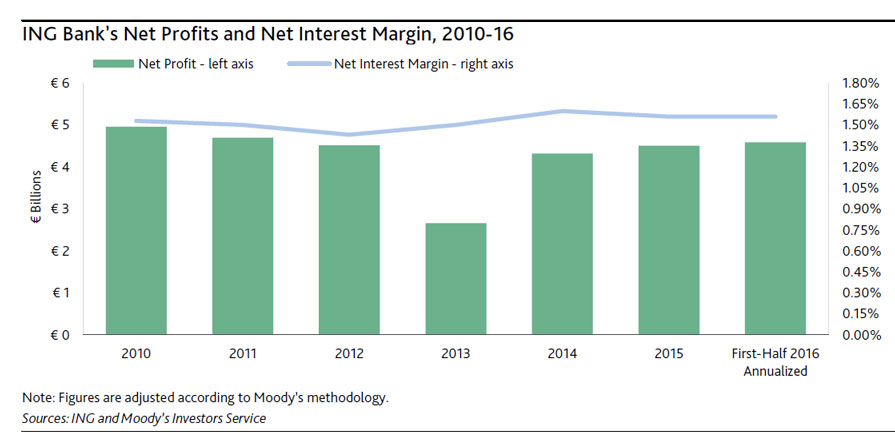

Although ING’s profitability and net interest margin have increased since 2013, they have started reaching a plateau especially in the Netherlands and Belgium, and its cost-to-income ratio (including regulatory costs) increased above its 50%-53% target. Belgian deposit rates have fallen to the legal minimum, leaving the bank with no headroom to further re-price its liabilities there. ING’s new set of measures seek to adapt the bank’s business model to margin pressure arising from a prolonged low rate environment and increased customer expectations in digital banking.