The latest data from the ABS, Lending Finance for October 2016, shows total credit flows in October were $68.1 billion, up 0.72% compared with last month, in the more reliable trend terms. Within that, the total value of owner occupied housing commitments excluding alterations and additions fell 0.5% in trend terms, to $19.7 billion. Alterations and additions, fell 0.5%.

The trend series for the value of total personal finance commitments fell 1.2%. Revolving credit commitments fell 3.5%, while fixed lending commitments rose 0.1%. Total personal finance flows fell to $6.6 billion.

The trend series for the value of total personal finance commitments fell 1.2%. Revolving credit commitments fell 3.5%, while fixed lending commitments rose 0.1%. Total personal finance flows fell to $6.6 billion.

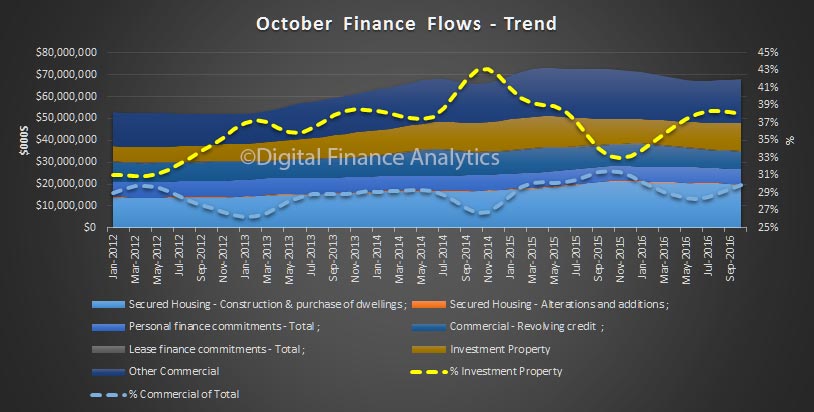

The trend series for the value of total commercial finance commitments rose 1.7% to $40.9 billion. Fixed lending commitments rose 2.0% to $32.8 billion and revolving credit commitments rose 0.4% to $8.1 billion

The trend series for the value of total lease finance commitments rose 0.1% in October 2016 and the seasonally adjusted series fell 11.8%, after a rise of 10.1% in September 2016.

What is possibly significant is that within the fixed business lending category, we have a combination of lending for investment property and lending for other business purposes. We are beginning to see a rise in other business lending, alongside lending for investment property. We need to see more of the former, and less of the latter.

Lending for investment property rose 1.5% to $12.5 billion, whilst lending for other business purposes rose 2.3% to $20.3 billion. As a result, the share of lending for business (other than for investment property) rose, whilst the share of commercial lending for investment property fell from 38.2% to 38%.

Looking at the investment property data, investors were hot to trot in Sydney, and Melbourne. Much of the investment property remains in these two centres.