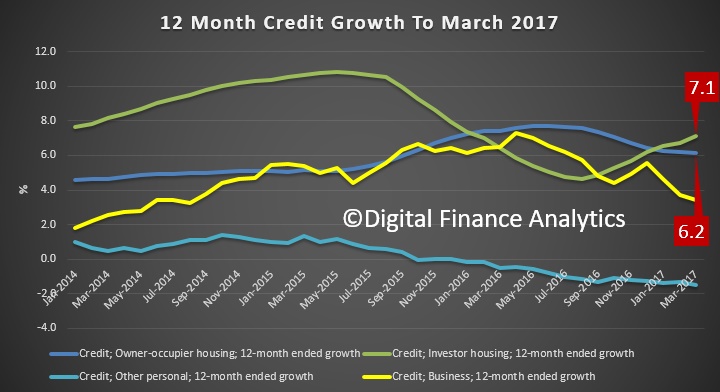

The latest data from the RBA, the credit aggregates, shows that loan growth was strongest for investment home loans, at an annualised rate of 7.1% compared with owner occupied loans at 6.2%. Business lending fell again, and personal credit continues to fall.

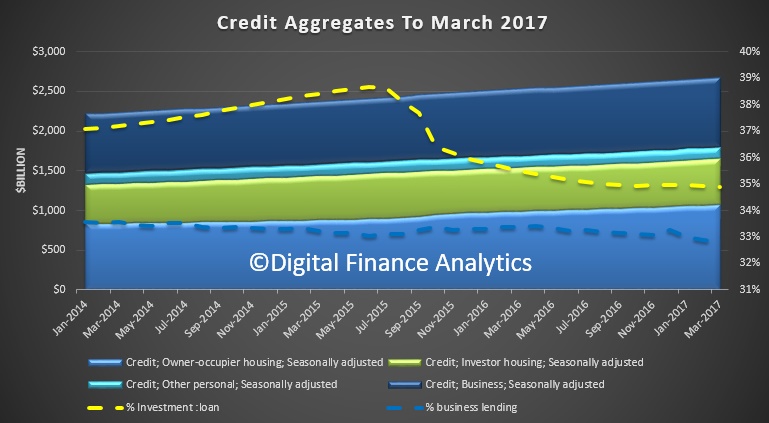

The proportion of lending to business fell to 32.8% (a record low) and the proportion of home lending for investors sat at 34.9%

The proportion of lending to business fell to 32.8% (a record low) and the proportion of home lending for investors sat at 34.9%

Total credit grew $9.7 billion (up 0.4%), owner occupied lending rose $6.7 billion (up 0.6%), investment loans rose $2.5 billion (up 0.4%) and lending to business up $1 billion (up 0.1%).

However, the RBA adjusts these numbers to take account of $1.2 billion restatement between owner occupied and investment loans. Overall housing rose 6.5% in the past 12 months, way above income growth, so higher household debt once again.

Comparing the RBA and APRA data, it looks like the share of non-bank investor home lending is rising, and of course these lenders are not under the APRA regulatory control, but fall under ASIC (and they are not required to hold capital, as they are not ADIs). This is a loophole.

Comparing the RBA and APRA data, it looks like the share of non-bank investor home lending is rising, and of course these lenders are not under the APRA regulatory control, but fall under ASIC (and they are not required to hold capital, as they are not ADIs). This is a loophole.

The RBA notes:

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $51 billion over the period of July 2015 to March 2017, of which $1.2 billion occurred in March 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

2 thoughts on “Investor Loan Growth Outpaces Owner Occupied In March”