Interesting BIS working paper which says that at low interest rates, monetary policy transmission becomes less effective.

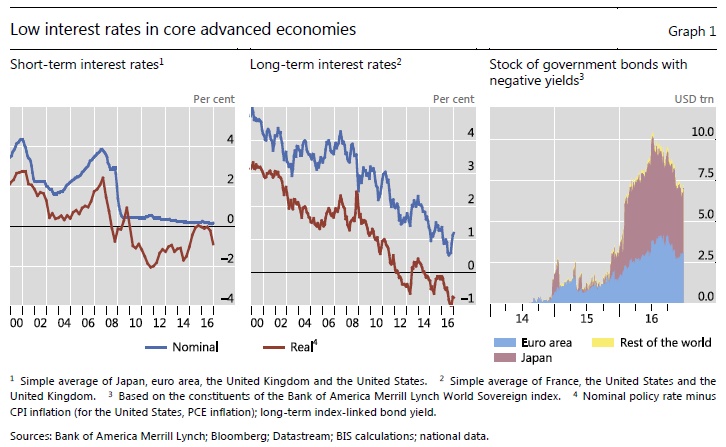

Interest rates in the core advanced economies have been persistently low for about eight years now. Short-term nominal rates have on average remained near zero since early 2009 and have been even negative in the euro area and Japan, respectively, since 2014 and 2016. The drop in short-term nominal rates has gone along with a fall in real (inflation-adjusted) rates to persistently negative levels. Long-term rates have also trended down, albeit more gradually, over this period: in nominal terms, they fell from between 3–4% in 2009 to below 1% in 2016.

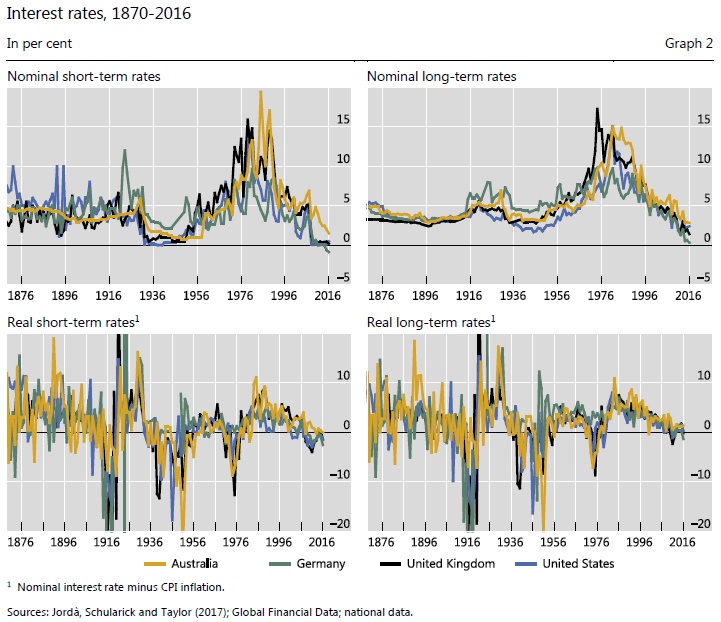

From a historical perspective, this persistently low level of short- and long-term nominal rates is unprecedented. Since 1870, nominal interest rates in the core advanced economies have never been so low for so long, not even in the wake of the Great Depression of the 1930s (Graph 2, top panels). Elsewhere, too, including in Australia, short- and long-term interest rates have fallen to new troughs, reflecting in part global interest rate spillovers especially at the long end.

The persistently low rates of the recent past have reflected central banks’ unprecedented monetary easing to cushion the fallout of the Great Financial Crisis (GFC), spur economic recovery and push inflation back up towards objectives. However, despite such efforts, the recovery has been lacklustre. In the core economies, for instance, output has not returned to its pre-recession path, evolving along a lower, if anything flatter, trajectory, as growth has disappointed. At the same time, in many countries inflation has remained persistently below target over the past three years or so.

Against this background, there have been questions about the effectiveness of monetary policy in boosting the economy in a low interest rate environment. This paper assesses this issue by taking stock of the existing literature. Specifically, the focus is on whether the positive effect of lower interest rates on aggregate demand diminishes when policy rates are in the proximity of what used to be called the zero lower bound. Moreover, to keep the paper’s scope manageable, we take as given the first link in the transmission mechanism: from the central bank’s instruments, including the policy rate, to other rates.

The review suggests that both conceptually and empirically there is support for the notion that monetary transmission is less effective when interest rates are persistently low. Reduced effectiveness can arise for two main reasons: (i) headwinds that typically blow in the wake of balance sheet recessions, when interest rates are low (eg debt overhang, an impaired banking system, high uncertainty, resource misallocation); and (ii) inherent nonlinearities linked to the level of interest rates (eg impact of low rates on banks’ profits and credit supply, on consumption and saving behaviour – including through possible adverse confidence effects – and on resource misallocation). Our review of the existing empirical literature suggests that the headwinds experienced during the recovery from balance-sheet recessions can significantly reduce monetary policy effectiveness. There is also evidence that lower rates have a diminishing impact on consumption and the supply of credit. Importantly, these results point to an independent role for nominal rates, regardless of the level of real (inflation-adjusted) rates.

The review reveals that the relevant theoretical and empirical literature is much scanter than one would have hoped for, in particular given that periods of persistently low interest rates have become more frequent and longer-lasting. While there are appealing conceptual arguments suggesting that monetary transmission may be impaired when rates are low, many of these have not been formalised by means of rigorous theoretical modelling. And the extant empirical work is limited, both geographically and in scope. For instance, most studies assessing changes in monetary transmission in low rate environments focus on the United States. Similarly, there is hardly any work assessing specific mechanisms. The field is wide open and deserves further exploration, not least given the first-order policy implications.

Note: BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS.